Celsius Holdings (CELH) Faces A Fresh Valuation Test As Its Growth Story Meets Share Price Weakness

Celsius Holdings, Inc. CELH | 0.00 |

Recent Performance Snapshot for Celsius Holdings Stock

Celsius Holdings (CELH) has drawn fresh attention after a choppy stretch for the stock, with shares closing at US$28.52 and sitting well below their level at the start of the year.

Over the past month, the stock is down about 4%, with a decline of roughly 16% over the past 3 months and a year to date drop of about 40%, leaving the 1 year total return lower by around 37%.

For Celsius Holdings, the recent 7 day share price return, down 7.4%, continues a broader loss of momentum, with the year to date share price return down 40.3% and the 3 year total shareholder return down 42.5%.

If the recent pullback has you reassessing growth ideas in your portfolio, this could be a good moment to scan a wider field of opportunities, including 20 top founder-led companies

With Celsius Holdings shares trading sharply below recent highs, while revenue and net income have both increased, the key question is whether the current valuation already reflects that progress or whether the recent weakness suggests a potential buying opportunity that markets have not fully priced in.

Most Popular Narrative: 48.5% Undervalued

At a last close of $28.52 against a narrative fair value of $55.43, Celsius Holdings is framed as materially undervalued in a detailed story that stretches far beyond recent price swings.

A 17-Year Story That Most Investors Only Discovered in the Last Three

In 2010, Celsius Holdings (CELH) was generating roughly US$5 million in annual revenue, a forgotten energy drink with niche distribution in Scandinavian gyms and a handful of US health food stores.

This narrative, according to JD009, pulls together growth in earnings, expected profitability and a premium consumer position, then layers on a valuation multiple usually reserved for larger consumer brands and fast growing consumer companies. If you want to see how those ingredients combine into a specific fair value for Celsius Holdings, the full story goes step by step through the assumptions and the tension between recent share price weakness and that higher estimate.

Result: Fair Value of $55.43 (UNDERVALUED)

However, Celsius Holdings still faces real pressure points, including any setback in PepsiCo distribution or weaker returns from the Alani Nu and Rockstar acquisitions.

Another View on Celsius Holdings Valuation

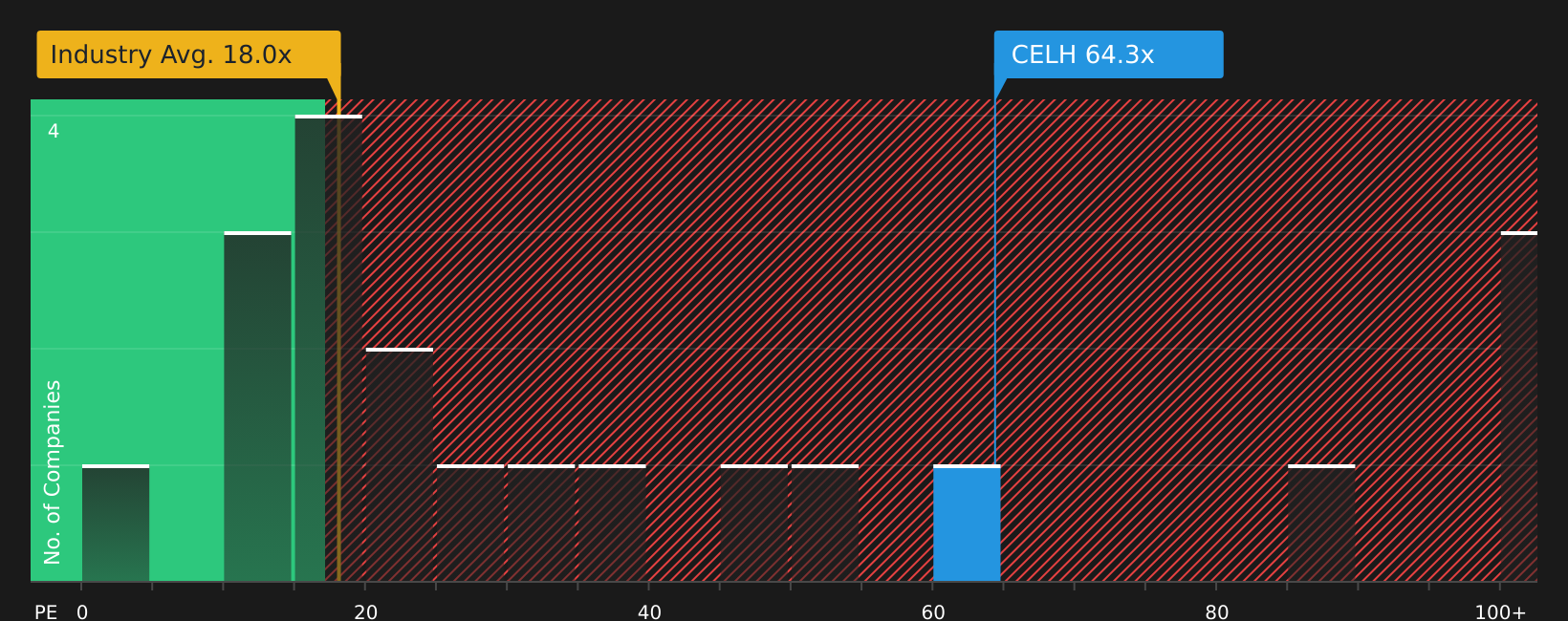

The narrative fair value of $55.43 presents Celsius Holdings as undervalued, but the current P/E of 63.7x tells a very different story. It is far above the Global Beverage industry average of 16.9x and above the fair ratio of 28.1x, which suggests meaningful valuation risk if the market moves closer to that fair ratio.

For a closer look at how this pricing compares with peers and what the gap to the fair ratio could mean in practice, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Celsius Holdings presenting both appealing growth arguments and clear valuation questions, this is a moment to move quickly, review the underlying data yourself, and weigh both sides by checking the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Celsius Holdings?

Do not stop with Celsius Holdings; broaden your watchlist now so you are not looking back later wishing you had checked a few more compelling setups.

- Target potential mispriced opportunities before others notice by checking stocks that screen as 44 high quality undervalued stocks.

- Prioritise resilience and sleep-better-at-night positions by reviewing companies in the 69 resilient stocks with low risk scores.

- Hunt for under-the-radar potential by scanning the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.