Can InterDigital’s HDR Standards Push Quietly Reinforce Its Licensing-Led Cash Flows Story (IDCC)?

InterDigital, Inc. IDCC | 368.50 | +2.52% |

- InterDigital, Inc. recently showcased its “HDR Master Production for Advanced Streaming” solution at NAB 2026, highlighting metadata-driven workflows that enable simultaneous premium HDR and SDR content creation, ad insertion, and consistent format conversion across the broadcast and streaming chain.

- A key insight is InterDigital’s work on SMPTE’s Dynamic Range Conversion Characterization Metadata ST 2094-60, which aims to solve interoperability challenges in live HDR–SDR conversions, especially for demanding use cases like live sports.

- Now we’ll examine how this HDR workflow and standards push could influence InterDigital’s investment narrative built around licensing-led cash flows.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe its licensing engine, anchored by long contracts with Apple, Samsung and major CE and IoT manufacturers, can keep translating R&D into durable, high margin cash flows. The NAB 2026 HDR workflow showcase looks directionally helpful for strengthening InterDigital’s video IP story, but it does not appear to change the near term licensing renewal cycle or the key risk that expectations for non smartphone verticals may be running ahead of actual monetization.

Among recent announcements, the February 2026 Sony license, which covers cellular, Wi Fi and video patents across Sony devices, feels most connected to the NAB HDR news. Both point to InterDigital pushing deeper into video and broader consumer electronics, which matters because much of the bullish narrative assumes continued growth in CE and IoT royalties even as consensus forecasts only modest revenue expansion and some pressure on earnings over the next few years.

Yet against this constructive story, there is a material risk investors should be aware of if global regulators begin to tighten the rules around FRAND and patent licensing...

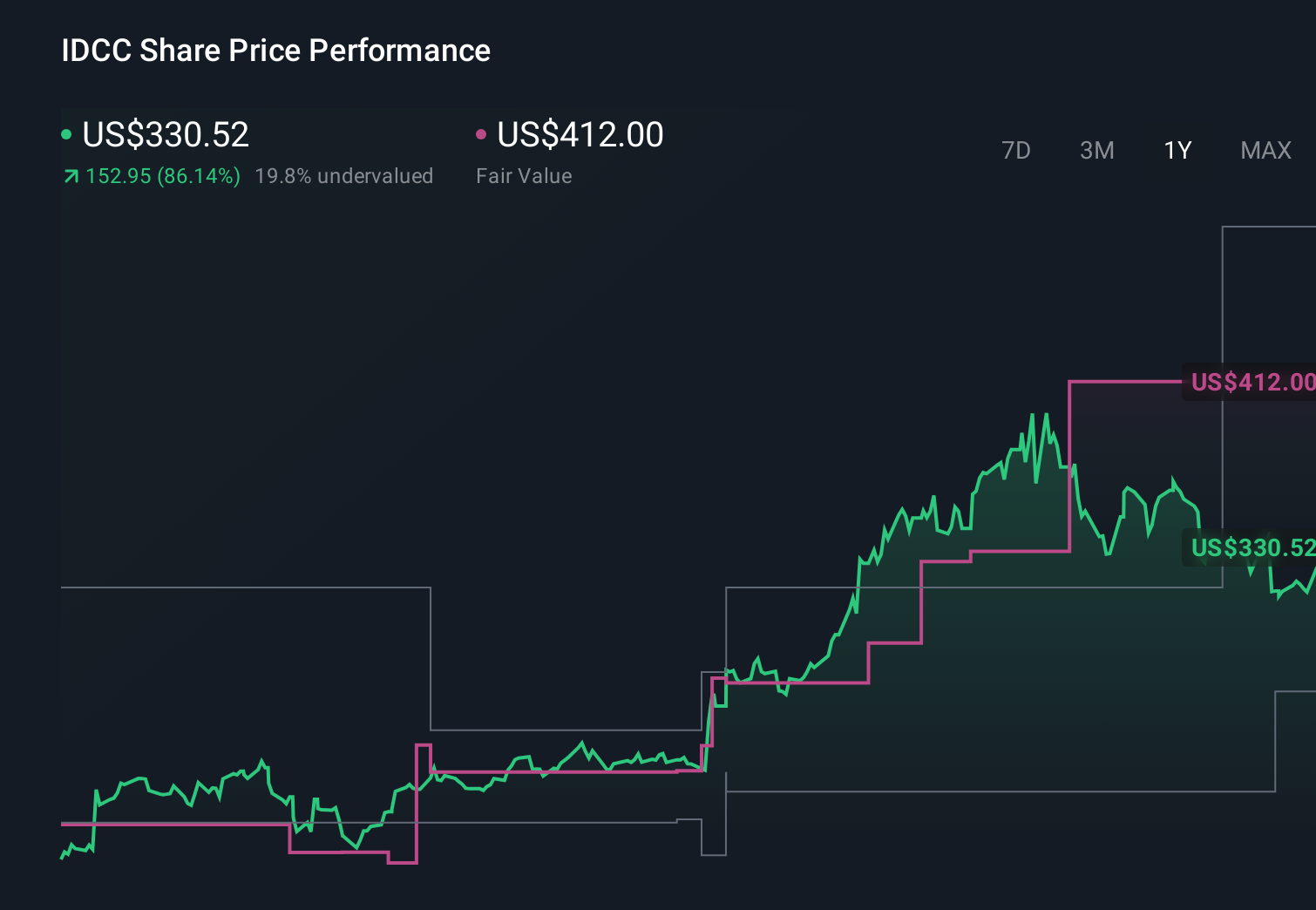

InterDigital's narrative projects $1.0 billion revenue and $490.5 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Compared with the consensus, the lowest analysts paint a more cautious picture, assuming revenue of about US$1.0 billion and earnings of roughly US$486.9 million by 2029, and they worry more that growing legal and enforcement costs could erode margins even if HDR and streaming standards success eventually broaden InterDigital’s addressable market.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth as much as 24% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.