Can Okta (OKTA) Sustain Its Leadership Edge in AI-Driven Identity Security Solutions?

Okta, Inc. Class A OKTA | 79.14 77.98 | +0.55% -1.47% Pre |

- Okta was recently recognized for the ninth consecutive year as a Leader in the 2025 Gartner Magic Quadrant for Access Management, demonstrating continued product execution and market presence, and announced enhanced Auth0 Platform capabilities to support secure AI agent development.

- This leadership highlights how Okta is responding to the rapid emergence of AI-driven identity security needs amid an evolving regulatory landscape and rising enterprise demand for unified identity management platforms.

- We'll explore how Okta's advancements in AI-driven identity security and sustained industry leadership may influence its investment narrative going forward.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Okta Investment Narrative Recap

To own Okta stock, investors need confidence in the company’s ability to remain essential as identity security becomes increasingly complex, especially with the rise of AI agents and evolving privacy regulations. The recent launch of Okta’s Canadian cell and support for local compliance does not materially alter the near-term catalyst, which remains centered on Okta’s upcoming earnings report and its ability to sustain revenue growth while facing ongoing competition and integration risks. The greatest immediate risk continues to be market share pressure from integrated security platforms, and this latest news is unlikely to shift that dynamic.

Among recent announcements, Okta’s new Canadian cell stands out for its alignment with regulatory requirements and enhanced data residency, particularly as local enterprises seek secure solutions for AI-driven data access. By addressing Canadian privacy laws and offering quicker disaster recovery, this expansion targets key client concerns, further supporting Okta's narrative of winning complex, compliance-driven deals that could reinforce its standing in high-value markets while execution risks persist.

Yet, against these strengths, investors should also be aware of the challenges Okta faces in keeping pace with rapid platform integrations and evolving market expectations...

Okta's narrative projects $3.6 billion revenue and $414.2 million earnings by 2028. This requires 9.5% yearly revenue growth and a $246.2 million earnings increase from $168.0 million today.

Uncover how Okta's forecasts yield a $120.37 fair value, a 53% upside to its current price.

Exploring Other Perspectives

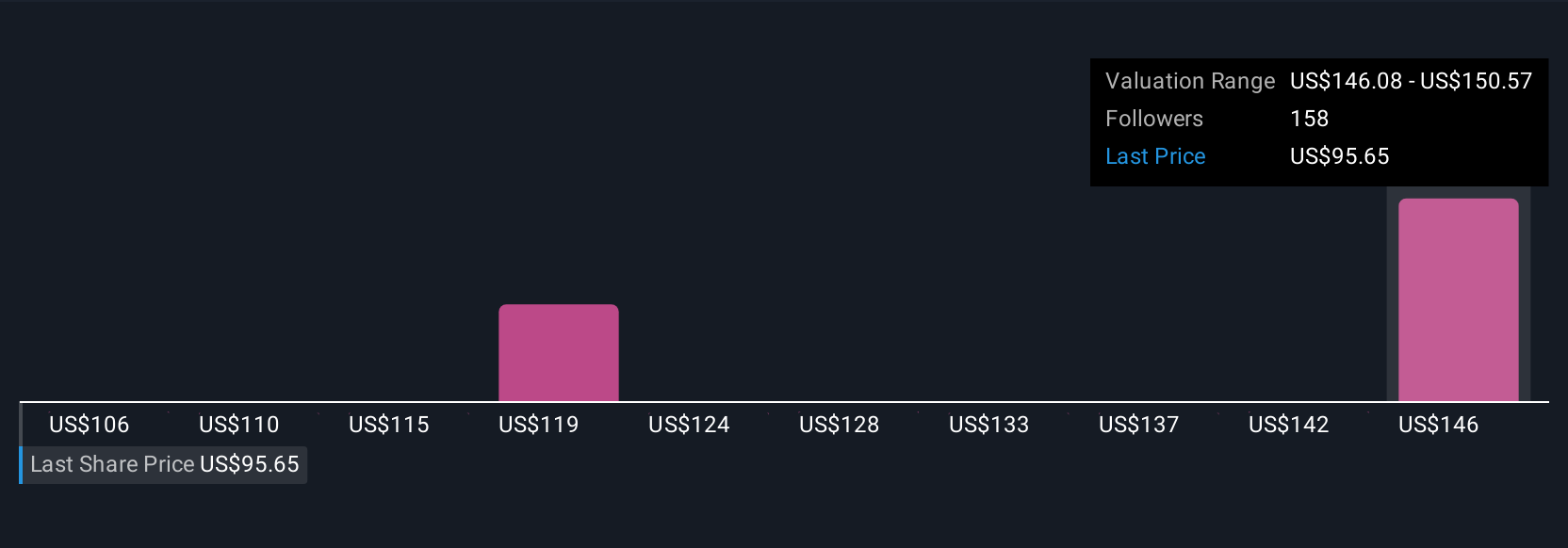

Fair value estimates from 7 members of the Simply Wall St Community span US$105.65 to US$147.87. While investor opinions vary, continued competition from bundled security suites could influence Okta’s ability to defend pricing and market share even as compliance-driven expansions gain traction.

Explore 7 other fair value estimates on Okta - why the stock might be worth just $105.65!

Build Your Own Okta Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Okta research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Okta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Okta's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.