Can Mondelez’s (MDLZ) Rising Debt and Falling EBIT Reshape Its Global Growth Ambitions?

Mondelez International, Inc. Class A MDLZ | 0.00 |

- Mondelez International’s net debt climbed to about US$19.4 billion as of June 2025, while its interest coverage ratio remained healthy and above 8.

- An interesting insight is that, despite a sharp 31% decline in EBIT last year, Mondelez International continues to generate substantial free cash flow and maintains a large market capitalization, helping it manage these challenges for now.

- Next, we’ll examine how concerns around declining EBIT and rising debt could influence the company’s global growth investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Mondelez International Investment Narrative Recap

To be a shareholder in Mondelez International, you need to believe in the company’s ability to use its global brand strength and innovation to pursue steady growth, despite headwinds like last year’s 31% EBIT decline and rising net debt to about US$19.4 billion. While the news of increasing debt and falling EBIT highlights short-term financial pressures, the core catalyst remains Mondelez’s sustained pricing power and brand momentum; so far, these issues do not represent a material change to that story.

Among recent announcements, Mondelez’s reaffirmation of 5% organic net revenue growth guidance is particularly relevant. This outlook indicates that, despite higher cocoa costs and increased leverage, management maintains confidence in revenue drivers such as new product launches and expanded distribution, aligning with the narrative of resilient top-line growth as a key catalyst.

On the flip side, investors should be alert to the potential impact on net margins if elevated cocoa prices persist and…

Mondelez International's narrative projects $42.7 billion revenue and $4.7 billion earnings by 2028. This requires 4.8% yearly revenue growth and a $1.1 billion earnings increase from $3.6 billion today.

Uncover how Mondelez International's forecasts yield a $74.44 fair value, a 17% upside to its current price.

Exploring Other Perspectives

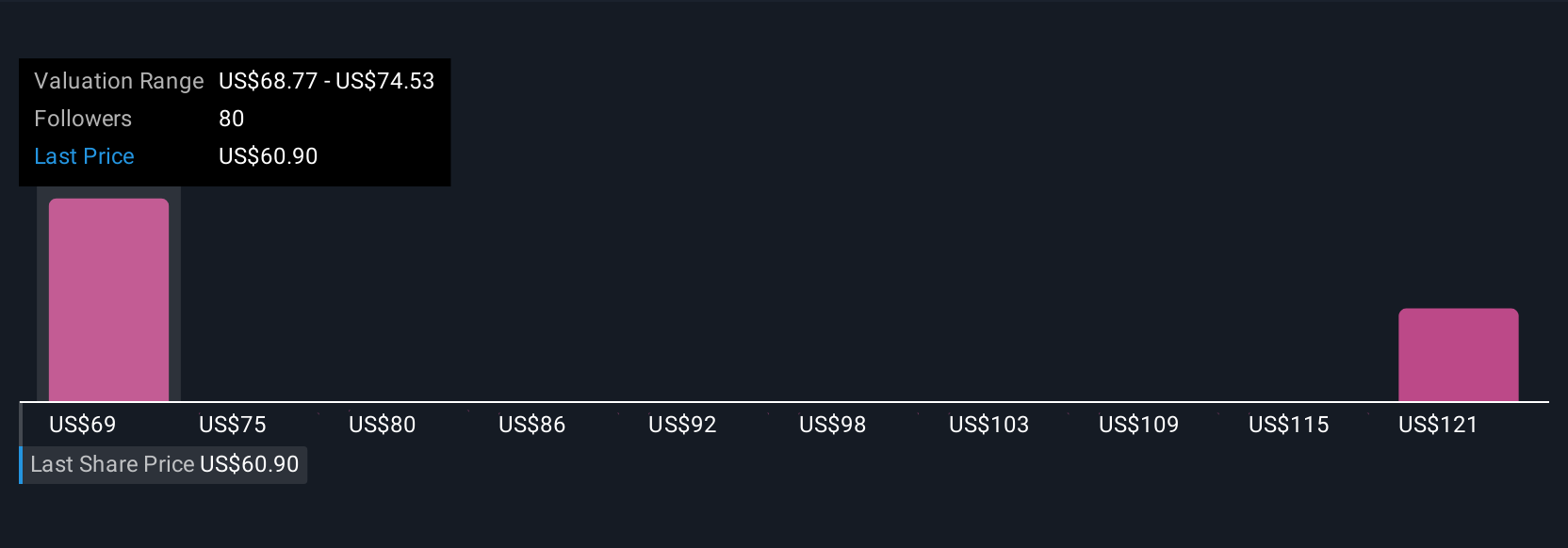

Five fair value estimates from the Simply Wall St Community range from US$68.77 to US$126.40 per share, reflecting wide-ranging expectations. While opinions differ, ongoing EBIT declines and higher debt levels could influence your view on Mondelez’s future performance, so it pays to consider several alternative viewpoints.

Explore 5 other fair value estimates on Mondelez International - why the stock might be worth just $68.77!

Build Your Own Mondelez International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mondelez International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Mondelez International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mondelez International's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.