Charter Communications (CHTR) Valuation Check After Spectrum WiFi 7 Extenders Launch

Charter Communications, Inc. Class A CHTR | 219.79 | +1.63% |

Charter Communications (CHTR) is back in focus after Spectrum rolled out WiFi 7 Extenders that use 6 GHz spectrum and cloud-based mesh networking to offer broader, multi-gig coverage for homes and businesses.

The WiFi 7 Extenders arrive after a tough period for investors, with the latest share price at US$187.43, a 1 day share price return of 1.75%. Over longer periods, the 90 day share price return shows a decline of 23.16%, the 1 year total shareholder return shows a decline of 46.87%, and the 5 year total shareholder return shows a decline of 69.56%. This suggests recent product news sits against weaker momentum that has built up over several years.

If this kind of connectivity upgrade has you thinking more broadly about communications and media, it could be a good moment to look across fast growing stocks with high insider ownership as a source of fresh stock ideas.

With Charter shares down sharply over 1 year and 5 years, yet trading at a discount to some analyst targets and intrinsic estimates, you have to ask: is this weakness an opportunity, or is the market already pricing in future growth?

Price-to-Earnings of 4.7x: Is it justified?

Against a long stretch of weak share price returns, Charter is trading on a P/E of 4.7x, which screens as low compared to peers and industry benchmarks.

The P/E multiple compares the current share price to earnings per share. With a figure of 4.7x, the market is attaching a relatively modest price tag to each dollar of Charter earnings. For a large US$55.1b revenue media and broadband operator that reports US$5.1b of net income, that gap between operations and valuation stands out.

Statements highlight that this 4.7x P/E is below the peer average of 22.7x and below the US Media industry average of 14.3x, which points to a strong valuation gap. The same framework suggests a fair P/E of 21.4x, a level the market could gravitate toward if sentiment and earnings expectations align more closely with this estimate.

Result: Price-to-Earnings of 4.7x (UNDERVALUED)

However, you still need to weigh risks like ongoing share price pressure, with a 46.87% 1 year total return decline and 69.56% over 5 years, and the possibility that low valuation multiples reflect concerns about Charter’s long term competitive position and capital intensity.

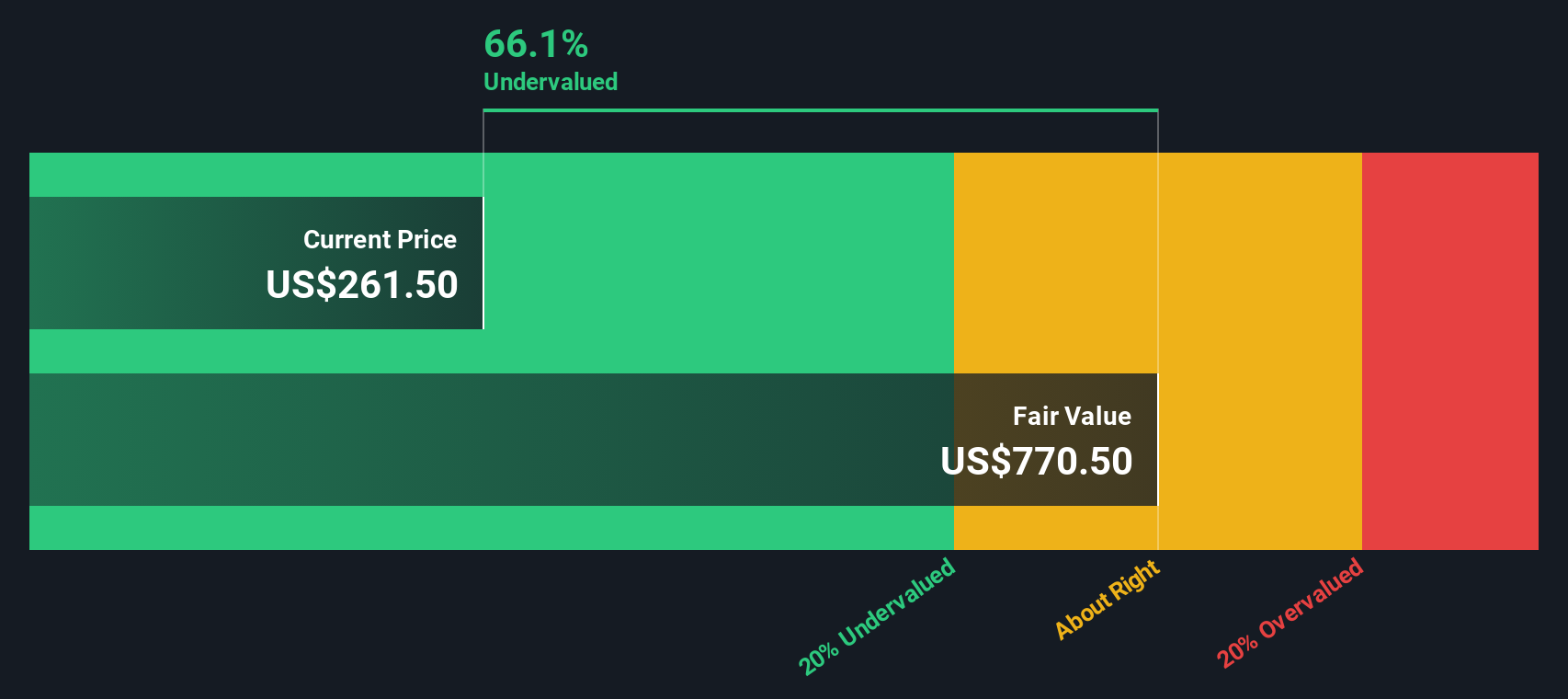

Another View: Cash Flows Tell an Even Bigger Story

If you look beyond earnings and focus on cash flows, our DCF model presents a different perspective. On that basis, Charter at US$187.43 is compared with an estimated future cash flow value of US$580.12.

A gap of this size can signal either a potential opportunity if cash flows hold up, or a warning that the market is questioning how durable those cash flows really are. The key issue is which side of that argument you think is closer to the truth.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Charter Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Charter Communications Narrative

If you see the numbers differently or prefer to dig into the details yourself, you can build a custom Charter view in minutes with Do it your way.

A great starting point for your Charter Communications research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for more opportunities?

If Charter has you thinking harder about price and potential, do not stop here. Your next solid idea could be sitting in plain sight.

- Spot potential bargains early by checking out these 879 undervalued stocks based on cash flows that line up current prices with underlying cash flows.

- Tap into the AI trend through these 23 AI penny stocks that focus on companies tied to automation, data analytics, and machine learning.

- Target income focused ideas with these 13 dividend stocks with yields > 3% that may help you build a more dependable stream of payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.