Citigroup (C) Could Be 26% Undervalued Following Dividend Rise And $30b Buyback Plan

Citigroup Inc. C | 0.00 |

Dividend and buyback plans shift focus to Citigroup stock

Citigroup (C) has moved into focus after the Federal Reserve’s 2026 stress test, with the bank outlining a 12% dividend increase and a multi year US$30b share repurchase program.

Citigroup’s share price has pulled back 2.22% in the last session to US$141.76, but the 30 day share price return of 13.06% and 90 day gain of 32.02% suggest positive momentum. The 1 year total shareholder return of 71.81% points to strong longer term performance.

Recent capital return plans sit alongside a busy period of funding and product activity, with multiple fixed income offerings completed and new structured products issued, as well as senior appointments in wealth and corporate banking that signal continued focus on key business lines.

If you are looking beyond Citigroup for ideas in financial services and related themes, this could be a good moment to broaden your search with 20 top founder-led companies

With Citigroup trading at US$141.76, around 5% below the average analyst price target and with an estimated intrinsic discount of roughly 26%, the key question is whether this signals a genuine mispricing or if the market is already factoring in the next leg of growth.

Preferred P/E ratio of 16.5x for Citigroup, is it justified?

Citigroup is trading on a P/E of 16.5x, which sits above both its peer group on 13.3x and the broader US Banks industry on 12.3x, pointing to a richer valuation compared to many competitors at the current $141.76 share price.

The P/E ratio compares what investors are currently paying for each dollar of Citigroup’s earnings. A higher P/E often reflects expectations for steadier profits, a more resilient business mix or a perception of higher quality earnings.

Here, the P/E of 16.5x is not only above peers and the sector, it also exceeds an estimated fair P/E of 15.6x. That gap indicates the market is assigning Citigroup a premium that could compress if sentiment or earnings expectations change. It could also be sustained if investors continue to see its profile as stronger than the typical US bank.

Result: Price-to-earnings of 16.5x (OVERVALUED)

However, Citigroup’s richer P/E and premium to estimated fair value could face pressure if earnings momentum slows or if sentiment toward the broader banks sector weakens.

Another view on Citigroup’s value

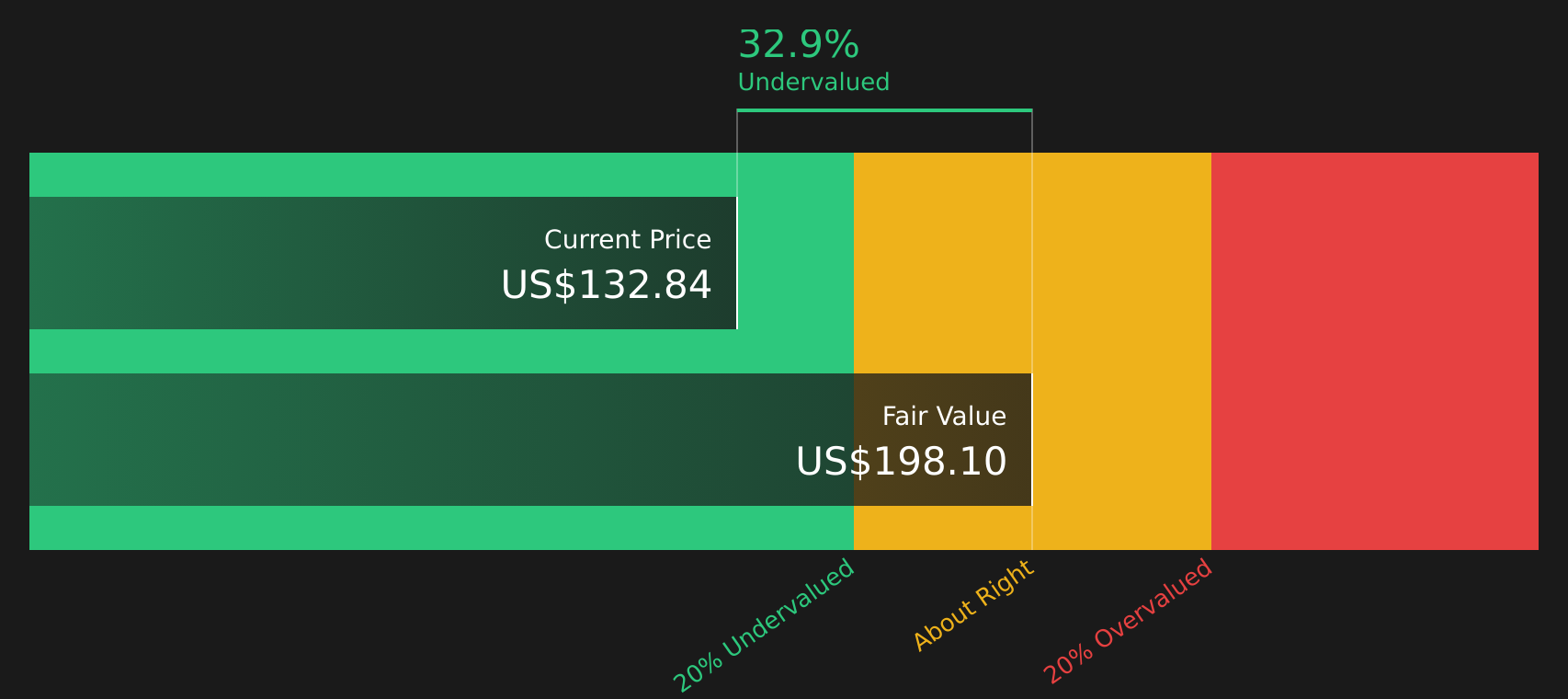

While the P/E of 16.5x makes Citigroup look expensive against peers and the US Banks industry, the SWS DCF model points the other way, with an estimated fair value of US$190.53 per share versus the current US$141.76, suggesting the stock trades at a discount.

That kind of gap between earnings based metrics and a cash flow based estimate raises a practical question for you as an investor: is the market overpaying for near term earnings quality or underpricing the longer term cash flow potential?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Citigroup for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mixed signals around Citigroup’s valuation and outlook mean sentiment is anything but one sided right now. It therefore makes sense to review the underlying data and move quickly to frame your own view using 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Citigroup?

If you want to round out your view of Citigroup with fresh stock ideas, this is the moment to widen your search using the Simply Wall Street Screener.

- Target stability by scanning for companies that combine resilient fundamentals with low risk profiles using the 70 resilient stocks with low risk scores.

- Hunt for potential value opportunities by zeroing in on companies that appear mispriced relative to their quality through the 44 high quality undervalued stocks.

- Spot potential standouts early by using the screener containing 19 high quality undiscovered gems to surface quality stocks that many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.