Carvana (CVNA) Valuation Check After Strong Revenue Growth And Volatile Share Price Reaction

Carvana Co. Class A CVNA | 320.22 332.08 | +1.06% +3.70% Post |

Carvana (CVNA) is back in focus after its latest results showed quarterly and full year revenue and net income figures that were well above the prior year, alongside an updated long term growth plan.

Despite the strong earnings headlines, the share price has been volatile, with a 30 day share price return of 18.35% and a year to date share price decline of 16.35%. At the same time, the 1 year total shareholder return of 43.63% and very large 3 year total shareholder return suggest longer term momentum has been much stronger than recent trading implies.

If Carvana’s swings have you thinking about where else growth stories might emerge, this could be a good moment to check our 19 top founder-led companies as potential next ideas to research.

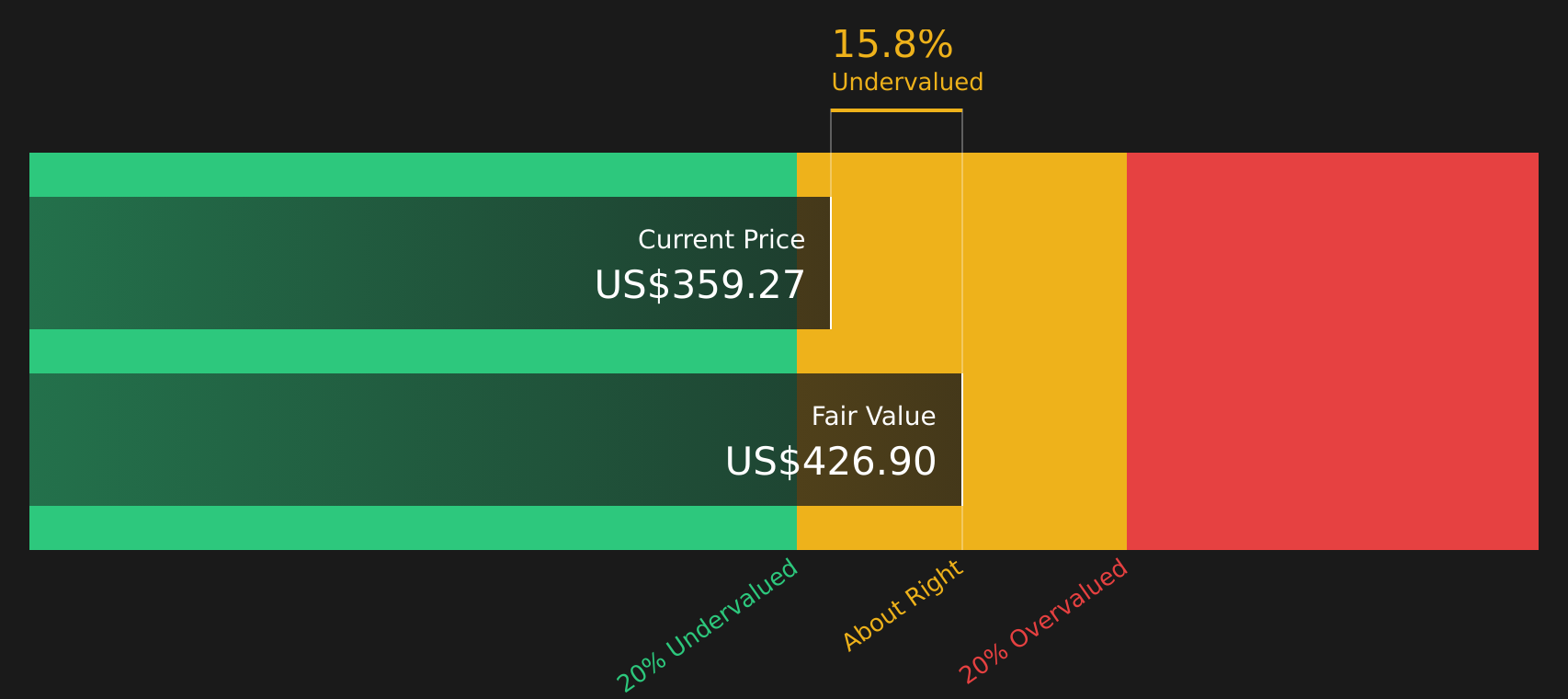

With revenue at US$20.3b, net income at US$1.4b and the share price well below the average analyst target, the real question is whether Carvana is still mispriced or if the market already assumes years of growth ahead?

Most Popular Narrative: 319.7% Overvalued

Carvana closed at $334.81, while the most followed narrative on the stock pegs fair value at $79.77, creating a wide gap that frames the debate.

The narrative for this quarter is "Peak Leverage." After a 2025 where CVNA was one of the top performers in the S&P 500, analysts are looking for more than just a "beat." They are looking for proof that Carvana can maintain its $7,000+ Gross Profit per Unit (GPU) while aggressively scaling volume. The whisper number is $1.10 EPS, a massive leap from the survival days of 2023. However, the elephant in the room is the January short report that alleged aggressive accounting regarding related-party transactions. This earnings call is not just a financial update; it is a defensive stand. CEO Ernie Garcia III needs to provide a "clean" bridge of cash flow to address the skeptics. If management can show that same-day delivery rollouts are lowering fulfillment costs rather than primarily increasing marketing spend, the "short squeeze" momentum could reignite.

Want to see what keeps this fair value anchored around one fifth of the current price? The narrative focuses on margin durability, future earnings power, and a premium profit multiple that is closer to a software company than a traditional car dealer. Curious which specific growth and profitability assumptions would need to align for that gap to close? The full story connects those dots in detail.

Result: Fair Value of $79.77 (OVERVALUED)

However, this story can shift quickly if the accounting concerns resurface, or if margins fail to support expectations for premium profit multiples.

Another Take: DCF Points in the Opposite Direction

While the most popular narrative sees Carvana as overvalued at a fair value of $79.77, our DCF model provides a different perspective, with an estimate of $422.46 that is above the current $334.81 share price. When two approaches disagree this much, which one would you lean on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Carvana for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of confidence and concern around Carvana leaves you undecided, act while the data is fresh and shape your own view by checking 4 key rewards and 1 important warning sign.

Ready for more investing ideas?

If Carvana has sharpened your thinking, do not stop here. Broaden your watchlist now with fresh ideas sourced directly from the Simply Wall Street Screener.

- Target resilient value by reviewing companies our screener flags as 46 high quality undervalued stocks that might warrant a closer look.

- Strengthen your income stream by scanning for reliable payers in our collection of 15 dividend fortresses.

- Prioritise resilience by focusing on companies highlighted in our 77 resilient stocks with low risk scores that may better suit a steadier approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.