Carvana (CVNA) Expands Sarasota Capacity, Is The Stock Still 32% Undervalued?

Carvana CVNA | 0.00 |

Carvana (CVNA) has moved to expand its operations by adding Inspection and Reconditioning Center capabilities to its ADESA Sarasota auction site, creating more reconditioning capacity and a new local inventory pool.

Carvana's expansion in Sarasota comes at a time when the stock has been under pressure in the short term, with the share price down 14.59% over the past 30 days and 22.11% year to date, even as the 3 year total shareholder return exceeds 10x and the 1 year total shareholder return is close to flat.

If this kind of operational shift has your attention, it can be useful to widen the lens and look for other companies with similar potential in the auto and retail space through the 20 top founder-led companies

Given Carvana’s short term share price pressure, long term total returns of more than 10x over three years, and its current discount to the average analyst price target, is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 32.3% Undervalued

Carvana's most followed narrative places fair value at $92.10 per share, well above the last close of $62.35. This frames the Sarasota expansion inside a wider growth and margin story.

The company's scaled logistics and reconditioning infrastructure, bolstered by the integration of ADESA locations, is driving lower delivery and inbound transport costs. As utilization rises, these investments are expected to further enhance operating leverage, improving gross margins and profitability.

Want to see what sits behind that confidence in Carvana's future economics? The narrative leans heavily on sustained revenue growth, firmer margins, and a premium profit multiple. Curious which assumptions need to hold for that projected earnings power to line up with a fair value near $92?

Result: Fair Value of $92.10 (UNDERVALUED)

However, Carvana’s story also hinges on ambitious unit growth and ADESA integrations, where slower utilization gains or higher operating costs could quickly pressure margins and earnings power.

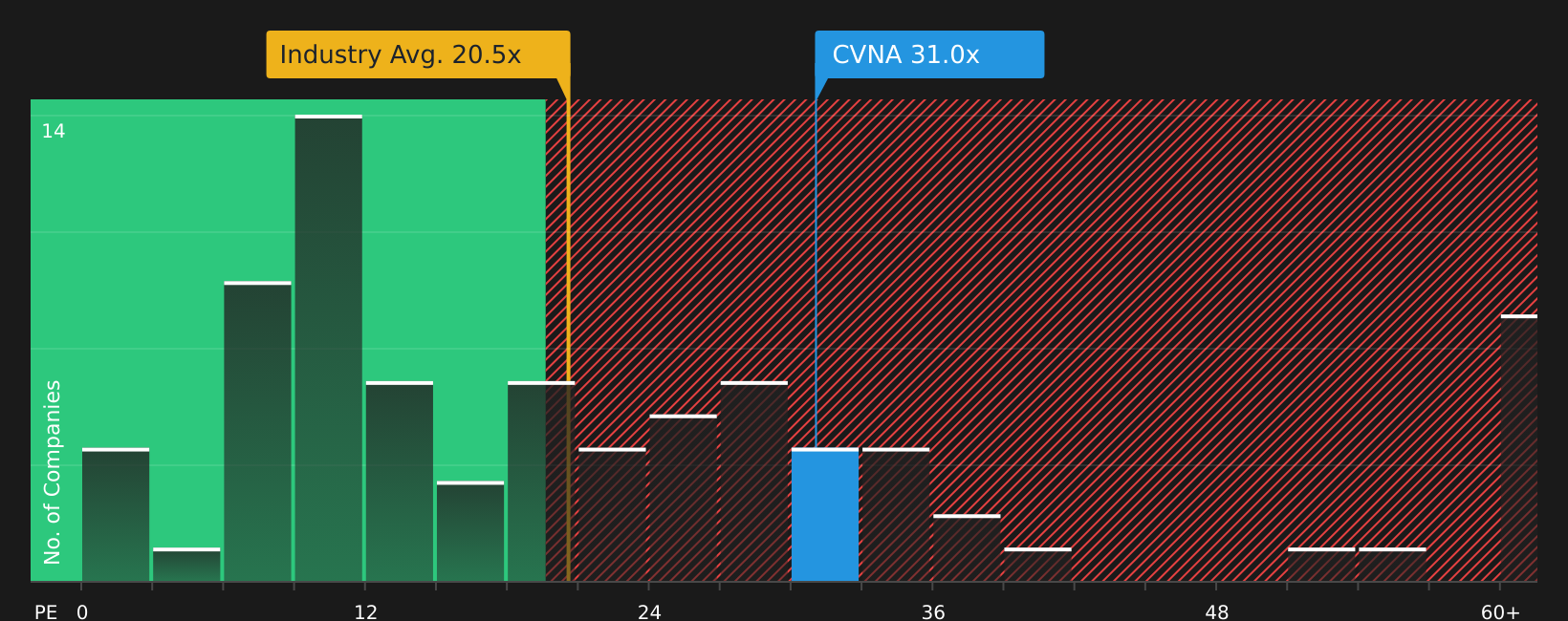

Another View: Carvana Through The P/E Lens

The 32.3% undervalued narrative around Carvana leans on future earnings power, but today’s price tells a different story. At about 31x P/E, the stock trades above the US Specialty Retail average of 20.5x and above its own fair ratio of 29.8x. This points to less room for error if growth or margins fall short. Is this a premium you are comfortable paying for the current thesis?

Next Steps

After weighing both the optimism and the concerns around Carvana, are you ready to look under the hood yourself, review the key data points quickly, and decide where you stand using the 3 key rewards and 2 important warning signs

Looking for more Carvana style investment ideas?

If Carvana has sharpened your focus, do not stop here. Broaden your watchlist with a few targeted stock ideas that you can review in minutes.

- Spot potential mispricing early by scanning 44 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your portfolio’s foundation by checking companies in the solid balance sheet and fundamentals stocks screener (48 results) that prioritize financial resilience and disciplined capital structures.

- Get ahead of the crowd by reviewing the screener containing 19 high quality undiscovered gems that currently sit off most investors’ radar yet show robust underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.