Cardinal Health (CAH) Valuation Check After Strong Recent Share Price Momentum

Cardinal Health, Inc. CAH | 214.05 | +0.96% |

Recent share performance and business scale

Cardinal Health (CAH) has attracted fresh attention after a strong past 3 months, with the stock showing a 36.47% total return and a 7.87% move over the past month.

For investors looking at the current backdrop, Cardinal Health last closed at $213.46, with a 1 day return close to flat and a 7 day return of 5.42%. The company reports annual revenue of about $234.31b and net income of $1.60b. This indicates a sizeable role in global healthcare distribution and services.

Over longer periods, the stock has delivered a 70.15% total return over the past year, with multi year total returns that are also positive. Year to date, the share price total return stands at 3.76%. Some investors may compare this with the recent acceleration in shorter term moves.

For context, Cardinal Health’s recent momentum, with a 36.47% 90 day share price return, sits on top of a much longer run where total shareholder returns over 3 and 5 years have been very strong. This can signal shifting expectations around its role in global healthcare distribution and services rather than just short term trading interest.

If Cardinal Health has caught your attention, it can be useful to compare it with other large players and see what else is setting up well across healthcare stocks.

With Cardinal Health trading at $213.46, an implied price target of $226.60 and one estimate of intrinsic value suggesting a larger discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 3.9% Undervalued

Compared with the last close at $213.46, the most followed narrative points to a fair value of about $222.20, using a 6.96% discount rate and explicit long term earnings and margin assumptions.

The company's investments in automation, advanced supply chain technology, and new distribution centers are expected to deliver long-term operational efficiencies and cost savings, supporting improved net margins and free cash flow as healthcare shifts to value-based and outpatient models.

Curious what kind of revenue growth, margin lift, and earnings multiple have to line up to support that valuation gap? The full narrative spells out the entire earnings roadmap and the profit profile it assumes for Cardinal Health over the next few years.

Result: Fair Value of $222.20 (UNDERVALUED)

However, regulatory pressure on drug pricing and the risk of major customer contract changes could quickly challenge those upbeat earnings and valuation assumptions.

Another Angle On Valuation

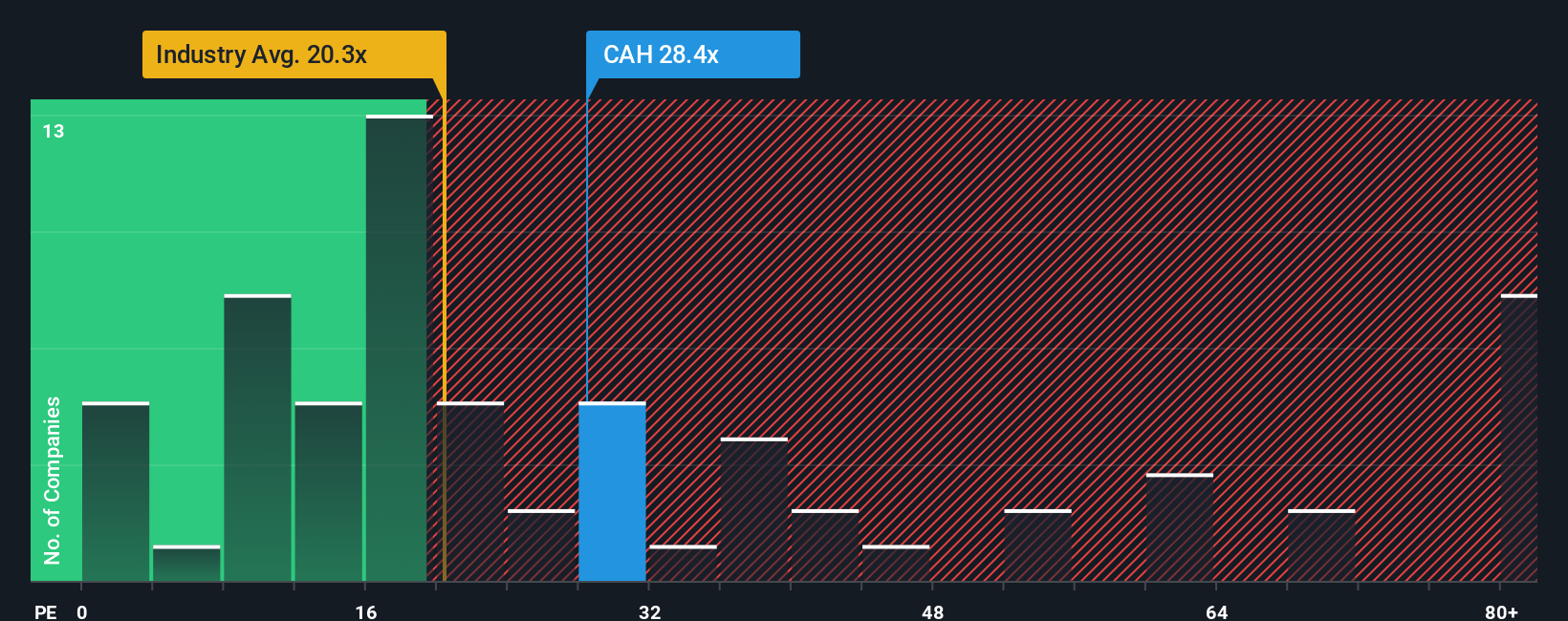

Those fair value models suggest upside, but the current P/E of 31.8x tells a different story. It sits above both the peer average of 28.1x and the Healthcare industry at 23.2x, and even edges past the 30.8x fair ratio our work points to. This leans toward valuation risk rather than a clear bargain.

Build Your Own Cardinal Health Narrative

If you see the numbers differently or prefer to stress test your own assumptions, you can build a complete view in just a few minutes with Do it your way.

A great starting point for your Cardinal Health research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Cardinal Health has sharpened your interest, do not stop here. Widen your opportunity set now so you are not relying on a single story.

- Spot potential turnaround names by scanning these 3538 penny stocks with strong financials that already show stronger financial underpinnings than many expect from low priced shares.

- Target the next wave of automation in medicine with these 108 healthcare AI stocks that connect data driven care with listed companies shaping that shift.

- Zero in on potential income ideas using these 12 dividend stocks with yields > 3% that focus on companies offering yields above 3% alongside listed track records.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.