Cisco Systems (CSCO) Stock After 50% YTD Surge Is There More Upside Left

Cisco Systems, Inc. CSCO | 0.00 |

- If you are wondering whether Cisco Systems stock still offers value after a strong run, this article walks through what the current share price might be implying.

- Cisco Systems recently closed at US$113.77, with the share price down 4.8% over the past week and 5.5% over the past month, yet still up 49.6% year to date and 69.5% over the last year.

- These moves have put Cisco Systems firmly on many investors' watchlists, as they reassess what is already priced into the stock. The strong 3 year return of 138.9% and 5 year return of 143.5% add useful context when thinking about whether expectations have become too optimistic or still look reasonable.

- Simply Wall St’s valuation model currently gives Cisco Systems a value score of 2 out of 6. The next sections will compare different valuation approaches and then finish with a broader way to think about what this score really means for long term investors.

Cisco Systems scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

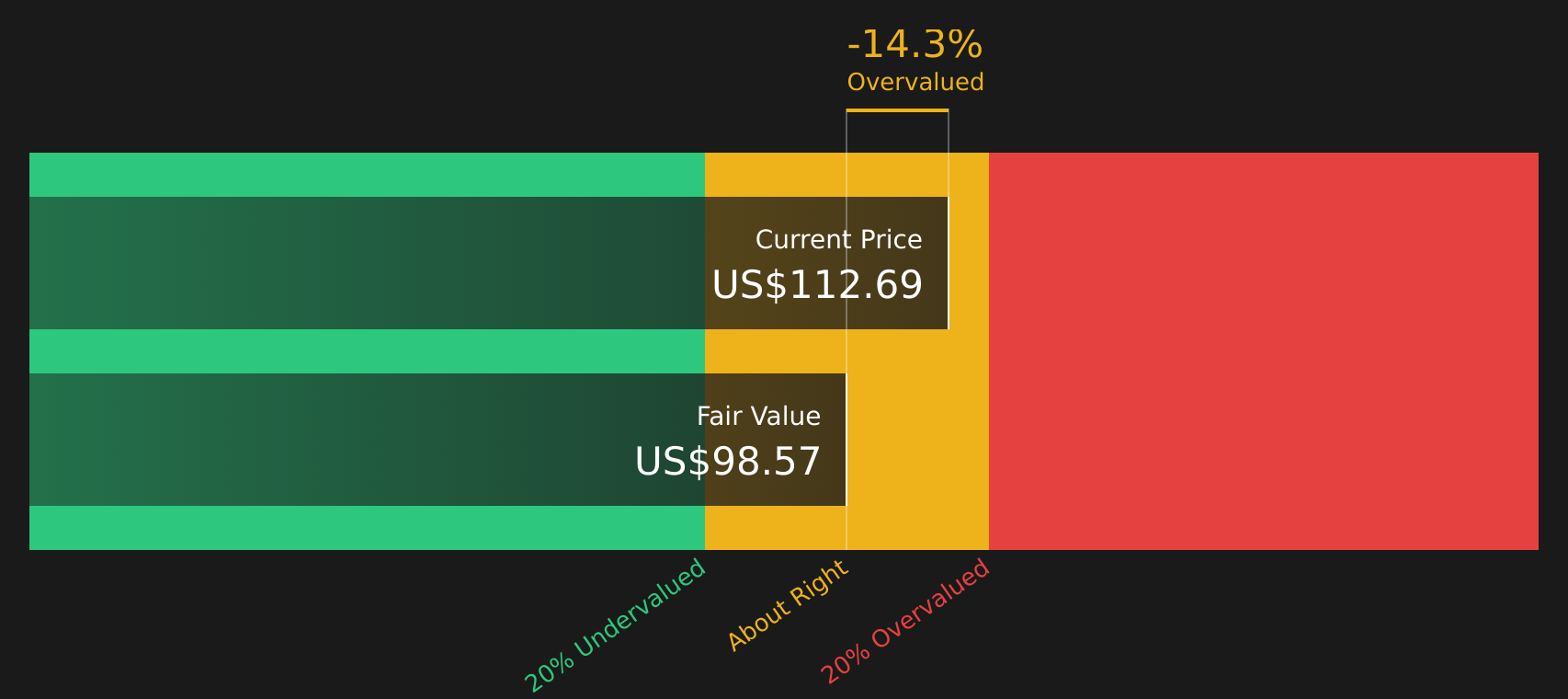

Approach 1: Cisco Systems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Cisco Systems might be worth today by projecting its future cash flows and discounting them back to a present value using a required rate of return.

