Can Healthpeak Properties’ (DOC) Lab Pivot Redefine Its Growth Trajectory Amid Asset Recycling?

Healthpeak Properties, Inc. DOC | 16.43 | 0.00% |

- Healthpeak Properties recently announced its third quarter 2025 results, reporting US$705.87 million in revenue, a US$117.12 million net loss, and reaffirming its full-year outlook while outlining significant asset recycling plans.

- An interesting insight is that, despite reporting a net loss, Healthpeak aims to reinvest over US$1 billion in proceeds from outpatient medical property sales into higher-return lab opportunities, supported by robust leasing pipelines and operational shifts such as internalized property management.

- We'll assess how Healthpeak's plan to recycle capital into lab assets and reaffirmed outlook shape its investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Healthpeak Properties Investment Narrative Recap

To be a shareholder in Healthpeak Properties today, you have to believe that its plans to recycle significant capital into higher-return lab assets, despite current net losses, will help offset ongoing sector uncertainties and volatile tenant demand. The recent quarterly results, reporting a US$117.12 million net loss, reaffirm the outlook but do not materially alter the most important short-term catalyst: the successful reinvestment of outpatient property sale proceeds into the lab segment. The biggest immediate risk remains execution delays or disruptions in these asset sales or reinvestments.

Among recent announcements, the update that Healthpeak completed no additional share buybacks last quarter stands out. While buybacks can support near-term valuation, this pause comes as the company prioritizes asset recycling and capital deployment for growth in labs, key to its catalyst of capital reallocation aimed at addressing current industry pressures.

Yet despite these growth-focused moves, investors should be aware that, if capital markets remain tight or transaction timelines slip, Healthpeak’s flexibility for new projects and debt management could be challenged...

Healthpeak Properties is expected to generate $3.1 billion in revenue and $198.8 million in earnings by 2028. This outlook is based on a projected annual revenue growth rate of 3.0%, and reflects a $34.8 million increase in earnings from the current $164.0 million.

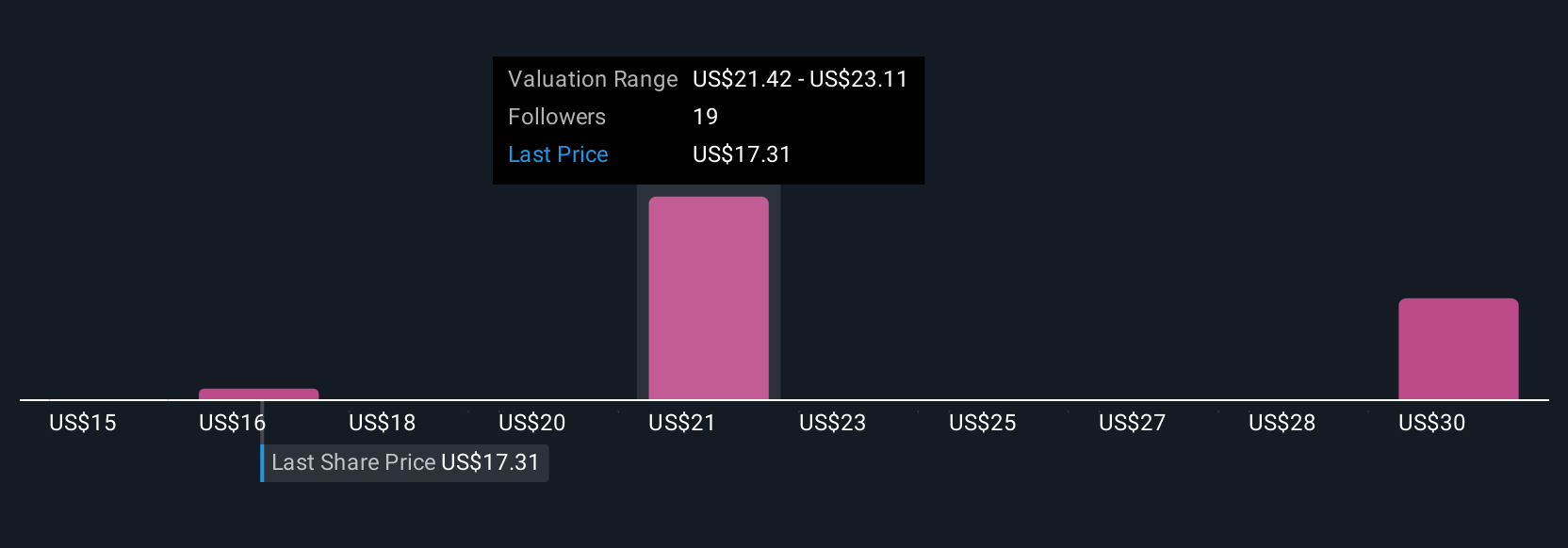

Uncover how Healthpeak Properties' forecasts yield a $21.19 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span US$14.63 to US$32.01 per share, showing broad splits among private analysts. While opinions differ, the ability to quickly recycle over US$1 billion from property sales could prove essential for Healthpeak’s future prospects, explore these alternative views for a balanced outlook.

Explore 6 other fair value estimates on Healthpeak Properties - why the stock might be worth 19% less than the current price!

Build Your Own Healthpeak Properties Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Healthpeak Properties research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Healthpeak Properties research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Healthpeak Properties' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.