ClearPoint Neuro (CLPT): Evaluating Valuation After Dr. Paul Larson Announced as Incoming Chief Medical Officer

ClearPoint Neuro CLPT | 0.00 |

ClearPoint Neuro is bringing Dr. Paul Larson on board as its new Chief Medical Officer starting January 2026. Larson’s extensive background in cell and gene therapy delivery, along with his ties to major research hospitals, adds fresh perspective to the company’s clinical strategy.

News of Dr. Larson stepping into the Chief Medical Officer role has certainly caught investor attention, reinforcing confidence in ClearPoint Neuro's leadership as the company advances in cell and gene therapy. The boost in sentiment is reflected in a steady share price this year, and with a 1-year total shareholder return of just over 1%, momentum remains modest but positive compared to recent periods. The sense is that the groundwork being laid now could spark stronger performance as new clinical partnerships bear fruit.

If ClearPoint’s progress has you watching innovation in medtech, now is the perfect time to explore fresh opportunities with the See the full list for free.

This recent leadership move and steady performance raise a key question for investors: is ClearPoint Neuro trading at an attractive discount given its future prospects, or has the market already priced in all the expected growth?

Most Popular Narrative: 13.6% Undervalued

ClearPoint Neuro's most popular narrative assigns a fair value notably above the current share price, capturing market attention as investors weigh long-term growth prospects.

Multiple biopharma partners are progressing through regulatory milestones, including nine active programs accepted for expedited FDA review and key drugs approaching commercialization (for example, for Huntington's disease). This sets the stage for non-linear revenue inflection from a broader commercial rollout over the next 1-3 years.

What is fueling this valuation? The narrative alludes to ambitious revenue ramp-ups and profit transformation that could redefine ClearPoint’s earnings profile. Want to see the ground-shaking financial assumptions and industry comparisons behind this price target? Take a closer look and uncover what could drive the next big move.

Result: Fair Value of $29 (UNDERVALUED)

However, persistent reliance on a few gene therapy partners and rising R&D expenses could challenge ClearPoint Neuro's path to sustainable and profitable growth.

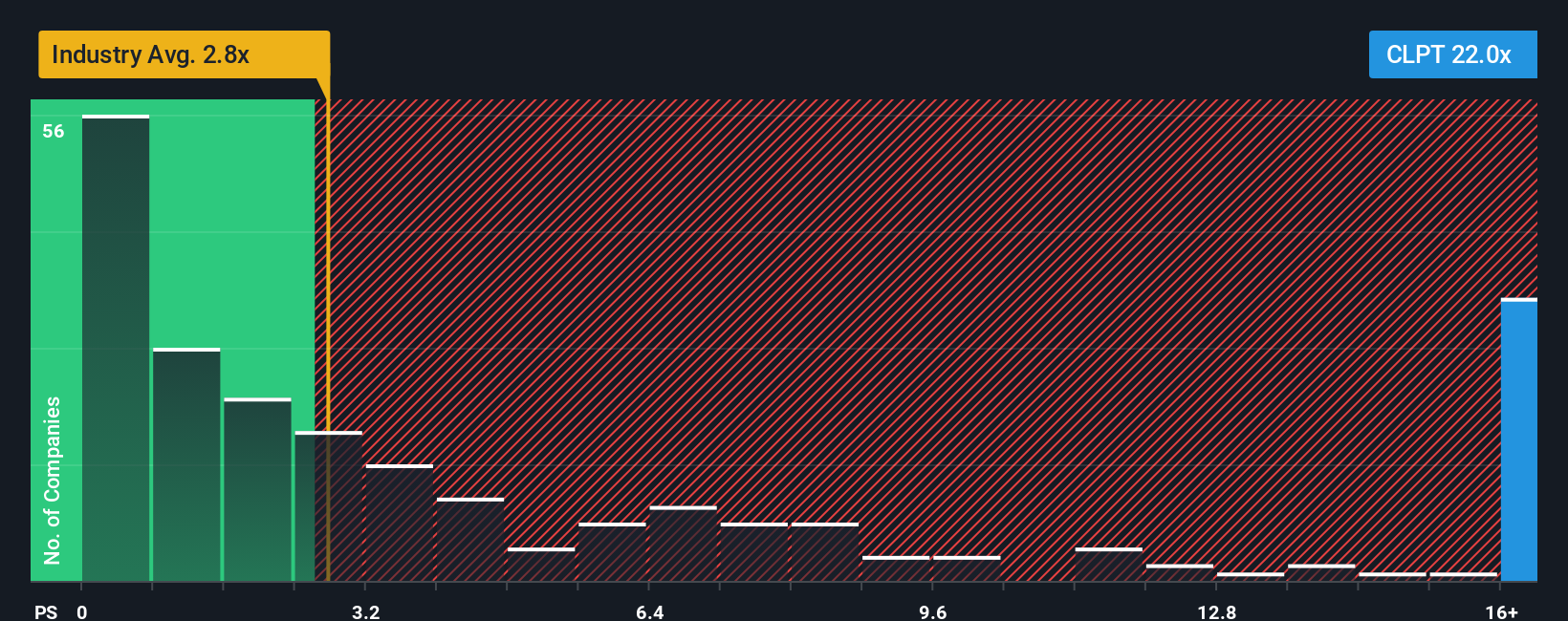

Another View: High Price Compared to Sales Benchmarks

Looking at ClearPoint Neuro’s value through its price-to-sales ratio, the numbers tell a more cautious story. The company trades at 21.2 times revenue, which is far above the US Medical Equipment industry average of 2.8, its peer average of 2.5, and even its potential fair ratio of 3.6. This high premium signals that investors are pricing in aggressive future growth, which can bring both opportunity and significant valuation risk if things do not play out as expected. Will ClearPoint’s momentum justify this, or is a correction likely?

Build Your Own ClearPoint Neuro Narrative

If you have your own perspective on ClearPoint Neuro’s outlook or want to investigate the story behind the numbers yourself, you can shape your own analysis in just a few minutes. Do it your way

A great starting point for your ClearPoint Neuro research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let your investment strategy miss out on the next big trend. Unique opportunities are waiting for action-takers using the right tools. Find your next standout stock by checking these out:

- Build steady income streams by targeting these 19 dividend stocks with yields > 3% that currently offer yields above 3%.

- Capitalize on fast-moving tech advancements by following these 24 AI penny stocks set to transform industries with artificial intelligence breakthroughs.

- Take advantage of significant upside by scanning these 900 undervalued stocks based on cash flows trading well below their intrinsic value, based on robust cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.