Carvana (CVNA) Is Up 7.1% After BofA Downgrade And Stock Split News Has The Bull Case Changed?

Carvana CVNA | 371.61 | -0.70% |

- In early April 2026, Bank of America downgraded Carvana from Buy to Neutral, citing higher oil prices, rising interest rates, and pressure on profit per vehicle as key headwinds for its used-car e-commerce model.

- At the same time, Carvana moved ahead with a planned 5-for-1 stock split and expansion of its same-day delivery service into major markets, highlighting management’s confidence even as macroeconomic pressures and governance debates draw investor scrutiny.

- We’ll now examine how Bank of America’s downgrade, focused on oil and interest rate pressures, might reshape Carvana’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Carvana Investment Narrative Recap

To own Carvana, you have to believe its e commerce model can keep scaling even when fuel and financing costs are less friendly. Right now, the key near term catalyst is execution around unit volumes and margins in upcoming earnings, while the biggest risk is that higher gas prices and interest rates weigh more heavily on its core customers and delivery economics than expected. Bank of America’s downgrade directly speaks to that risk and is likely material to the short term story.

Against that backdrop, the proposed 5 for 1 stock split stands out. It does not change Carvana’s fundamentals, but it comes as analysts debate how rising oil and rates could affect demand, margins, and valuation multiples. For investors watching earnings and unit growth as primary catalysts, the split mainly matters for liquidity and access, while the macro headwinds flagged in the downgrade sit much closer to the heart of the thesis.

Yet even with all this optimism, investors still need to be aware that Carvana’s elevated debt could...

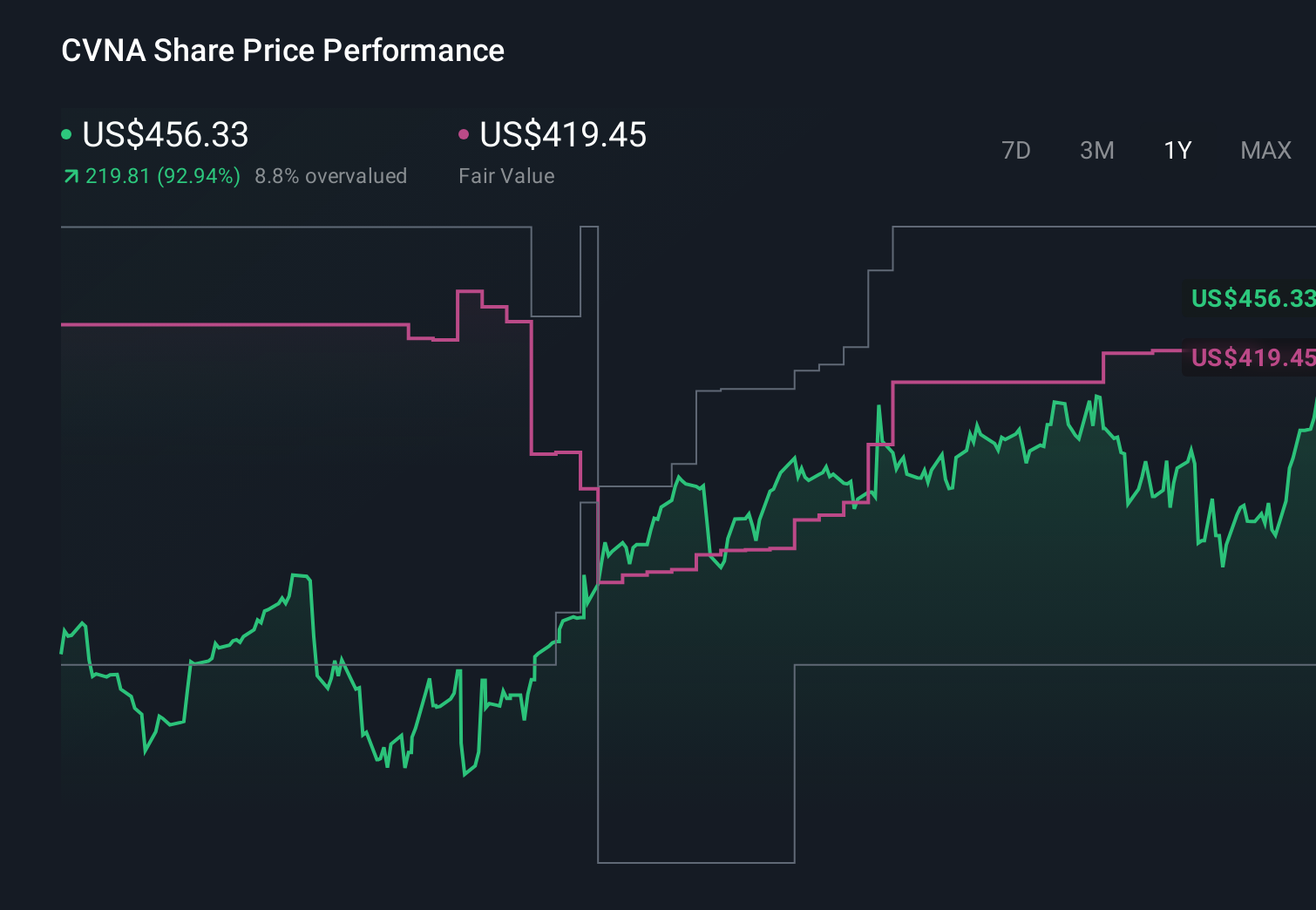

Carvana's narrative projects $40.2 billion revenue and $3.0 billion earnings by 2029. This requires 25.6% yearly revenue growth and a roughly $1.6 billion earnings increase from $1.4 billion today.

Uncover how Carvana's forecasts yield a $428.50 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously modeling Carvana to reach about US$48.3 billion in revenue and US$3.9 billion in earnings by 2029, which is far more bullish than consensus and assumes debt and competitive pressures remain manageable despite shocks like rising oil and higher rates, highlighting just how differently you and other investors might weigh these risks and potential rewards as new information comes in.

Explore 14 other fair value estimates on Carvana - why the stock might be worth as much as 54% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 58 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.