Cheesecake Factory (CAKE) Valuation In Focus After Recent Share Price Momentum And Conflicting Fair Value Views

Cheesecake Factory Incorporated CAKE | 55.23 | -0.13% |

Cheesecake Factory stock in focus

Cheesecake Factory (CAKE) is back on many investors’ watchlists after recent trading, with the share price around $58.60 and a mix of short term and longer term returns drawing fresh comparisons with its fundamentals.

Recent trading has added to a steady run for Cheesecake Factory, with a 30 day share price return of 10.96% and a 3 year total shareholder return of 61.43% suggesting momentum has been building over a longer horizon.

If CAKE’s move has caught your eye and you want to see what else is gaining traction in consumer facing names, broaden your search with fast growing stocks with high insider ownership.

With CAKE trading near $58.60, a value score of 3, revenue of about $3.7b and net income of around $160.8m, the real question is whether the stock is still mispriced or if the market is already baking in future growth.

Most Popular Narrative: 20.6% Undervalued

Compared with Cheesecake Factory’s last close at $58.60, the most followed narrative pegs fair value at $73.83, framing the recent share price against a higher long term view.

The Cheesecake Factory is a stock that I believe most people do not understand it's actual potential; or really what makes this stock so attractive for long term growth. Here is a brief description of the company according to Benzinga: "Cheesecake Factory Inc owns and operates restaurants in the United States and Canada under brands that include The Cheesecake Factory, North Italia, and a collection within the Fox Restaurants Concepts subsidiary. The company's international presence, in the Middle East and Mexico, is through licensing agreements with third parties. The company also has a bakery division that produces cheesecakes and other baked products for sale in its restaurants, international licensees, and third-party bakery customers. The company has four operating business segments: The Cheesecake Factory restaurants, North Italia, other FRC, and Flower Child. Majority of the company's revenue comes from The Cheesecake Factory restaurants segment."

According to Zwfis, that $73.83 fair value rests on a multi brand expansion plan, rising margins and a profit multiple usually reserved for faster growing consumer names. Curious which revenue path and long run profitability assumptions sit underneath that number and how they connect to unit growth targets across every concept.

Result: Fair Value of $73.83 (UNDERVALUED)

However, this growth story could be challenged if new concepts underperform, or if higher capital spending and debt levels pressure margins and cash generation.

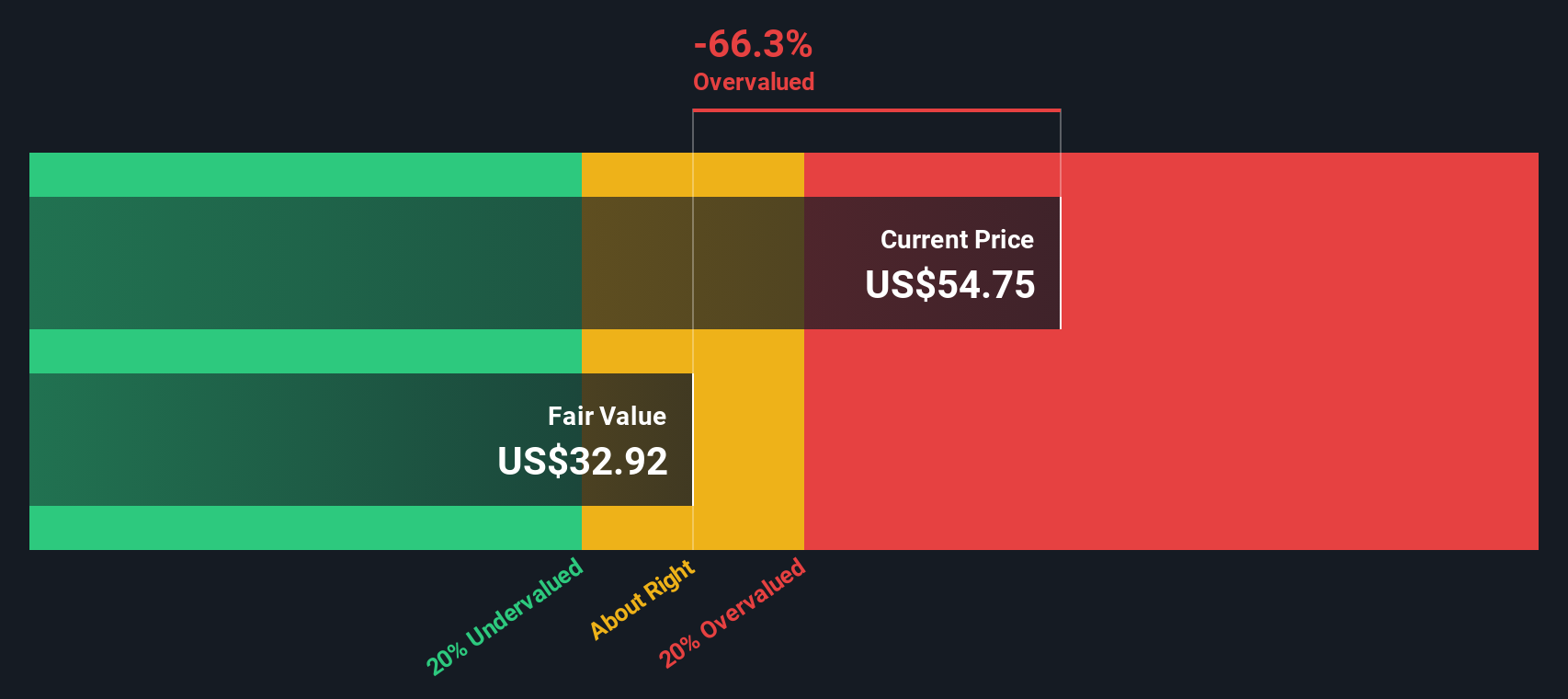

Another Take: SWS DCF Flags a Different Story

While Zwfis’ narrative points to a fair value of $73.83, our DCF model comes out far lower, at $31.10, with CAKE trading around $58.60. That gap suggests the cash flow assumptions behind each view differ sharply. Which set of expectations do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cheesecake Factory for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 875 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Cheesecake Factory Narrative

If you see CAKE’s story differently or simply want to test your own assumptions against the numbers, you can build a personalised view in minutes with Do it your way.

A great starting point for your Cheesecake Factory research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If CAKE has sparked your interest, do not stop there. Broaden your watchlist with a few focused stock ideas that could sharpen your next move.

- Spot potential value and income combinations by checking out these 13 dividend stocks with yields > 3% that might suit a yield focused approach.

- Back future facing themes by scanning these 24 AI penny stocks that tap into artificial intelligence across different parts of the market.

- Hunt for mispriced opportunities with these 875 undervalued stocks based on cash flows that could sit below what their cash flows suggest.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.