Carvana Stock And Auto Retailers Set For Cheaper Vehicle Imports

Carvana CVNA | 0.00 |

Tariff changes on imported vehicles are reshaping the playing field for auto-related stocks, and some could be better placed than others to respond. With import duties on both used and new vehicles cut sharply, the economics of bringing cars into key markets may shift for companies that import, distribute, and retail automobiles. At the same time, trade facilitation efforts and ongoing smuggling concerns keep the picture complex. This article examines what the new conditions could mean for investors and highlights 3 stocks exposed to this news that appear positioned as potential beneficiaries of higher vehicle import activity.

Carvana (CVNA)

Overview: Carvana runs a U.S. e-commerce platform where you can buy, finance, and sell used cars entirely online, supported by its own logistics, reconditioning centers, and a distinctive delivery and pickup experience. It also operates digital auction sites that connect dealers with wholesale inventory.

Operations: Carvana generates all of its US$22.5b in revenue from U.S. retail gasoline and auto dealer activity.

Market Cap: US$75.7b

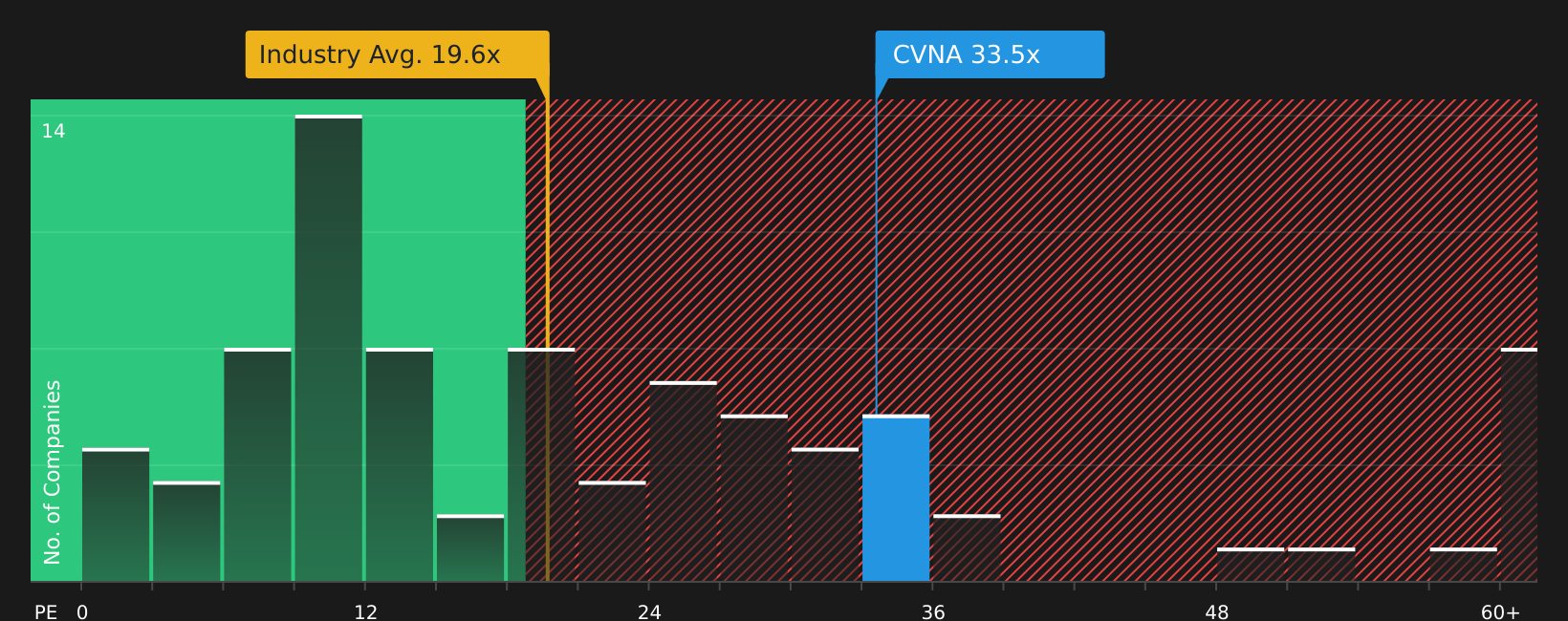

Investors looking at auto retailers after the tariff cuts may find Carvana hard to ignore, as a fully online used car platform that could see stronger demand if imported vehicles become cheaper and shoppers focus on value. The company combines rapid earnings growth, a high 41.6% ROE, and expanding margins with a premium P/E multiple and heavy reliance on external borrowing, so expectations are already high and the balance sheet adds risk. Rising advertising spend, ADESA auction expansion, and new retail models around test drives and new-car sales add more moving parts. The real question is whether Carvana’s execution and unit economics justify both its growth narrative and that premium pricing.

