Clearway Energy (CWEN) Stock Still Looks Cheap On Clean Energy Finance Trends

Clearway Energy, Inc. Class C Common Stock CWEN | 0.00 |

Clearway Energy stock has delivered a 67.8% return over the past 5 years, yet its broader valuation checks still point to the shares looking inexpensive rather than fully priced in.

- Over 5 years, a 67.8% total return suggests Clearway Energy has already rewarded patient shareholders while still leaving room to question whether the current price fully reflects its track record.

- Growing investor focus on recurring cash flows from clean energy projects can support how the stock is priced, while higher funding costs and policy uncertainty around renewables remain important risks for what investors are willing to pay.

- On Simply Wall St's checks, Clearway Energy screens as undervalued in 6 of 6 valuation tests, which leans toward the stock looking inexpensive across multiple angles.

The issue now is whether that high valuation score and past 5 year return justify viewing Clearway Energy as a bargain at around US$34.18 per share today.

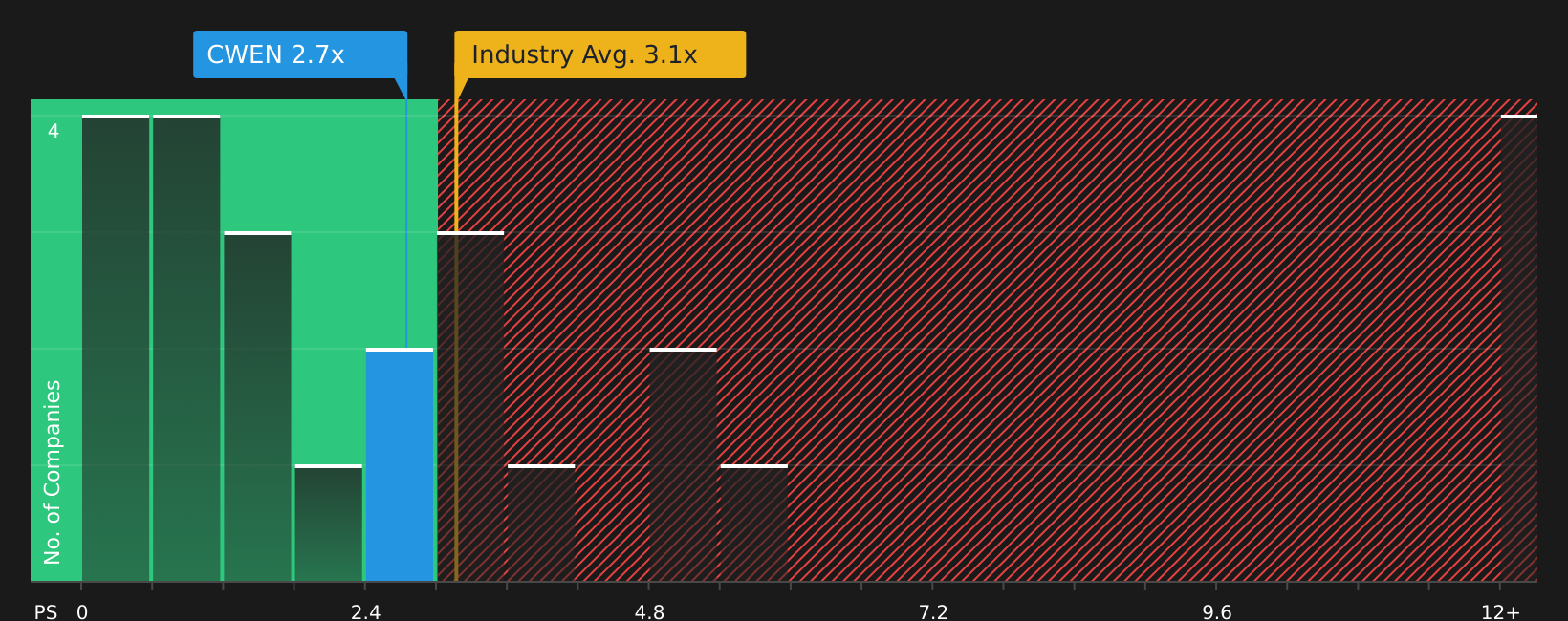

Does Clearway Energy Look Undervalued on Sales?

The P/S multiple suits Clearway Energy because revenue is a key anchor for valuing contracted power generation. Clearway Energy currently trades on a P/S of 2.8x, almost identical to the peer average of about 2.8x and a little above the broader renewable energy industry average of 2.5x. That puts the stock roughly in line with how similar companies are priced on sales today rather than standing out as either heavily discounted or richly priced against the group.

On Simply Wall St's more tailored fair P/S estimate of 4.5x, which incorporates factors like profitability, business mix and risk, Clearway Energy appears undervalued relative to what that framework suggests investors might be willing to pay for each dollar of revenue. Even with sector peers also focusing on recurring income from clean energy infrastructure, Clearway Energy's current multiple sits below that fair ratio, indicating a gap between its present pricing and the level implied by those fundamentals.

On the P/S multiple, Clearway Energy stock appears undervalued relative to the fair ratio suggested by its fundamentals.

The Clearway Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Clearway Energy's valuation puzzle leaves off by spelling out which future paths for revenue, margins and earnings would need to play out for the stock to look materially cheaper or more expensive than it does today. Each one treats fair value as a thesis about Clearway Energy's business that you can revisit over time, rather than a single static number. Narratives for Clearway Energy sit on Simply Wall St's Community page.

Community views on Clearway Energy sit far apart, with one camp leaning into the long-term pipeline and another fixating on funding and execution risk.

Bull case: 22% undervalued

"Clearway expects to deploy at least US$2.5b of corporate capital by 2030 at CAFD yields around 10% to 11%, funded by a mix of retained cash flow, corporate debt and ongoing equity issuance…"

Bear case: roughly fairly valued

"The plan to deploy about US$3b of corporate capital from 2026 to 2029 relies heavily on continued access to construction debt, project debt, tax equity and tax credit transfer markets…"

Do you think there's more to the story for Clearway Energy? Head over to our Community to see what others are saying!

The Bottom Line

For Clearway Energy, the current set of valuation checks leans toward the stock looking undervalued on market multiples, with the P/S ratio sitting below the tailored fair ratio implied by its fundamentals. That gap only matters if the company can keep translating its contracted portfolio into steady cash flows while managing funding costs and policy risk. The crux for you as an investor is whether the discount reflects excess caution around execution and financing, or whether it marks a genuine opportunity if Clearway Energy continues to deliver on its project and capital deployment plans.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.