Carvana (CVNA) Valuation In Focus After Earnings Beat And Confident Outlook For 2026

Carvana CVNA | 0.00 |

Carvana stock in focus after earnings surprise

Carvana (CVNA) is back in the spotlight after first quarter 2026 earnings came in ahead of estimates, with retail vehicle sales driving revenue and management signaling confidence in sales and adjusted EBITDA for the rest of the year.

The stock has been volatile, with the share price up 6.9% over the past week and 12.9% over the past 90 days but down 8.8% year to date. The three year total shareholder return is extremely high, suggesting longer term investors have already experienced a very strong run, and recent earnings and lower logistics costs are now shaping shorter term momentum.

If Carvana’s moves have you thinking about where else growth or recovery stories might be emerging, this is a good moment to scan 20 top founder-led companies

With Carvana now valued at US$73 a share and sitting about 27% below the average analyst price target of roughly US$92.90, investors may ask whether there is still a buying opportunity or whether potential future growth is already reflected in the current price.

Most Popular Narrative: Fairly Valued

Carvana’s most followed narrative on Simply Wall St assigns a fair value that effectively matches the current share price of $73, so the focus shifts to how sustainable that profile looks over time rather than a clear discount or premium call.

There are growing concerns among some market observers that Carvana's business model may be masking deeper financial instability. The company has a long history of operating with negative cash flow followed with rapid debit expansion, and unusually aggressive revenue recognition practices that raise questions about the sustainability of its margins. Analysts have also noted that Carvana's reported improvements in profitability often coincide with accounting adjustments rather than genuine operational strength, suggesting the possibility of earnings "smoothing out". Additionally, the firm’s reliance on securitizing subprime auto loans creates opacity around the true quality of its assets; rising delinquencies in the used car loan market increase the risk that these securities are overvalued. When a company simultaneously carries heavy debt, thin cash reserves and complex financial structures that are difficult for outside investors to verify, it breeds skepticism.

Want to see what sits behind that skepticism according to Sirupy? The narrative leans heavily on profitability quality, funding structure and how future margins are built into the fair value.

Result: Fair Value of $0 (ABOUT RIGHT)

However, any clear SEC resolutions or stronger, verifiable cash flow trends could quickly shift sentiment away from the more skeptical fair value argument.

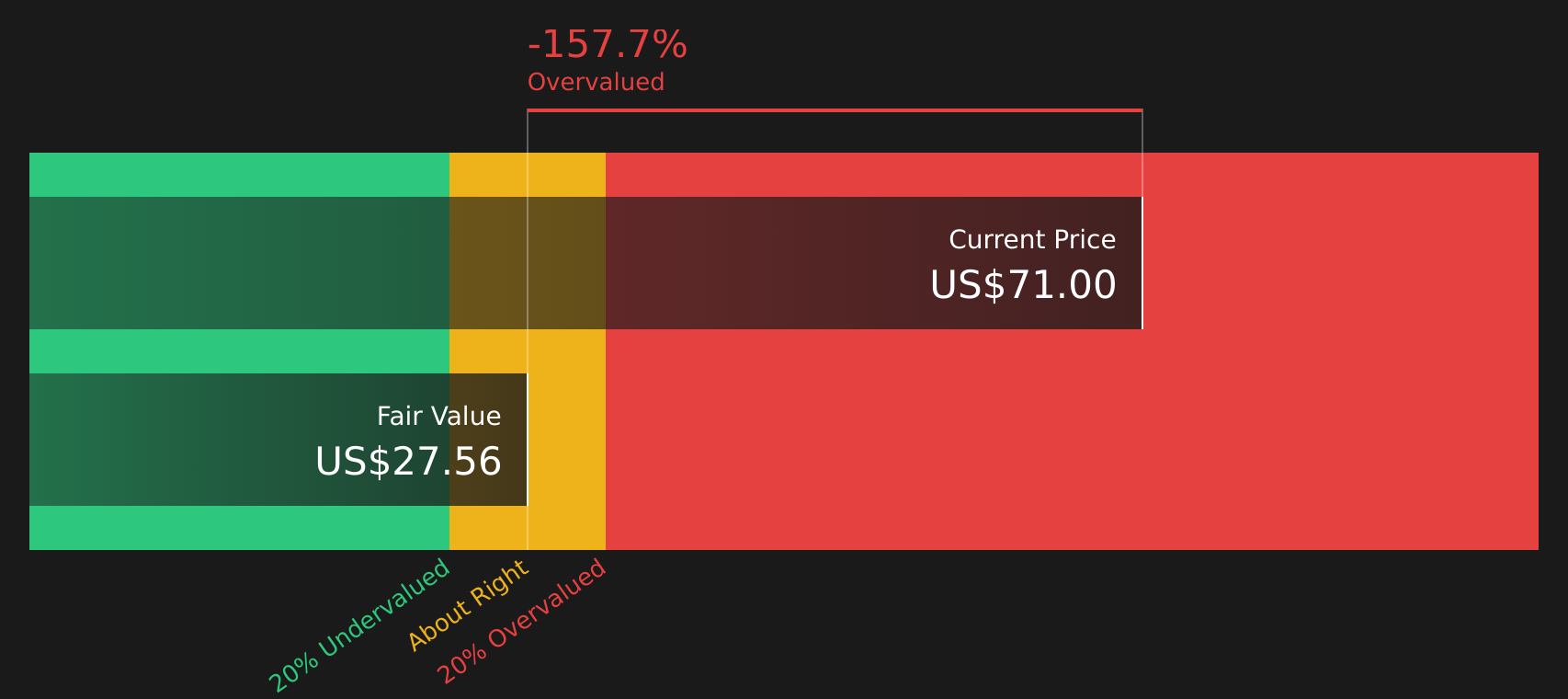

Another View: Cash Flows Paint A Different Picture

While the user narrative pegs fair value roughly in line with the current $73 share price, Simply Wall St’s DCF model tells a different story. It places Carvana’s future cash flow value at $27.56 per share, which suggests the stock is currently priced well above that estimate.

For investors, that gap raises a simple question: are you more comfortable anchoring on accounting earnings and sentiment, or on a cash flow model that points to less room for error at today’s price?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Carvana for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed views on Carvana so far? Use this moment to review the key data points yourself, then weigh up the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Carvana has you rethinking your watchlist, this is the moment to widen your scope and line up a few fresh ideas for your next move.

- Target resilient compounding potential by focusing on companies that combine quality and attractive pricing using the 46 high quality undervalued stocks.

- Prioritise sleep-at-night stability with stocks that show financial strength through the solid balance sheet and fundamentals stocks screener (46 results).

- Spot tomorrow's potential standouts before the crowd by checking the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.