Carvana (CVNA) Is Down 6.7% After Record Q1 2026 Results And Syracuse Expansion Plans – Has The Bull Case Changed?

Carvana CVNA | 0.00 |

- In the first quarter of 2026, Carvana reported record results, with sales of US$526 million, revenue of US$6.43 billion, and net income of US$250 million, alongside higher earnings per share than a year earlier.

- A day earlier, the company revealed plans to add an Inspection and Reconditioning Center at its long-standing ADESA Syracuse auction site, expanding capacity, creating about 200 local jobs over time, and deepening its integrated reconditioning network.

- We’ll now explore how Carvana’s record quarterly earnings and expanded Syracuse reconditioning hub affect the company’s longer-term investment narrative.

Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

Carvana Investment Narrative Recap

To own Carvana, you have to believe its online model can keep scaling profitably while its vast reconditioning and logistics network holds together. Right now, the key near term catalyst is Carvana’s ability to translate strong unit growth into sustainable margins, while the biggest risk is operational strain and cost creep in that same reconditioning footprint. The latest record quarter and the Syracuse expansion support the growth story, but do not remove that execution risk.

The most relevant recent announcement here is the plan to add Inspection and Reconditioning Center capabilities to the ADESA Syracuse site. It ties directly into Carvana’s push to expand capacity and speed up delivery, both central to its growth catalyst and its main operational risk. Syracuse fits into a broader pattern of ADESA integrations that can improve selection and logistics efficiency, but they also add complexity and upfront cost while utilization ramps.

Yet behind the strong quarter, the risk that underused reconditioning hubs could weigh on margins is something investors should be aware of...

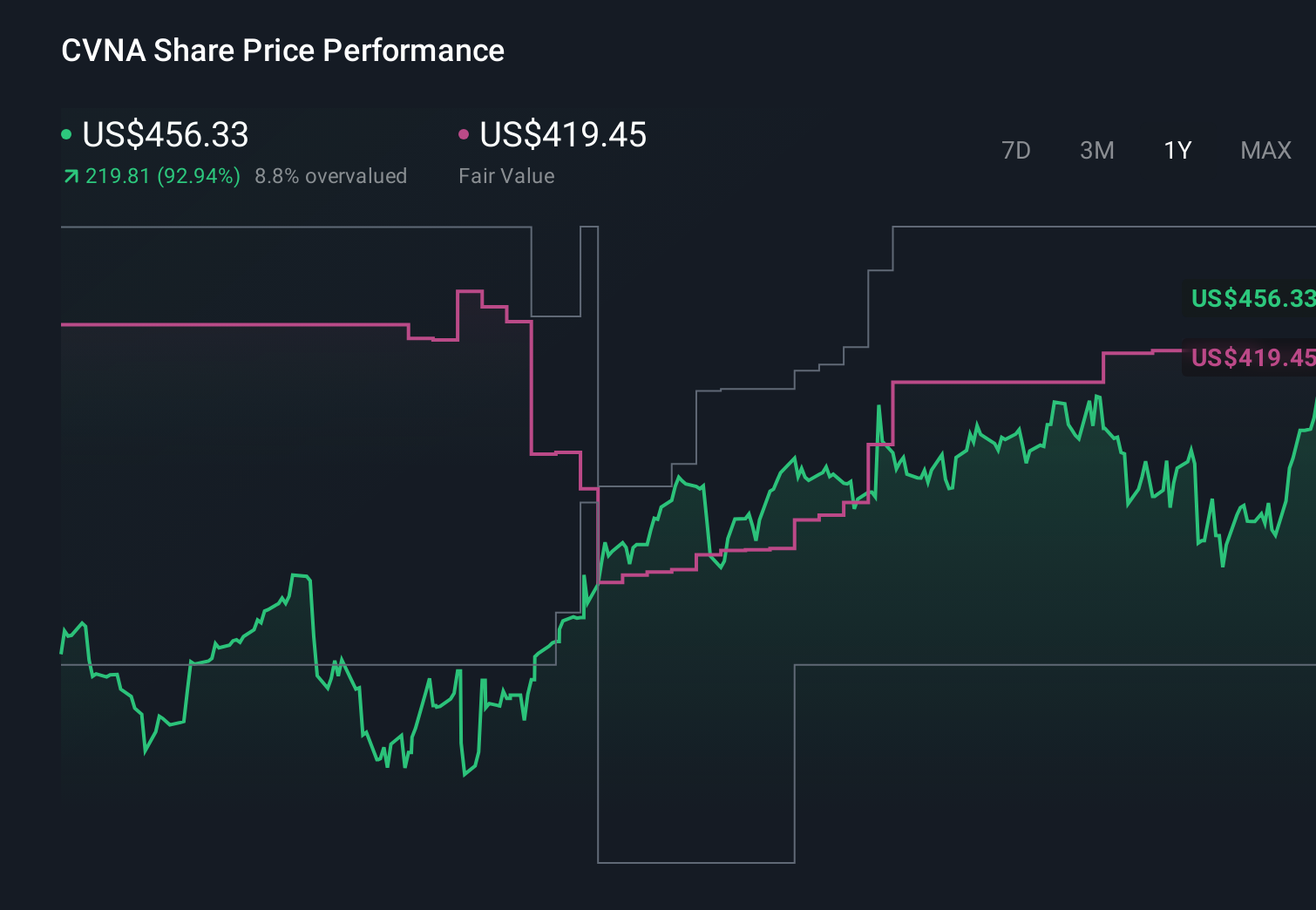

Carvana's narrative projects $40.2 billion revenue and $3.0 billion earnings by 2029.

Uncover how Carvana's forecasts yield a $428.50 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the lowest priced analysts were assuming Carvana’s revenue would reach about US$38.4 billion and earnings US$1.7 billion by 2029, yet they still saw margin pressure and capital intensity as key threats, reminding you that even with strong recent results, reasonable people can look at the same numbers and reach very different conclusions about what happens next.

Explore 13 other fair value estimates on Carvana - why the stock might be worth as much as 37% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.