Can Public Storage’s (PSA) Acquisition-and-Tech Push Offset Rising Occupancy and Funding Risks?

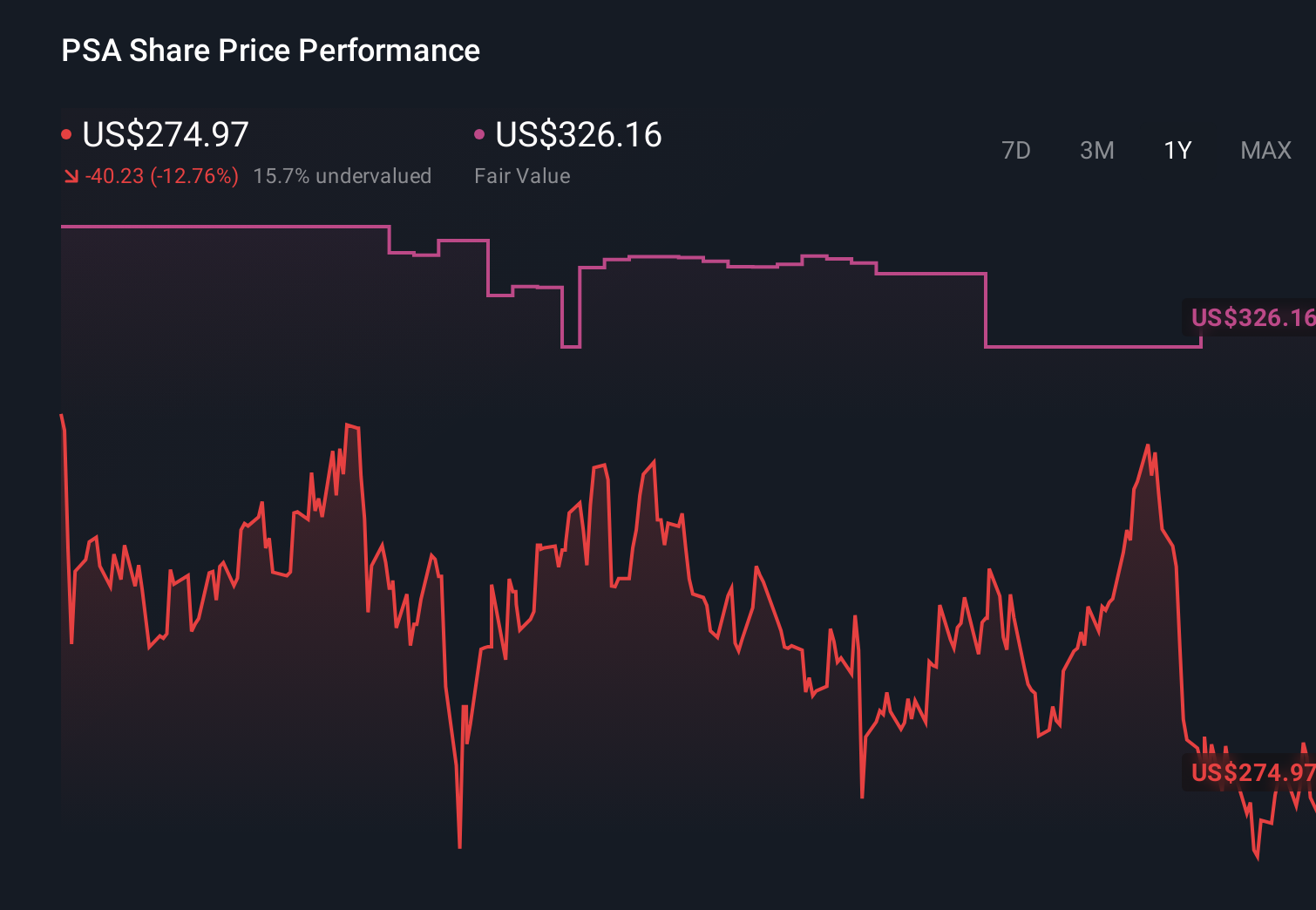

Public Storage PSA | 280.35 | +1.49% |

- In recent months, Public Storage, a major US self-storage REIT, has drawn attention for continued facility acquisitions, technology investments, and disciplined rent optimization amid sector concerns about occupancy and interest rates.

- What stands out is how the company’s steady acquisition pace and digital focus are being weighed directly against rising occupancy risk and funding costs.

- We’ll now examine how this focus on occupancy resilience and interest rate uncertainty could influence Public Storage’s broader investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Public Storage Investment Narrative Recap

To own Public Storage, you need to be comfortable with a steady, income oriented REIT that is leaning on its large footprint, brand, and technology to support cash flows while occupancy and interest rates stay in focus. Recent trading pressure around these issues does not appear to materially alter the near term story, where the key catalyst remains demand resilience at existing facilities and the biggest risk is a prolonged period of weaker occupancy in oversupplied markets.

The company’s continued acquisition of 260 facilities since early 2023, alongside digital investments for revenue optimization, is the most relevant recent development here, because it reinforces the importance of how well new and existing properties are filled and priced. As investors weigh this expansion against sector concerns, the next phase of the story will likely hinge on whether these added properties support, or dilute, overall occupancy resilience.

Yet while acquisitions and technology may support the story, investors should be aware of the risk that persistent industry oversupply in key markets could...

Public Storage’s narrative projects $5.3 billion revenue and $2.0 billion earnings by 2028. This requires 3.8% yearly revenue growth and roughly a $0.4 billion earnings increase from $1.6 billion today.

Uncover how Public Storage's forecasts yield a $319.10 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Five Public Storage fair value estimates from the Simply Wall St Community range widely, from about US$260 to roughly US$475 per share, underlining how differently people see the same stock. When you set those views against current concerns around occupancy risk and interest rate uncertainty, it becomes clear that checking several perspectives can help you think through how resilient the company’s performance might be.

Explore 5 other fair value estimates on Public Storage - why the stock might be worth just $260.01!

Build Your Own Public Storage Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Public Storage research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Public Storage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Public Storage's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.