Chubb (CB) Stock May Be A Bargain As Buyback News Lands

Chubb Limited CB | 0.00 |

After a strong 122.3% total return over the past five years, Chubb now sits at a point where its market price and valuation checks send a mixed message. The intrinsic value estimate from the Excess Returns model points to meaningful undervaluation, while earnings based multiples look closer to fair.

- Chubb has returned 122.3% over five years, which puts extra focus on whether today’s price still leaves enough room for attractive long term returns.

- Recent commentary around disciplined capital deployment, including sustained dividend growth and a sizeable repurchase program, can support the valuation case, while catastrophe related insurance risks may cap how much investors are willing to pay for the stock.

- On Simply Wall St’s broader checks, Chubb scores 3 out of 6 on valuation, which points to a mixed picture rather than a clear bargain or clear overvaluation.

For investors, the debate is whether Chubb’s current price around US$346 still offers enough upside versus the intrinsic value estimate to justify the risks that come with its recent share price run.

Does Chubb Look Undervalued on Excess Returns?

The Excess Returns model evaluates how much additional profit Chubb earns on its equity compared with the return that shareholders require, and then estimates how long that difference might persist. For Chubb, the inputs indicate a solid spread between what the business earns and its estimated cost of equity.

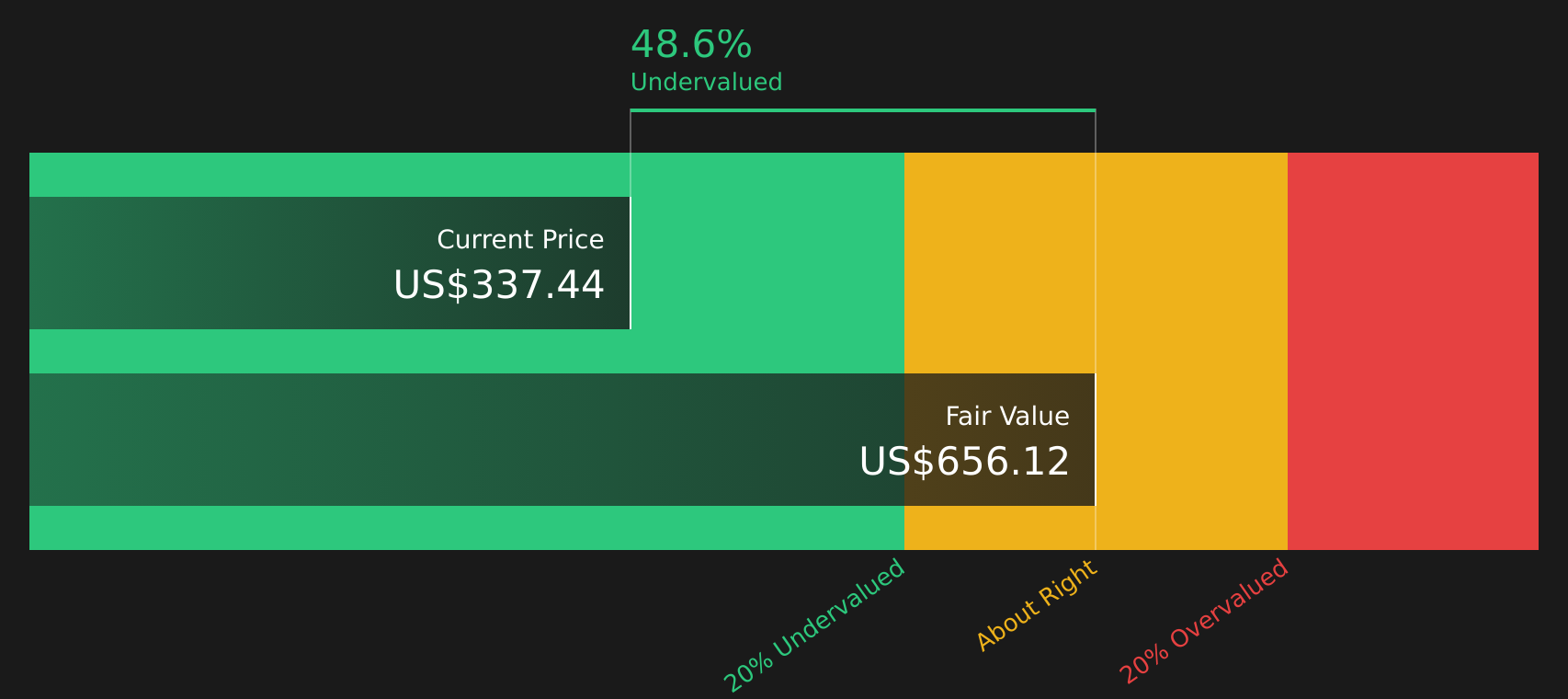

On the latest inputs, Chubb has a Book Value of $189.93 per share and a Stable EPS of $30.22 per share, against a Cost of Equity of $15.65 per share. That leaves an Excess Return of $14.57 per share on an Average Return on Equity of 13.37%, with Stable Book Value projected at $226.07 per share. When these excess profits are capitalized, the model points to an intrinsic value of about $656.56 per share, which compares to the current price near $346 and indicates the stock is 47.3% undervalued. Because recent catastrophe-related concerns have weighed on sentiment, the California wildfire and hurricane-related risks help explain why the market price still trails the intrinsic value output of this model.

On the Excess Returns numbers, Chubb screens as undervalued relative to the cash generation its equity base is expected to support.

Our Excess Returns analysis suggests Chubb is undervalued by 47.3%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Chubb Fairly Priced on Earnings?

P/E is a useful yardstick for Chubb because earnings are a central focus for investors following large, established insurers. On this measure, Chubb trades at about 11.9x earnings, compared with an insurance industry average of roughly 12.4x and a peer group average near 8.9x, so the stock is neither clearly cheap nor clearly expensive against its direct competitors.

Simply Wall St’s fair P/E ratio for Chubb is 11.4x, only slightly below the current 11.9x, which points to a small premium rather than a large mismatch. Given the company’s scale, capital strength and the catastrophe related risks that can influence sentiment, this gap is modest and does not suggest an obvious mispricing on earnings alone.

On the P/E multiple, Chubb looks priced roughly in line with what the underlying business profile and sector context would suggest.

The Chubb Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Chubb sit on the Community page and act as a bridge between the valuation gap above and the specific expectations that would need to hold on growth, margins and earnings for the stock to be worth meaningfully more or less than today’s price. Each narrative links Chubb’s potential catalysts and risks to a particular fair value estimate, so you can track over time which version of events appears to be unfolding.

If you have a numbers based view on whether Chubb's capital deployment and catastrophe related risks support today’s share price, share a Narrative in the Simply Wall St community and set out the drivers you think matter most.

It is a chance to put your thesis on record, then watch how it stacks up as Chubb’s results and market reaction unfold.

Do you think there's more to the story for Chubb? Head over to our Community to see what others are saying!

The Bottom Line

For Chubb, the intrinsic value estimate from the Excess Returns model suggests a sizeable discount to current trading levels, while the P/E view points to a stock that is priced about right against peers. That split reflects different lenses, with the intrinsic value work anchored on the returns Chubb earns on its equity, and the multiple view more tied to sentiment and how insurers are currently being valued. With broader valuation checks sitting in the mixed zone, the key consideration for investors is whether catastrophe related risks justify the current discount or whether the market is underestimating the durability of Chubb’s returns on capital.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.