Citigroup (C) Stock Looks Below Fair Value Despite A 230% Run

Citigroup Inc. C | 0.00 |

Citigroup stock has surged over the past three years, yet the current checks send a mixed message on value, with the Excess Returns intrinsic value estimate pointing to upside while the earnings multiples look broadly in line with the market.

- Citigroup has returned about 230.3% over three years, which puts extra weight on whether investors are now paying a full price for the turnaround.

- The push into areas like tokenized private assets and higher planned capital returns via dividends and buybacks can support the intrinsic value case. At the same time, regulatory scrutiny and legal probes may limit how much of that value investors are willing to pay for.

- The stock screens as neither clearly cheap nor clearly expensive overall, with 3 out of 6 valuation checks suggesting it is undervalued.

The issue now is whether Citigroup's current share price already reflects this turnaround and capital return story, or if the intrinsic value estimate still points to a margin of safety.

Is Citigroup Still Cheap on Excess Returns?

The Excess Returns model estimates what Citigroup can earn on its equity above its cost of capital and then prices those recurring “excess” profits per share. For Citigroup, the inputs point to a business that is expected to earn more on its book value than investors require.

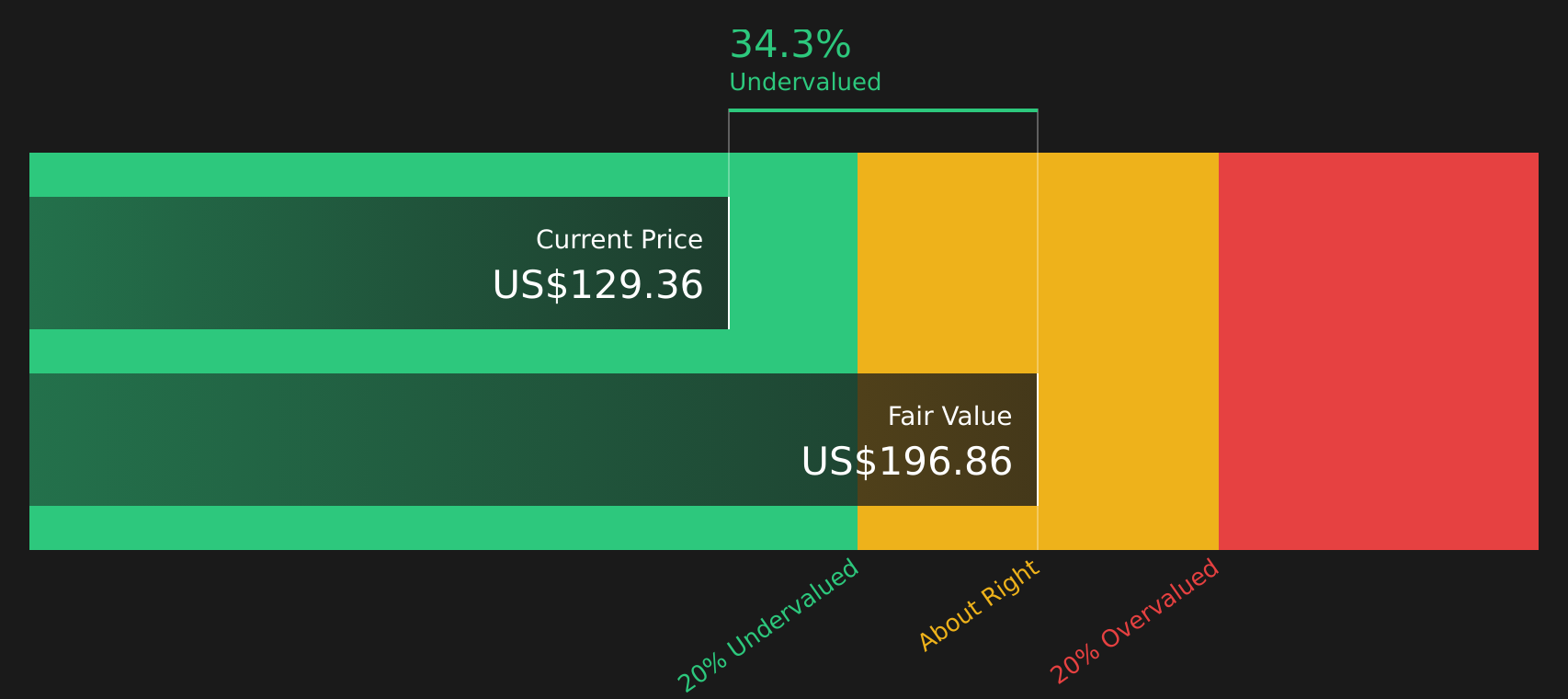

Citigroup is modeled with a Book Value of $112.23 per share and a Stable EPS of $13.09 per share, based on forward Return on Equity estimates from 14 analysts. Against a Cost of Equity of $10.22 per share, this implies Excess Return of $2.87 per share, supported by an average Return on Equity of 10.26% and a Stable Book Value assumption of $127.62 per share. Together, these inputs translate into an Excess Returns intrinsic value estimate of $191.79 per share, suggesting the stock screens as 26.9% undervalued versus the current price.

Because the Fed stress test cleared the way for higher dividends and a multi year $30b buyback plan, the market is now weighing those capital returns in relation to the Excess Returns model, which still indicates a valuation gap.

On this model, Citigroup currently appears undervalued, with the price not yet matching the excess earnings power implied by its equity base.

Our Excess Returns analysis suggests Citigroup is undervalued by 26.9%. Track this in your watchlist or portfolio, or discover 41 more high quality undervalued stocks.

Does Citigroup Look Fairly Valued on Earnings?

