Centene (CNC) Swings To US$6.7b TTM Loss Challenging Bullish Margin Recovery Narratives

Centene Corporation CNC | 37.60 37.24 | +0.91% -0.97% Post |

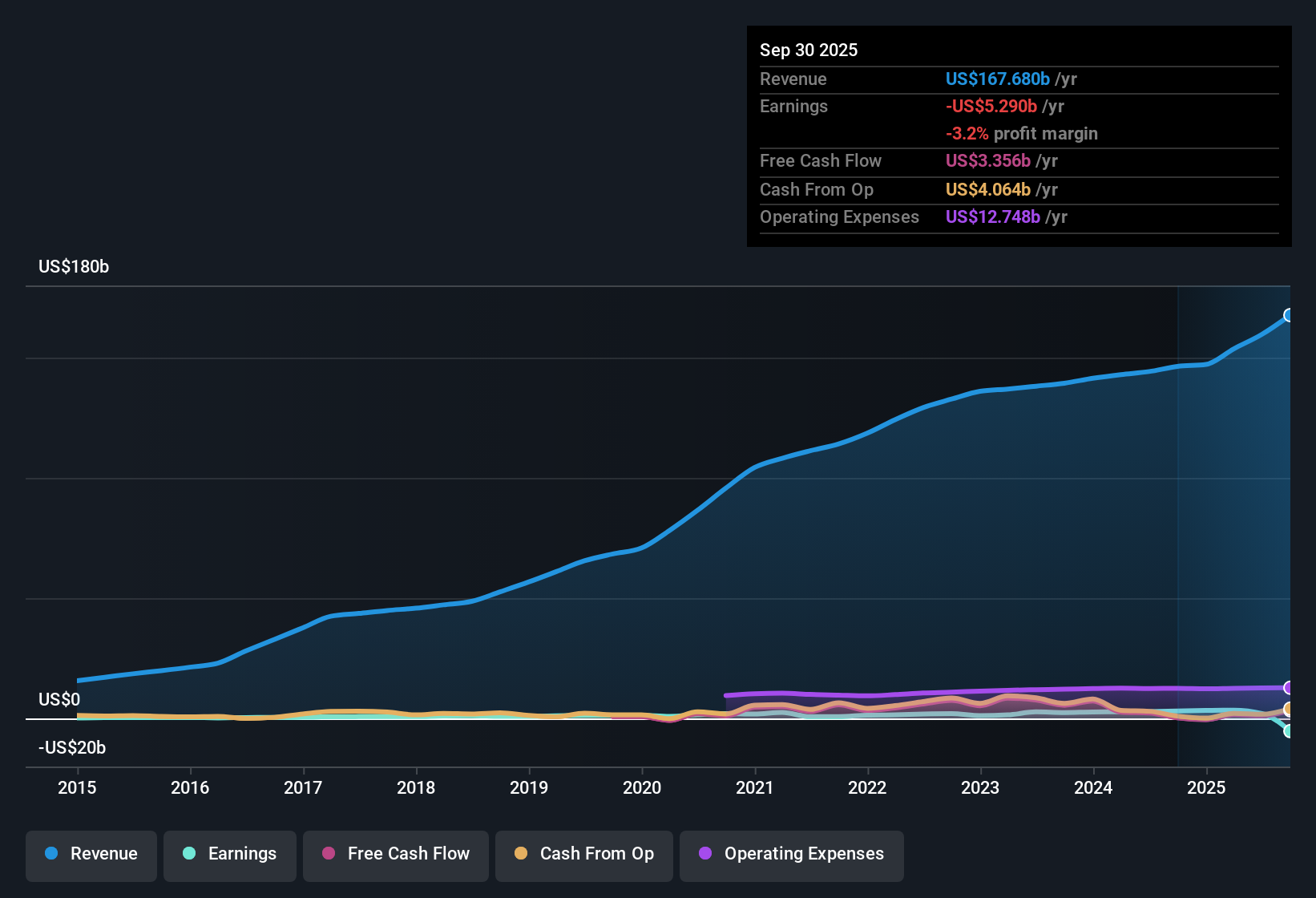

Centene (CNC) just closed out FY 2025 with Q4 revenue of US$45.1b and a basic EPS loss of US$2.24, capping a trailing twelve month period where revenue reached US$176.2b and basic EPS stood at a loss of US$13.53. The company has seen quarterly revenue move from US$36.6b in Q4 2024 and US$37.3b in Q3 2024 to the current US$45.1b and US$45.3b in Q4 and Q3 2025. Over the same periods, EPS shifted from US$0.57 and US$1.37 in those 2024 quarters to losses of US$2.24 and US$13.50 in the latest 2025 quarters. These results are likely to keep investor attention on how sustainably Centene can improve its margins from here.

See our full analysis for Centene.With the headline numbers on the table, the next step is to see how these results line up against the widely followed narratives around Centene's growth prospects, risk profile and path back to healthier margins.

US$6.7b LTM Loss Puts Profit Recovery In Focus

- Over the last twelve months, Centene generated about US$176.2b of revenue but recorded a net loss of roughly US$6.7b and basic EPS of a US$13.53 loss, compared with a US$3.3b profit and basic EPS of US$6.33 in the prior-year LTM snapshot.

- Bears often point to the multi year trend of losses growing about 19.9% each year. That view lines up with the recent swing from a US$3.5b LTM profit in early 2025 to the current US$6.7b LTM loss, even though Q1 2025 alone showed US$1.3b of net income and US$2.64 EPS.

Valuation Gap Versus DCF Fair Value

- At a share price of US$38.46, the data indicates Centene trades at about 0.1x P/S and roughly 82.2% below an internal fair value estimate, with a DCF fair value of about US$215.75.

- Supporters of the bullish view highlight the combination of low P/S versus the US Healthcare industry average of 1.3x and peers at 1.5x, and the gap to the US$215.75 DCF fair value. The recent shift from a US$3.5b LTM profit in Q1 2025 to a US$6.7b loss in Q4 2025 shows why others question how quickly that valuation thesis can be backed by the actual earnings path.

- Revenue is forecast at about 2.5% annual growth and earnings are expected to grow around 66.01% per year, which bullish investors see as a route toward closing that valuation gap.

- The fact that losses have grown about 19.9% per year over five years gives cautious investors a clear data point to weigh against those earnings forecasts.

Curious how other investors are connecting Centene's current loss profile with that wide valuation gap? Curious how numbers become stories that shape markets? Explore Community Narratives

Forecast Turn To Profit Within Three Years

- The analysis data states that revenue is forecast to grow around 2.5% per year and earnings are expected to turn positive within three years, with projected EPS and earnings growth of about 66.01% per year from the current LTM loss of US$6.7b.

- What stands out for the more bullish narrative is that these strong earnings growth forecasts are starting from a base that includes a Q3 2025 net loss of about US$6.6b and Q4 2025 loss of US$1.1b, so any improvement needs to be large enough to reverse a five year pattern where losses have increased roughly 19.9% each year.

- Supportive data points include the earlier LTM snapshots in 2024 and early 2025 that were still profitable, with net income between about US$3.1b and US$3.5b, showing the business has produced profits in the recent past.

- On the other hand, revenue growth forecasts of 2.5% per year compare with a referenced US market rate of 10.2% per year, which some investors may see as a headwind if margin repair does not move quickly enough.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Centene's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Centene's swing from prior LTM profits to a US$6.7b loss and a five year pattern of rising losses indicates that earnings stability is a key concern.

If that level of volatility makes you cautious, you may wish to consider companies that score well on resilience and consistency with our 86 resilient stocks with low risk scores for potentially steadier options.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.