For Cisco Systems, the model uses last twelve month Free Cash Flow of about $12.0b and projects how that cash flow could evolve over time. Analyst inputs extend to specific annual forecasts, such as projected Free Cash Flow of $21.8b in 2030, with additional years extrapolated by Simply Wall St to build a full 2 Stage Free Cash Flow to Equity model.

Based on these projections, the DCF model arrives at an estimated intrinsic value of $93.28 per share. Compared with the recent share price of $113.77, the DCF implies that Cisco Systems stock trades at roughly a 22.0% premium to this estimate. On this specific cash flow framework, the shares appear overvalued relative to the model's intrinsic value estimate.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cisco Systems may be overvalued by 22.0%. Discover 44 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Cisco Systems Price vs Earnings

For a profitable company like Cisco Systems, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. Higher growth expectations or lower perceived risk usually support a higher “normal” P/E, while slower growth or higher risk often line up with a lower multiple.

Cisco Systems currently trades on a P/E of 37.50x. This sits above the Communications industry average P/E of 31.28x and below the peer group average of 96.25x. Simply Wall St also calculates a proprietary “Fair Ratio” for Cisco Systems of 41.52x, which is the P/E the stock might be expected to trade on given factors such as its earnings profile, industry, profit margins, market cap and risk characteristics.

The Fair Ratio aims to be more tailored than a simple comparison with peers or industry averages because it incorporates company specific features like growth, profitability and risk, as well as where Cisco Systems sits within its sector by size. With the current P/E of 37.50x below the Fair Ratio of 41.52x, this framework indicates that Cisco Systems stock may be undervalued on a P/E basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Cisco Systems Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in as a simple way to connect Cisco Systems story with a set of numbers like revenue, earnings, margins and a Fair Value estimate that you can compare to the current share price.

On Simply Wall St, a Narrative is your own Cisco Systems storyline written in financial form, where you pick assumptions for things like future revenue growth, profit margins and the P/E you think is reasonable, and the platform converts that story into forecasts and a Fair Value that you can track against the live price to help decide whether the stock looks expensive or cheap to you.

Narratives sit inside the Community page used by millions of investors, are easy to set up and are updated automatically when new information such as earnings, news or guidance is added. This means you can keep your Cisco Systems view current without rebuilding your model each time.

For example, one investor might build a Cisco Systems Narrative similar to the bullish community view, with a Fair Value around US$150.00. Another might lean closer to the cautious view with a Fair Value near US$94.55, and seeing both side by side makes it clearer which story, and which Fair Value, feels closer to your own expectations before you decide whether the current price fits your plan.

For Cisco Systems however we'll make it really easy for you with previews of two leading Cisco Systems Narratives:

Here is an example of a bullish Narrative that currently treats Cisco Systems as slightly undervalued on its own assumptions.

Fair value: US$127.05 per share

Implied undervaluation vs last close of US$113.77: about 10.5% below this Narrative fair value

Revenue growth assumption: 7.47% per year

- Focuses on AI infrastructure orders, integrated security and data center networking as key supports for Cisco Systems revenue and margin strength.

- Emphasizes the shift toward subscriptions and software, using figures such as 54% of revenue from subscriptions and recurring product ARR up 8% as inputs for more stable earnings.

- Builds a fair value of US$127.05 per share around analyst assumptions for revenue of US$75.4b, earnings of US$19.5b, a future P/E of 32.8x and an 8.78% discount rate, while also flagging competition, execution and acquisition integration risks.

On the other side, here is a Narrative that is more cautious on Cisco Systems and treats the stock as overvalued on its chosen assumptions.

Fair value: US$110.56 per share

Implied overvaluation vs last close of US$113.77: about 2.9% above this Narrative fair value

Revenue growth assumption: 7.20% per year

- Describes Cisco Systems as a defensive AI infrastructure and enterprise technology stock with solid cash generation, but with growth that depends on successful execution in AI networking, security and software.

- Highlights risks around concentration in hyperscaler customers, competition from other AI and networking providers, margin pressure from hardware mix and potential culture or innovation setbacks from restructuring and cost cuts.

- Frames valuation as requiring only moderate growth and income to justify current pricing, with a fair value of US$110.56 and a future P/E of 38.11x, leading to a more balanced or selective stance on Cisco Systems stock.

If you want to stress test your own expectations for Cisco Systems against these types of bullish and cautious stories, the Community page lets you review or build Narratives side by side, update the numbers and see how your fair value view compares to the current price.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Cisco Systems on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Cisco Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.