Carvana (CVNA) Is Down 8.9% After Expanding Into EV Partnerships And New-Car Franchises - What's Changed

Carvana CVNA | 0.00 |

- In recent months, Carvana acquired a warrant to buy shares in Jeff Bezos‑backed EV startup Slate Auto and moved into new car sales, reportedly purchasing multiple Stellantis dealerships as it broadens beyond its core used car marketplace.

- This push into EV exposure and franchised new-car retailing marks a meaningful shift in how Carvana may source, sell, and finance vehicles across its platform.

- Next, we’ll examine how Carvana’s expansion into new car sales and its Slate Auto warrant may reshape the existing investment narrative.

Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

Carvana Investment Narrative Recap

To own Carvana, you have to believe its online model, reconditioning network, and financing engine can keep attracting car buyers while supporting improving profitability. The latest Slate Auto warrant and reported move into franchised new car sales could influence how quickly Carvana can source vehicles and broaden its customer reach, but the more immediate focus for many shareholders still sits on execution at ADESA sites and the risk that insider selling and recent share price weakness signal concerns around near term performance.

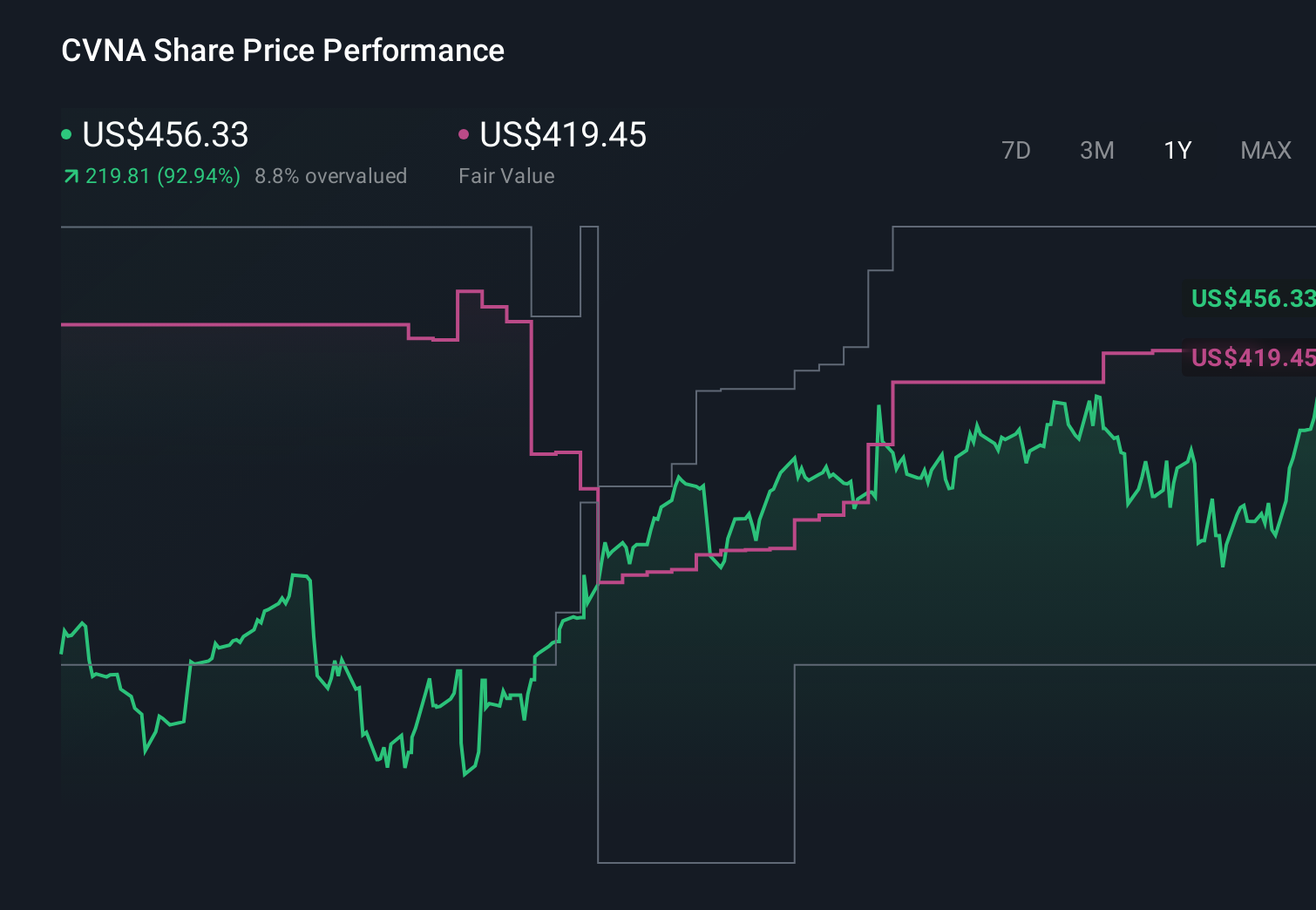

Among recent announcements, the build out of Inspection and Reconditioning Center capabilities at ADESA Chicago and Syracuse is most relevant. These projects directly affect Carvana’s ability to process more units efficiently, which ties into the same growth and margin story that investors are weighing against the new EV exposure and dealership acquisitions, especially as the stock has fallen about 15% over the past month while analysts’ consensus fair value remains materially higher.

Yet against this expansion story, investors should be aware of the possibility that rising compliance and data privacy demands could materially affect Carvana’s digital model...

Carvana's narrative projects $44.1 billion revenue and $2.9 billion earnings by 2029.

Uncover how Carvana's forecasts yield a $92.90 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenues of about US$50,000,000,000 and earnings of US$3,700,000,000 by 2029, which is a far more upbeat view than consensus. When you compare that to concerns about higher compliance and data privacy burdens, you can see how wide the gap is between different risk and reward stories, and why this latest EV and new car push could shift both bullish and cautious narratives in different ways.

Explore 10 other fair value estimates on Carvana - why the stock might be worth over 4x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.