Carvana’s premium P/E and 41.6% ROE suggest something powerful is happening beneath the headline growth story, yet its heavy borrowing raises tough questions about durability, so tap into the 3 key rewards and 2 important warning signs

Motorpoint Group (LSE:MOTR)

Overview: Motorpoint Group is a UK based omnichannel vehicle retailer that sells nearly new cars and commercial vehicles under five years old with low mileage, supported by its own online auction platform Auction4Cars.com and a range of motor related services such as finance, warranties and insurance.

Operations: Motorpoint Group generates £1.27b of revenue, with £1.13b from Retail and £137.8m from Wholesale operations, all in the United Kingdom.

Market Cap: £101.5m

Motorpoint Group stands out in the tariff story because cheaper imported vehicles can ease supply constraints and support the affordability focus that management keeps stressing, particularly below the £12,000 price point where many of its newer customers sit. Earnings rebounded 75% over the past year and forecasts indicate expectations of earnings growth above 20% a year, with ROE already high at 21.5%. The stock trades on a richer P/E and above some cash flow based value estimates, which raises questions about how much optimism is already in the price. Dependence on higher risk external funding also adds a layer of financial risk, so investors may weigh the appeal of a recovering dealer with stronger fundamentals and improving used car supply against valuation and funding considerations.

Motorpoint Group’s rebound, higher ROE and focus on affordability hint that the story might be less stalled than the share price suggests. Check the analyst forecasts for Motorpoint Group before drawing firm conclusions about how far this recovery can really go.

XPeng (XPEV)

Overview: XPeng is a Guangzhou based electric vehicle company that designs and sells smart EVs such as sedans, SUVs and MPVs, while layering in its own operating system, driver assistance software and services like charging, maintenance and financing.

Operations: XPeng generates CN¥73.9b in revenue from auto manufacturing, all from customers in the People’s Republic of China.

Market Cap: US$12.5b

XPeng sits at the crossroads of cheaper vehicle imports and rising interest in smart EVs, offering investors a mix of potential upside and clear execution risk. The company is still loss making, with all liabilities funded by higher risk external sources, and analyst forecasts currently indicate expectations of profitability within 3 years, ROE improvement and overseas expansion contributing more than 20% of revenue. Its focus on proprietary AI hardware, robotaxis and humanoid robots, plus partnerships such as Volkswagen, points to multiple ways to grow software and service income if these technologies scale. With tariffs falling, a relatively low P/S and fresh models like MONA and the X9 gaining attention, the key question is whether XPeng can turn strong product momentum into durable profits before competition and funding needs catch up.

XPeng’s push into AI hardware, robotaxis and humanoid robots could be masking a very different earnings path, so walk through the analyst forecasts for XPeng to see what analysts might be missing about the next phase.

The three stocks covered here are only a starting point, and the full Automobile and Auto Dealership Sector screener surfaces 6 more companies with equally compelling import, distribution, and retail stories that line up with the tariff and vehicle flow themes discussed above. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you, so you can focus on the highest conviction opportunities in this corner of the market.

Take Control of Your Investment Journey

If Carvana or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Auto Stocks?

Fresh ideas do not stay under the radar for long. New themes gain momentum, prices move, and the best entry points get caught early, before the crowd, so consider acting while opportunities are still emerging.

- Spot early turnarounds by scanning the 18 high quality undiscovered gems that are quietly building strong fundamentals before attention and trading volumes start rising.

- Target durable cash flows with the 8 dividend fortresses designed to surface companies prioritizing reliable income while prices are still dropping below many income investors’ radars.

- Explore the next infrastructure build out using the 35 power grid technology and infrastructure stocks highlighting businesses positioned around grid upgrades while the story is still developing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.