Can Flywire’s (FLYW) Deeper Workday Integration Shift Its Competitive Edge in Higher Education Payments?

Flywire Corp. FLYW | 11.64 | +1.31% |

- Earlier this month, Flywire Corporation announced an expanded partnership with Workday, Inc., integrating its payments and software platform with Workday Student to streamline billing, payments, and administrative tasks for higher education institutions.

- This collaboration brings Flywire’s global payment options and real-time data synchronization directly within Workday Student, offering a more seamless financial experience for both students and administrators while reducing manual workload by up to 40%.

- We'll explore how Flywire’s integration with Workday may influence its investment narrative by enhancing operational efficiencies for education clients.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

Flywire Investment Narrative Recap

To be a Flywire shareholder, you’ll need conviction in technology-driven efficiencies for global payments, especially in higher education, amid a shifting regulatory and competitive landscape. The recent partnership with Workday bolsters Flywire’s positioning as a preferred back-end payments provider in education, driving better client stickiness; however, it may not meaningfully change the shorter-term catalysts, which hinge on digital payments adoption and new client wins, or address the most pressing risks from policy uncertainty and revenue concentration.

Flywire’s most relevant recent announcement is its expanded Workday integration, which directly aligns with the automation and data connectivity that clients increasingly demand. This comes on the heels of Flywire showcasing strong returns from its Student Financial Software at its annual Fusion conference, evidence the company’s education vertical can generate measurable operational and financial improvements as clients upgrade systems.

However, investors should also consider that, despite technology partnerships, Flywire remains highly exposed to regulatory changes across key markets...

Flywire's narrative projects $817.0 million in revenue and $102.1 million in earnings by 2028. This requires 14.8% yearly revenue growth and a $95.3 million increase in earnings from $6.8 million today.

Uncover how Flywire's forecasts yield a $14.55 fair value, a 5% upside to its current price.

Exploring Other Perspectives

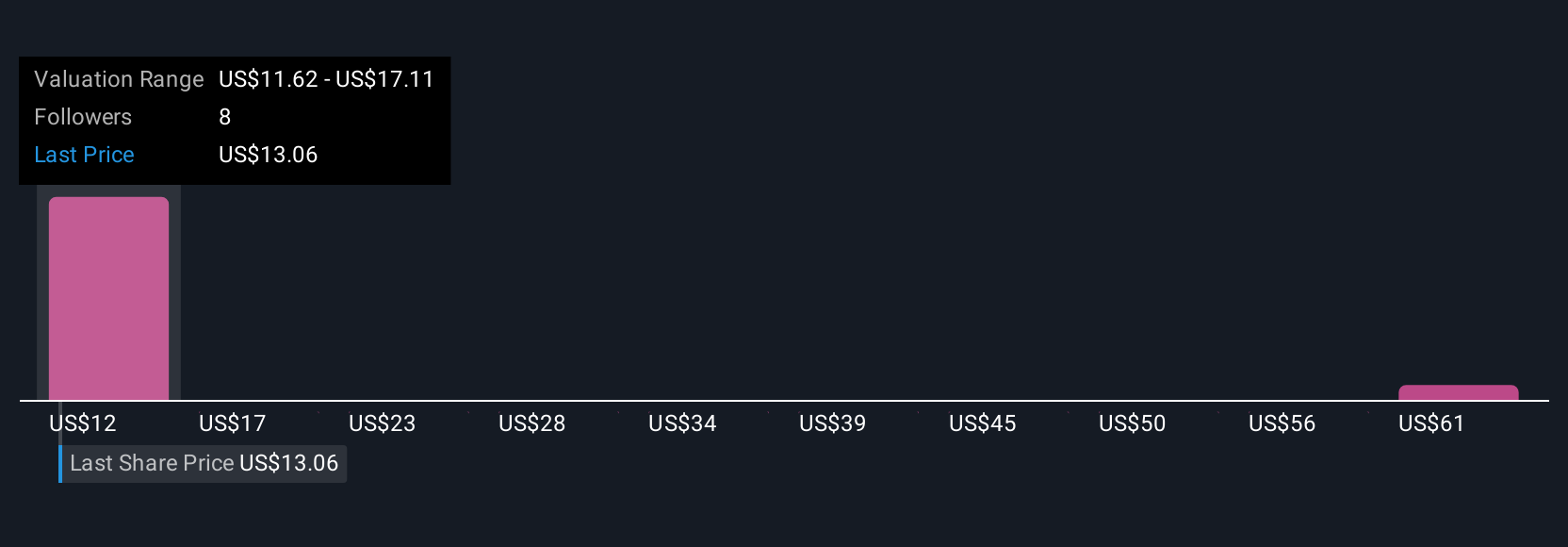

Simply Wall St Community members’ fair value estimates for Flywire span from US$13.70 to US$66.49, based on three unique perspectives. With ongoing regulatory risk in major education markets, you may want to compare these views and reflect on how regulation could influence growth and valuation.

Explore 3 other fair value estimates on Flywire - why the stock might be worth over 4x more than the current price!

Build Your Own Flywire Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Flywire research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flywire research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flywire's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.