Can Harmonic's (HLIT) Expanded Spectrum Partnership Offset Financial Fluctuations and Shape Its Growth Path?

Harmonic Inc. HLIT | 9.08 | +1.11% |

- On November 3, 2025, Spectrum announced an expanded partnership with Harmonic to deploy advanced cOS™ vCMTS and DOCSIS 4.0 technologies across its service area, coinciding with Harmonic's third-quarter earnings release which detailed year-over-year declines in revenue and net income but guidance for fourth-quarter growth.

- This collaboration highlights Harmonic's market leadership in virtual broadband technology and signals ongoing momentum in large-scale operator deployments, even as the company manages near-term financial fluctuations.

- We'll review how this broad rollout of DOCSIS 4.0 with Spectrum could influence Harmonic's investment narrative and future growth opportunities.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Harmonic Investment Narrative Recap

To be a Harmonic shareholder today, you need to believe in the company's ability to capitalize on the multi-year upgrade cycle in the broadband industry, driven by global demand for high-speed internet and next-generation DOCSIS 4.0 deployments, while weathering the volatility tied to its reliance on large customers. The expanded Spectrum partnership meaningfully supports the company's positioning in virtual broadband, but it does not neutralize the immediate revenue concentration risk or the financial impact of customer delays.

Of the recent announcements, Harmonic's completion of its share repurchase program stands out as especially relevant. By returning capital to shareholders even amid earnings headwinds, management reinforces confidence in its outlook and the value proposition tied to its ongoing broadband transition, though large customer dependencies remain a central challenge for future quarters.

Yet in contrast, investors should be mindful of just how much Harmonic's dependence on major customers like Comcast could impact revenue stability if...

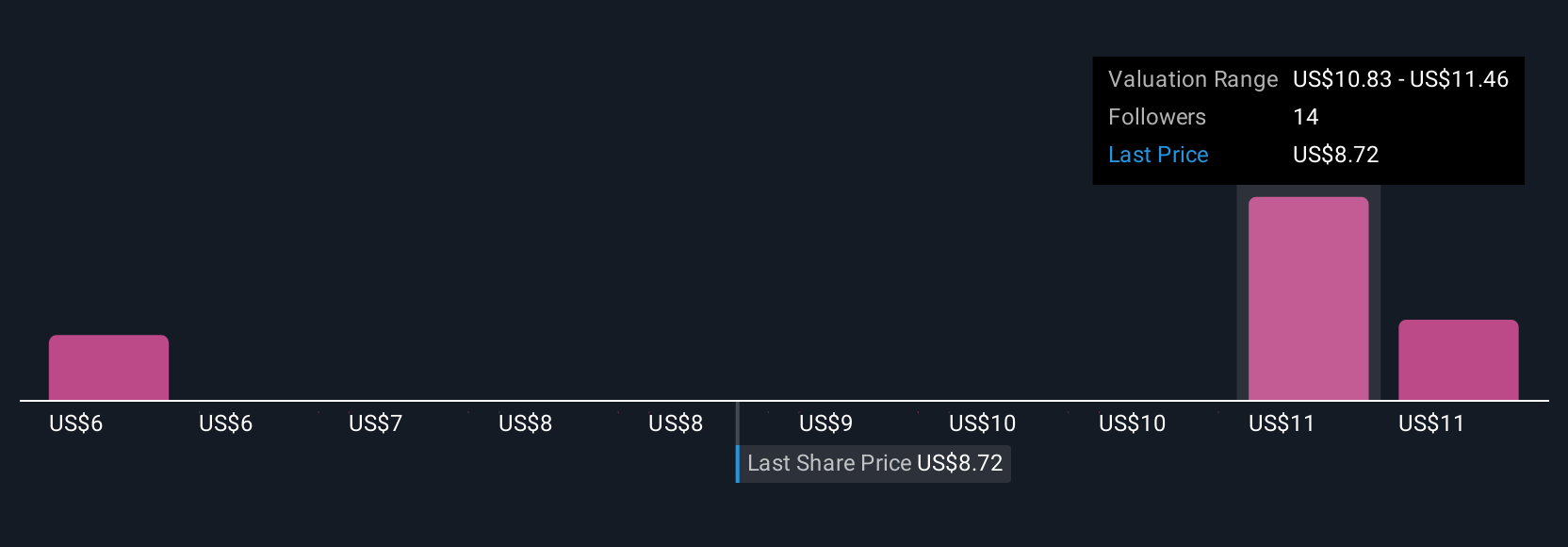

Harmonic's outlook forecasts $695.5 million in revenue and $70.6 million in earnings by 2028. This scenario implies a -0.3% annual revenue decline and a $2 million increase in earnings from the current $68.6 million.

Uncover how Harmonic's forecasts yield a $10.50 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Harmonic span from US$10.50 to US$174.13 across 3 perspectives. While some see significant upside, many continue to focus on risks tied to customer concentration and operator spending delays, making it essential to consider a range of possibilities for Harmonic’s future outcomes.

Explore 3 other fair value estimates on Harmonic - why the stock might be worth just $10.50!

Build Your Own Harmonic Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Harmonic research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Harmonic research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harmonic's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Find companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.