Celebration Key Expansion Might Change The Case For Investing In Carnival (CCL)

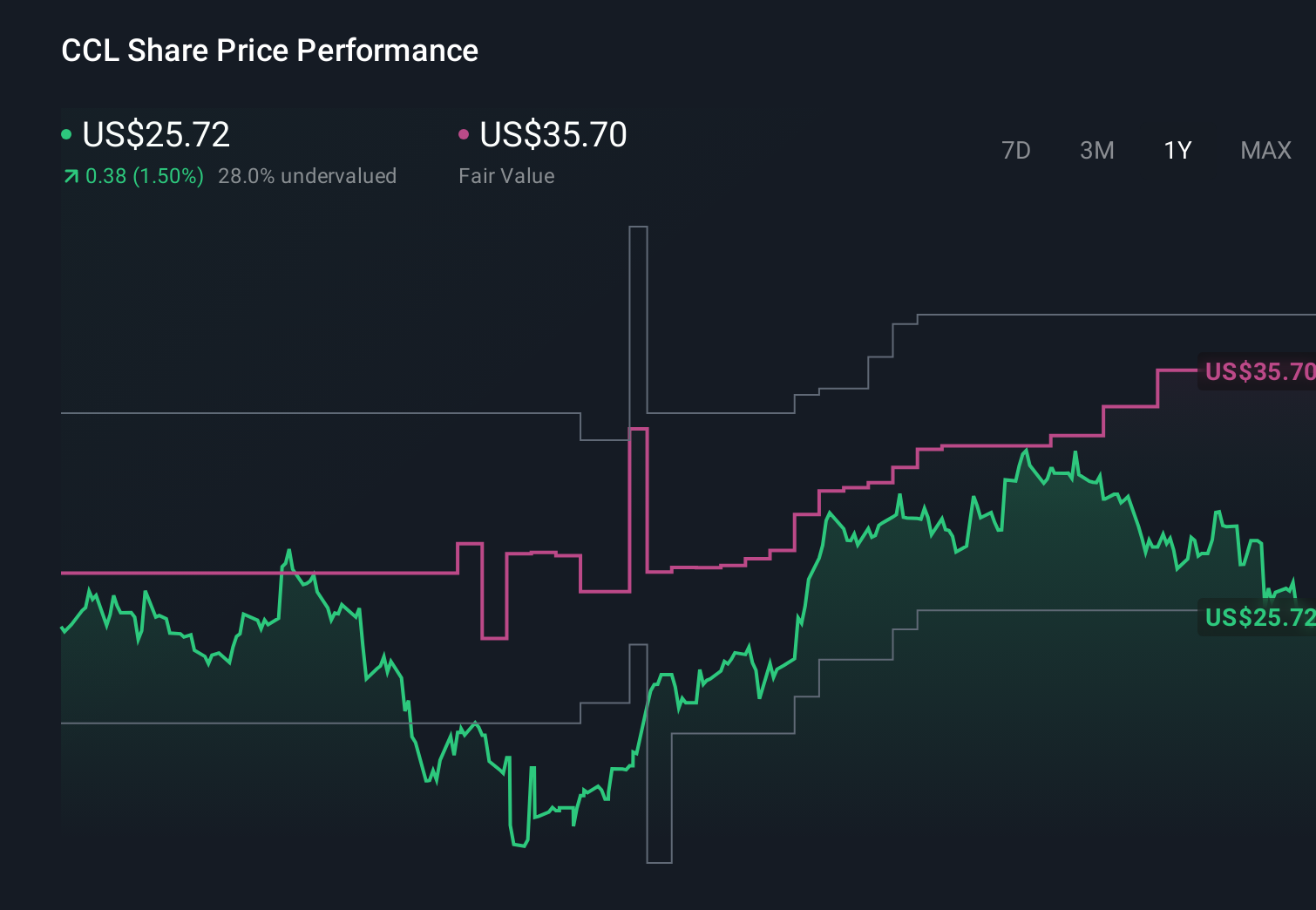

Carnival Corporation Ltd. CCL | 0.00 |

- Carnival Corporation has completed the Celebration Key pier extension on Grand Bahama Island, adding two new berths so the destination can now host four ships and more than 13,000 guests per day while supporting hundreds of additional annual ship calls and guest arrivals.

- This build-out reinforces Celebration Key as a core asset in Carnival’s Caribbean deployment, underpinning its push toward higher guest volumes, stronger onboard spending and greater control over the end-to-end cruise experience.

- We’ll now examine how Celebration Key’s expanded capacity and role within Carnival’s Caribbean network could influence the company’s broader investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Carnival Investment Narrative Recap

To own Carnival, you need to believe its focus on owned destinations, onboard spend, and disciplined capacity can offset high debt and capital needs. Celebration Key’s pier extension supports the near term catalyst of higher guest volumes and spending, while the biggest current risk remains the balance sheet and refinancing demands. The expansion itself does not materially change that risk profile, but it reinforces the importance of execution on yield and cash generation.

The most relevant recent announcement here is Carnival’s slightly raised 2026 earnings guidance to US$2.22 per share. That guidance, issued just days before the Celebration Key update, underlines how management is already counting on better per share earnings from factors like buybacks and operational performance. Celebration Key’s added capacity now sits alongside those efforts, potentially giving the company more levers to support earnings if demand and pricing hold up.

But even with Celebration Key’s success, investors should also be aware of how Carnival’s sizeable debt could affect...

Carnival's narrative projects $30.5 billion revenue and $4.0 billion earnings by 2029. This requires 3.8% yearly revenue growth and an earnings increase of about $0.9 billion from $3.1 billion today.

Uncover how Carnival's forecasts yield a $35.60 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Carnival to reach about US$31.0 billion in revenue and US$4.4 billion in earnings by 2029, so Celebration Key’s expansion could either support that bullish path or expose how sensitive those assumptions are to risks like rising cruise costs and changing traveler preferences.

Explore 10 other fair value estimates on Carnival - why the stock might be worth just $28.70!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carnival research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.