P/E is a useful cross check for Citigroup because earnings are still a core yardstick for large banks and tend to capture both credit costs and fee income in a single measure. Right now, Citigroup trades on a P/E of 16.3x, above both the broader banks industry average of 12.3x and the peer group average of 13.5x, so the stock carries a clear premium to many large lenders.

The Fair Ratio for Citigroup is 16.6x, only slightly above the current multiple, which suggests the premium is broadly in line with what you might expect given its size, business mix and risk profile. While recent stress test results, higher planned capital returns and interest in areas such as tokenized assets have supported sentiment, the current P/E already reflects much of that narrative when compared with sector norms.

Overall, Citigroup’s P/E appears broadly consistent with its model based fair ratio, so the stock comes across as roughly fairly valued on this earnings multiple.

The Citigroup Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Citigroup pick up where the valuation checks leave off by spelling out the future paths for Citigroup's revenue, margins and earnings that would need to hold for the stock to be worth materially more or less than today's price, and they sit on the company's Community page. Where a single ratio or model gives one figure, these narratives unpack the underlying assumptions so you can watch how Citigroup's actual progress lines up with them over time.

Community narratives on Citigroup sit far apart, with one side arguing the stock still has a wide valuation gap while the other sees expectations running ahead of earnings quality.

Bull case: 40% undervalued

"This means businesses can move cash instantaneously, 24/7, across their global hubs, from New York to Hong Kong or the U.K., with Citi absorbing all the intricate 'complexities of compliance, reporting, accounting, AML'..."

Bear case: 11% overvalued

"Heavy macroeconomic influence and high expenses from transformation investments could pressure Citigroup's revenues, margins, and net earnings amid regulatory and credit risk challenges..."

Do you think there's more to the story for Citigroup? Head over to our Community to see what others are saying!

The Bottom Line

Citigroup’s intrinsic value estimate on the Excess Returns model points to a meaningful discount, while the P/E suggests the stock is priced roughly in line with large bank peers. That mixed read, echoed by the broader valuation checks, leaves the real question of whether the market is underestimating the durability of Citigroup’s excess earnings power or correctly pricing regulatory and execution risks. For you, the crux is whether the current discount to intrinsic value is compensation for those risks or a gap that could close if the turnaround and capital return plans stay on track.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.