Carrier Global (CARR) Valuation Check After Q1 Beat And Surging Data Center Orders

Carrier Global Corp. CARR | 0.00 |

Carrier Global (CARR) is back in focus after Q1 2026 results topped expectations, total orders rose 11%, and data center demand was strong enough to fully cover the company’s targeted 2026 sales.

The Q1 beat and reaffirmed 2026 guidance have been met with strong buying interest, with a 21.38% 1 month share price return and 26.35% year to date, even though the 1 year total shareholder return is down 4.42%, so momentum is clearly building off a longer term gain of 65.65% over three years.

If data center and electrification themes are on your radar, this is a useful moment to broaden your watchlist with 37 AI infrastructure stocks

With Carrier now trading near US$68 and analyst targets clustered in the mid US$70s, recent gains and strong data center orders appear to be well recognized. This raises the question of whether there is still a buying opportunity here or whether potential future growth is already reflected in the price.

Most Popular Narrative: 4.8% Undervalued

Carrier Global's most followed narrative pins fair value at $71.03 versus the last close at $67.62, so the gap to that estimate is relatively modest.

The analysts have a consensus price target of $71.03 for Carrier Global based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $90.0, and the most bearish reporting a price target of just $55.0.

Want to see what is sitting behind that fair value label? The narrative leans on steadier revenue, fatter margins and a richer earnings multiple than the sector. Curious how those pieces fit together into $71.03.

Result: Fair Value of $71.03 (UNDERVALUED)

However, there are still pressure points to watch, including softer demand in parts of the light commercial business and tariff exposure. These factors could squeeze margins if pricing power weakens.

Another Angle on Value: Earnings Multiple

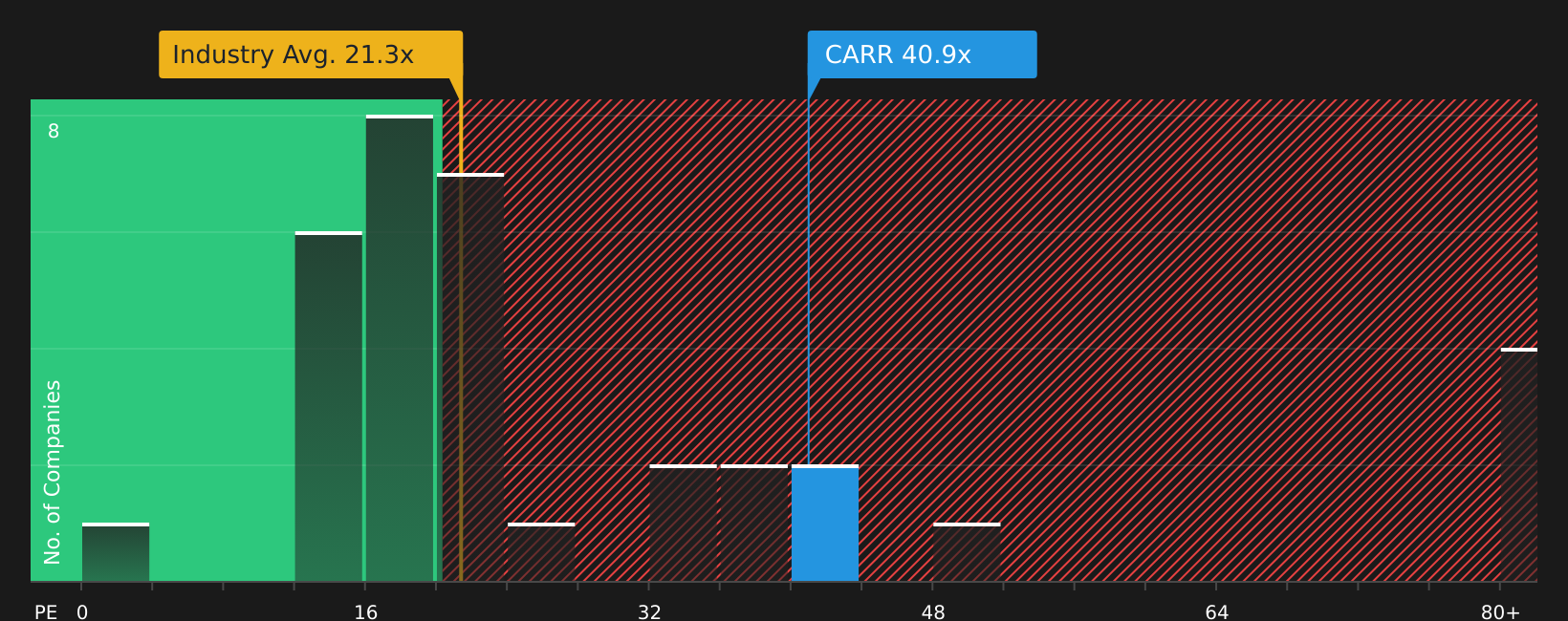

The analyst narrative points to a fair value of $71.03 and labels Carrier Global as modestly undervalued. However, the current P/E of 44.1x is well above the estimated fair ratio of 39.8x, the US Building industry at 21.7x, and peers at 31.5x. This points to heavier valuation risk if growth stumbles and raises the question of whether the premium is justified or whether enthusiasm is simply catching up with the stock.

Next Steps

Mixed messages on value, momentum and data center exposure can be hard to weigh, so take a moment to review the key numbers yourself and decide where you stand. Then round out your view with 1 key reward and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock story, you risk missing other opportunities that might suit your goals even better, so widen your search before you act.

- Target sturdier portfolios by focusing on companies with strong finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Spot potential value gaps by scanning for mispriced quality companies using the 50 high quality undervalued stocks.

- Grow your watchlist with under-the-radar businesses that still have solid fundamentals via the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.