CATRION Catering Holding (TADAWUL:6004) Is Looking To Continue Growing Its Returns On Capital

CATRION 6004.SA | 69.60 | -0.57% |

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at CATRION Catering Holding (TADAWUL:6004) and its trend of ROCE, we really liked what we saw.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for CATRION Catering Holding:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

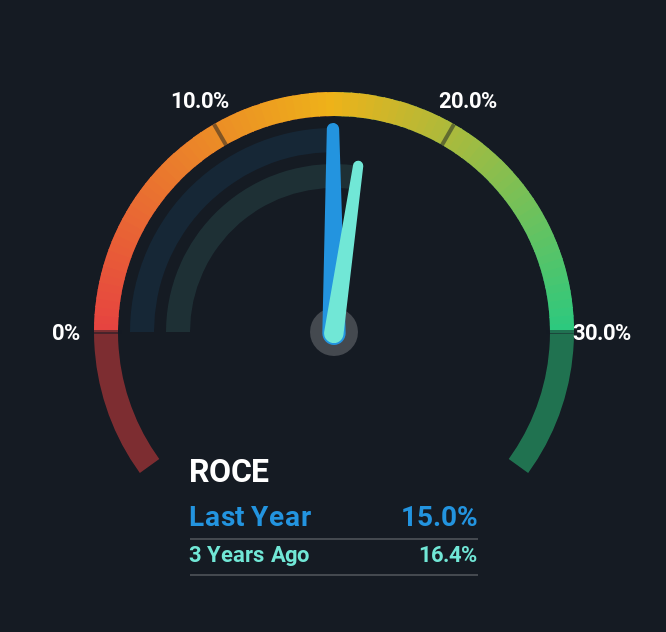

0.15 = ر.س360m ÷ (ر.س3.2b - ر.س749m) (Based on the trailing twelve months to September 2025).

Therefore, CATRION Catering Holding has an ROCE of 15%. In absolute terms, that's a pretty standard return but compared to the Commercial Services industry average it falls behind.

In the above chart we have measured CATRION Catering Holding's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering CATRION Catering Holding for free.

So How Is CATRION Catering Holding's ROCE Trending?

CATRION Catering Holding has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 15% which is a sight for sore eyes. And unsurprisingly, like most companies trying to break into the black, CATRION Catering Holding is utilizing 59% more capital than it was five years ago. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, both common traits of a multi-bagger.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 24%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

What We Can Learn From CATRION Catering Holding's ROCE

Overall, CATRION Catering Holding gets a big tick from us thanks in most part to the fact that it is now profitable and is reinvesting in its business. Considering the stock has delivered 13% to its stockholders over the last five years, it may be fair to think that investors aren't fully aware of the promising trends yet. Given that, we'd look further into this stock in case it has more traits that could make it multiply in the long term.

If you'd like to know more about CATRION Catering Holding, we've spotted 2 warning signs, and 1 of them is a bit unpleasant.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.