Celsius Holdings (CELH) Could Be 40% Undervalued Following Legal Heat And Strong Growth

Celsius Holdings, Inc. CELH | 0.00 |

Celsius Holdings (CELH) is back in focus after fresh legal and regulatory actions around alleged channel stuffing and youth marketing, which coincided with recent revenue growth and a sizeable U.S. energy drink market share.

Recent headlines around lawsuits and regulatory investigations have come alongside sharp share price swings, with Celsius Holdings posting a 1 month share price return of 17.88% and a year to date share price return that is down 30.55%. The 1 year total shareholder return is down 28.78%, suggesting recent momentum has picked up after a weaker period for long term holders.

If this mix of legal risk and growth potential has your attention, it can also be useful to look beyond Celsius and see what else is moving in related areas by checking out 20 top founder-led companies

So, with Celsius Holdings trading at US$33.16 against an average analyst price target of US$58.24 and some models still flagging the stock as expensive on earnings, is this a genuine opportunity or is potential future growth already reflected in the price?

Most Popular Narrative: 40.2% Undervalued

According to the most followed narrative on Celsius Holdings, a fair value of $55.43 versus the latest close at $33.16 implies a wide valuation gap that hinges on how investors view its growth, margins, and distribution story.

In 2010, Celsius Holdings (CELH) was generating roughly US$5 million in annual revenue, a forgotten energy drink with niche distribution in Scandinavian gyms and a handful of US health food stores. By the end of 2025, the company had crossed US$2 billion in trailing twelve-month revenue and acquired two major energy drink brands. It secured PepsiCo as both its primary distributor and an 11% equity holder. Most retail investors only discovered this stock near the peak in 2023.

The fair value narrative on Celsius Holdings leans heavily on rapid earnings compounding, expanding profitability, and a richer future profit multiple that assumes the Pepsi distribution footprint and acquired brands support a very different earnings profile from today. Curious which growth and margin assumptions have the biggest impact on that $55.43 figure, and how sensitive the story is to even small changes in those inputs.

Result: Fair Value of $55.43 (UNDERVALUED)

However, Celsius Holdings still faces real pressure points, including the shareholder lawsuit over past disclosures and the risk that Alani Nu or Rockstar integration weighs on margins.

Another View on Celsius Holdings Valuation

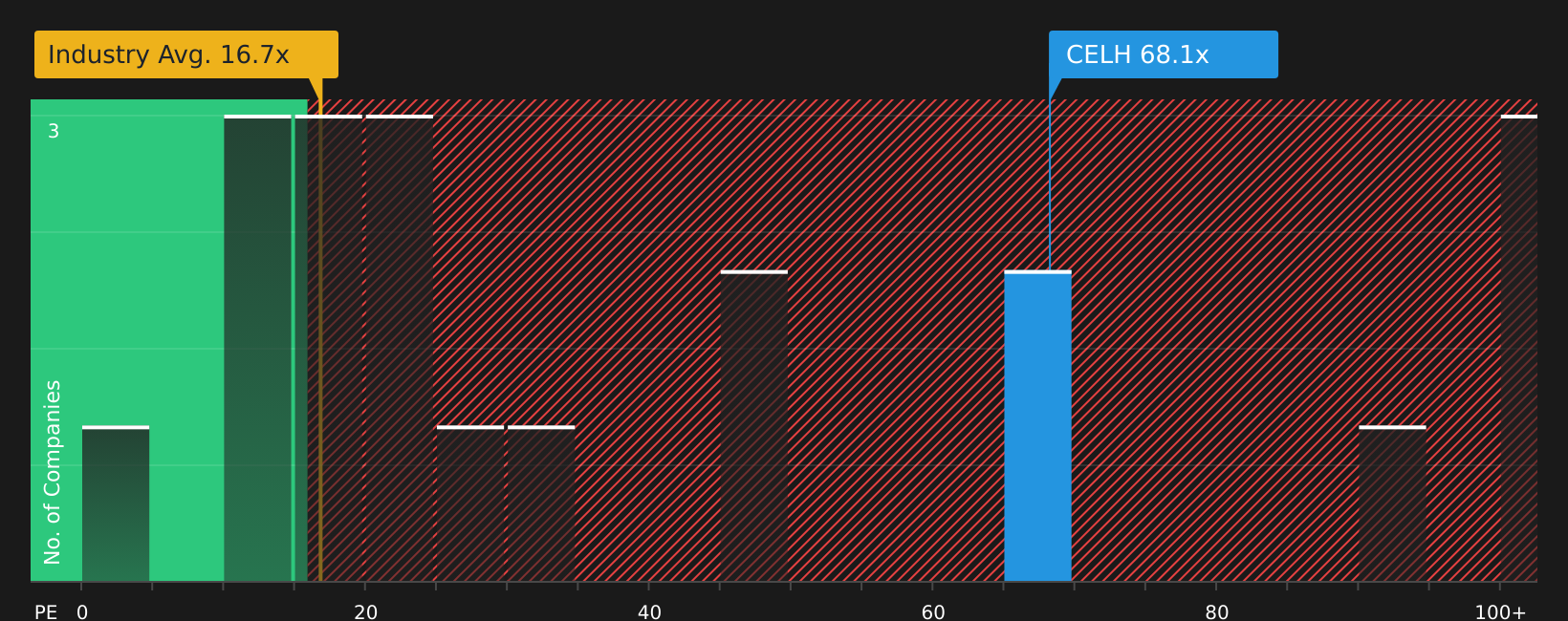

While the user narrative points to a fair value of $55.43 and labels Celsius Holdings as undervalued, the market is currently assigning a P/E of 74x. That is far above the Global Beverage industry at 17x, the peer average at 52.4x, and an estimated fair ratio of 29x. This suggests a wide gap that could either close through earnings growth or a lower share price. Which side of that adjustment do you think is more realistic?

For a closer look at how the numbers stack up against this earnings multiple view, take a look at See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on Celsius Holdings clearly split between concern and optimism, now is a good time to review the underlying data and pressure test both sides. To weigh the balance of upside potential against the legal and operational questions being raised, start by working through the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Celsius Holdings?

If the Celsius Holdings story has you thinking more seriously about where you put your capital next, do not stop at a single stock when you can compare many.

- Target resilient income by reviewing companies that appear built to keep paying, using the 7 dividend fortresses.

- Spot potential value opportunities by screening for stocks that look attractively priced relative to quality fundamentals through the 44 high quality undervalued stocks.

- Prioritize capital preservation by focusing on companies that show stronger downside protection with the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.