Can PVH (PVH) Tariff Offsets Mask Deeper Brand and Profitability Challenges?

PVH Corp. PVH | 0.00 |

- PVH Corp., the owner of Calvin Klein and Tommy Hilfiger, recently outlined plans to offset a larger share of tariff costs through measures such as vendor negotiations, re-sourcing, and pricing changes, aiming to mitigate about three quarters of its tariff burden on an annualized basis by 2026.

- At the same time, PVH’s below-standard constant currency growth, stagnant returns on capital, and flat free cash flow margins underscore that tariff mitigation alone does not resolve the company’s underlying operational and competitive pressures.

- We’ll now examine how PVH’s push to offset a greater share of tariff costs interacts with its existing investment narrative and risk profile.

Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

PVH Investment Narrative Recap

To own PVH, you need to believe its Calvin Klein and Tommy Hilfiger franchises can translate cost savings and brand investments into healthier margins, even as growth and returns remain muted. The tariff mitigation plan reduces one near term earnings headwind, but it does not change that the key catalyst is operational execution under PVH+ and the biggest risk is that weak brand momentum, especially in digital and APAC, keeps returns on capital and free cash flow stuck at low levels.

Against this backdrop, PVH’s recent Q4 2026 results, with full year sales of US$8,950.2 million and net income of US$25.3 million after a large one off loss, are an important reference point. They highlight how much work remains to convert tariff mitigation, AI partnerships, and supply chain efforts into durable profitability, and to support any thesis that earnings can recover meaningfully from today’s very thin net margin base.

But investors should also be aware of the ongoing risk that PVH’s heavy dependence on Calvin Klein and Tommy Hilfiger could start to...

PVH's narrative projects $9.4 billion revenue and $707.7 million earnings by 2028. This requires 2.3% yearly revenue growth and a $239.2 million earnings increase from $468.5 million today.

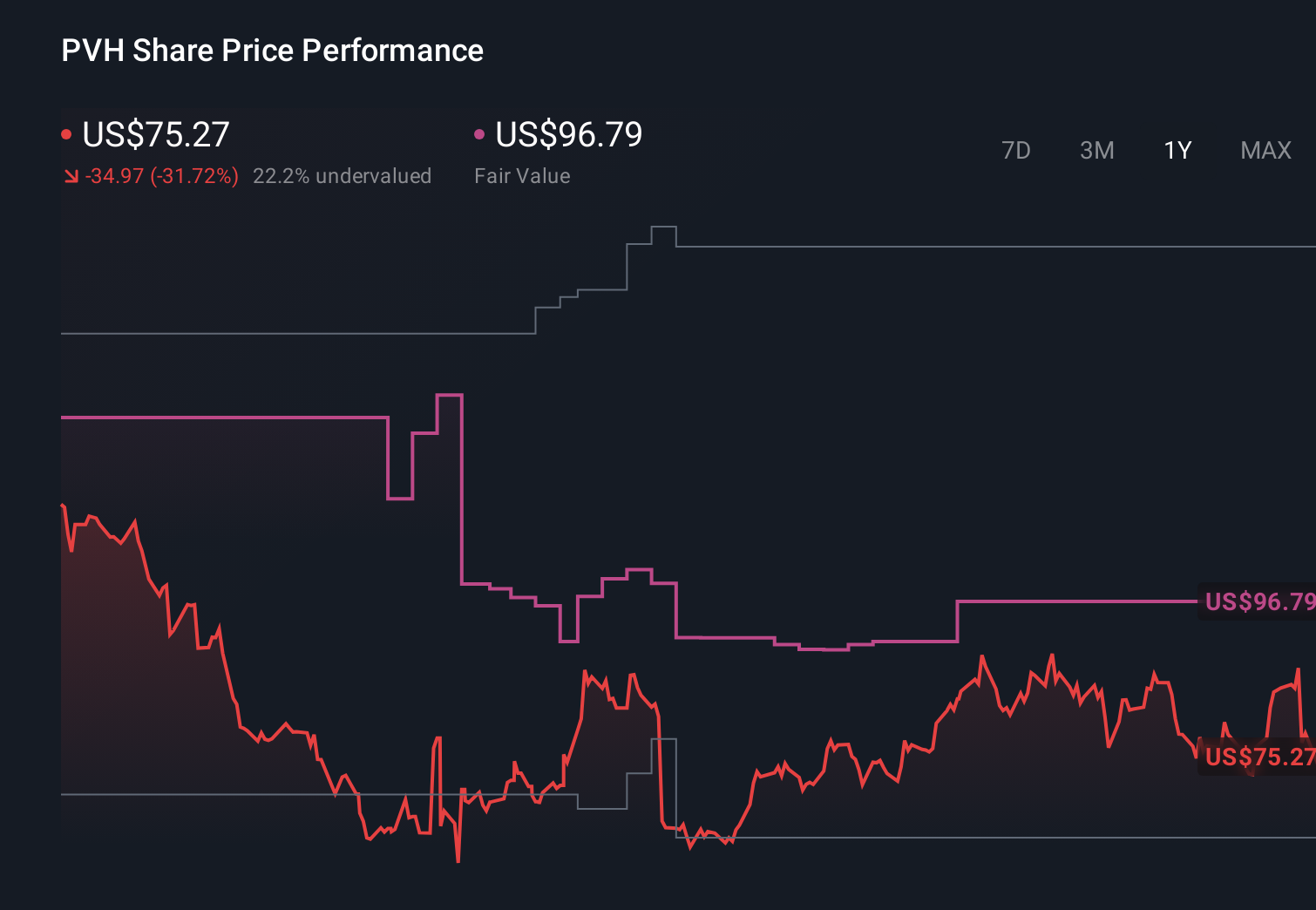

Uncover how PVH's forecasts yield a $96.79 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some analysts see a much brighter path, assuming revenue climbs to about US$9.7 billion and earnings to roughly US$680 million, while tariff pressures and brand concentration risks highlight how sharply opinions can diverge and why this new tariff news could reshape both the optimistic and cautious views.

Explore 4 other fair value estimates on PVH - why the stock might be worth just $96.79!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PVH research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

No Opportunity In PVH?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find 58 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.