Carrier Global (CARR) Stock Could Be 5.9% Undervalued After Europe Leadership Change

Carrier Global Corp. CARR | 0.00 |

Carrier Global (CARR) is drawing attention after announcing a leadership transition in its Climate Solutions Europe segment, with Thomas Donato taking over as president from long-serving executive Thomas Heim.

Carrier Global's recent leadership change in Climate Solutions Europe lands at a time when the stock has strong short term momentum, with a 30 day share price return of 16.88% and a year to date share price return of 34.17%, alongside a 5 year total shareholder return of 66.17%. This may suggest that investors are reassessing both growth prospects and risks around its climate and energy solutions focus.

If this shift in Carrier Global's European operations has your attention, it could be a moment to broaden your watchlist and check out 34 power grid technology and infrastructure stocks

With Carrier Global stock trading at US$71.81 and sitting about 6% below the average analyst price target and roughly 27% below one intrinsic value estimate, investors have to ask: is there still upside here, or is future growth already in the price?

Most Popular Narrative: 5.9% Undervalued

On the most followed narrative, Carrier Global’s fair value of $76.31 sits modestly above the last close at $71.81, which puts extra focus on what is driving that gap.

Carrier's introduction of differentiated products, such as air-cooled commercial heat pumps and the integration of HEMS technology with Google Cloud's AI, positions them to capture the growing demand for sustainable and smart energy solutions, potentially driving future revenue growth.

The company's strong performance in the aftermarket space, with double-digit growth and increased attachment rates on chillers, is expected to bolster net margins through high-margin service offerings and customer retention.

Want to see why this narrative prices Carrier Global above today’s share price? The whole framework leans on tighter margins, steadier revenue compounding, and a richer earnings multiple baked into 2029. The crucial inputs, and how they interact, sit just beneath the surface of that fair value line.

Result: Fair Value of $76.31 (UNDERVALUED)

However, Carrier Global’s narrative can be knocked off course if tariff exposure and weaker Climate Solutions Asia, Middle East & Africa performance affect the earnings path analysts are assuming.

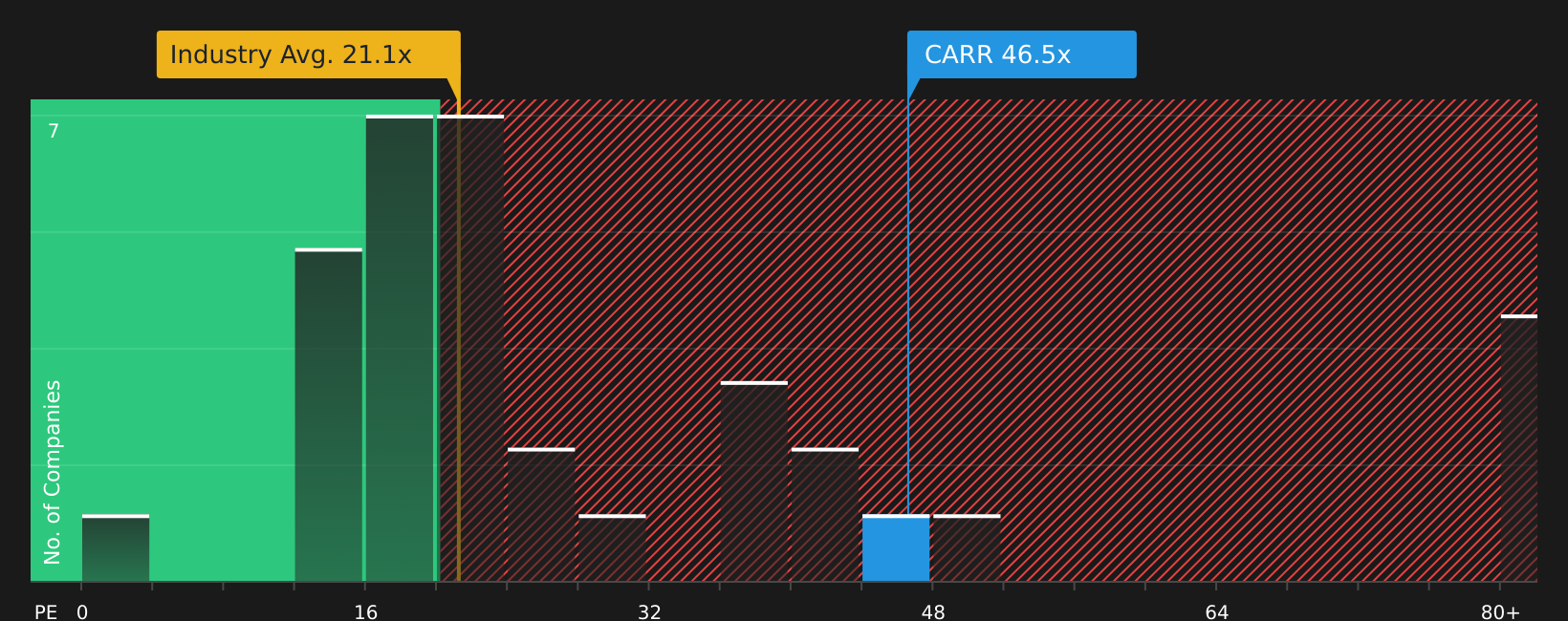

Another View: What Carrier Global’s P/E Is Telling You

While the preferred narrative frames Carrier Global as 5.9% undervalued, the P/E lens points in the opposite direction. At 46.5x earnings, the stock trades well above the peer average of 30.7x and the US Building industry at 20.6x, and also exceeds a fair ratio of 38.1x.

That kind of gap can mean investors are paying up today for expectations that may already be ambitious. This raises the risk that any disappointment in earnings or margins could hit the share price harder than the DCF view suggests. Which yardstick do you trust more when numbers start to diverge?

Next Steps

Seeing both optimism and concern around Carrier Global in the numbers, do you want to quickly test the thesis yourself? Start with the key balance of risks and potential upsides highlighted in our 2 key rewards and 1 important warning sign

Looking For More Investment Ideas Beyond Carrier Global?

If Carrier Global has sharpened your thinking, do not stop here. Use fresh stock ideas to pressure test your views and keep your portfolio options open.

- Spot potential high growth stories early by scanning 24 elite penny stocks with strong financials and see which smaller companies already show stronger financial foundations.

- Strengthen your watchlist with companies that pair financial quality and appealing prices by reviewing the 45 high quality undervalued stocks.

- Reduce portfolio stress by focusing on companies with sturdier finances through the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.