Cheniere Energy Partners (CQP) Stock Can Its Valuation Hold Up After The $1.75b Notes Sale

Cheniere Energy Partners, L.P. CQP | 0.00 |

Cheniere Energy Partners (CQP) has drawn fresh investor attention after closing a US$1.75b private placement of senior notes, prompting a closer look at how its funding choices interact with LNG demand and existing contracts.

At a share price of US$58.05, Cheniere Energy Partners has seen short term share price pressure, with the stock down 8.42% over 30 days and 17.24% over 90 days. Its 5 year total shareholder return of 89.63% points to solid longer term momentum.

If you are assessing how this financing fits into the wider energy opportunity set, it can be helpful to widen your lens and review 89 nuclear energy infrastructure stocks

With Cheniere Energy Partners now trading near US$58 and recent returns mixed, investors are weighing solid LNG contracts and new debt against a modest discount to analyst targets. The key question is whether there is real value left or if future growth is already priced in.

Price-to-Earnings of 13.6x: Is it justified?

On earnings, Cheniere Energy Partners is trading on a P/E of 13.6x, with the stock at $58.05 and sitting close to analyst targets that imply only a small upside.

The P/E multiple compares the current share price with annual earnings per share and is a common way to gauge how much investors are paying for each dollar of profit. For a business like Cheniere Energy Partners, which already has meaningful LNG infrastructure in place and ongoing contracts, this type of earnings based yardstick is a useful cross check against more complex models.

Relative to the wider US market average P/E of 18.7x, that 13.6x figure suggests investors are paying less for each dollar of current earnings. It is also below an estimated fair P/E of 19x, a level the market could move towards if sentiment or assumptions about the earnings profile shift. However, against the US Oil and Gas industry average of 12.9x, Cheniere Energy Partners trades on a slightly richer multiple, so investors are accepting a small premium compared to the sector while still at a discount to both peers on average and the fair ratio.

Result: Price-to-Earnings of 13.6x (ABOUT RIGHT)

However, investors in Cheniere Energy Partners still face risks around contract renewals, LNG demand variability, and the added leverage from the US$1.75b senior notes issuance.

Another View: Cheniere Energy Partners Through a DCF Lens

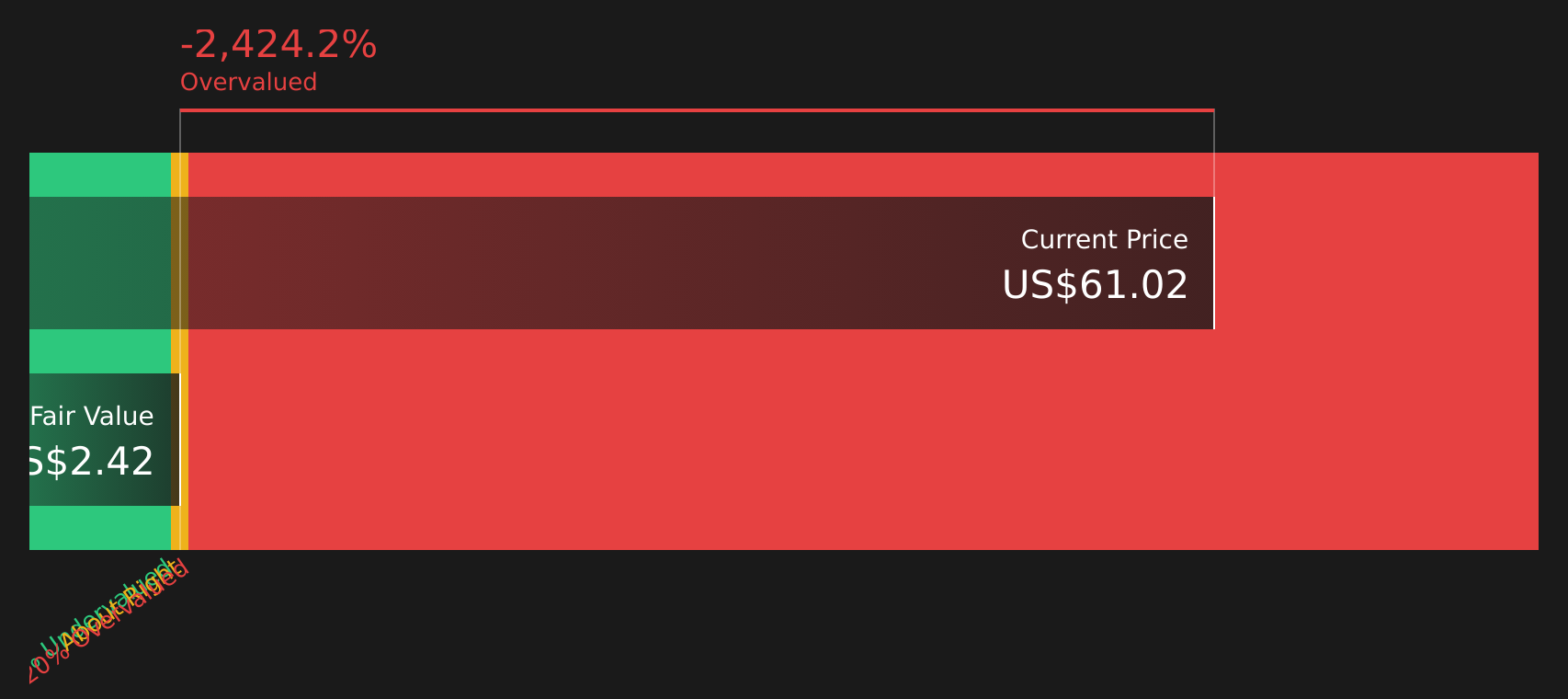

While the P/E of 13.6x suggests Cheniere Energy Partners might be reasonably priced on earnings, the SWS DCF model paints a different picture, with an estimated future cash flow value of just $2.42 per unit versus a $58.05 market price.

That gap implies the current price is well above this cash flow based estimate, raising the question of whether investors are paying up for contracted LNG visibility or simply taking on valuation risk if those assumptions prove too optimistic.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cheniere Energy Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of concerns and optimism around Cheniere Energy Partners feels finely balanced, this is the moment to review the numbers, stress test your own assumptions, and weigh both the potential upsides and the downside flags through the lens of 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Cheniere Energy Partners?

If Cheniere Energy Partners has sharpened your focus, do not stop here. Use the screener to surface fresh stocks that better match your return expectations and risk comfort.

- Target resilient income by reviewing 8 dividend fortresses that prioritize robust payouts and potential stability in tougher markets.

- Hunt for quality at a discount with the screener containing 19 high quality undiscovered gems before they attract wider attention and capital.

- Prioritize sleep at night investing by scanning 66 resilient stocks with low risk scores tailored for investors who refuse to trade discipline for excitement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.