Clearway Energy (CWEN) Stock Still Looks Reasonable Despite Its 57% Run

Clearway Energy, Inc. Class C Common Stock CWEN | 0.00 |

Clearway Energy has delivered a 56.6% total return over the past 5 years, yet its current checks still lean on the cheap side, which raises the question of whether the recent share price around US$33.77 is fully reflecting the underlying cash generation and risks.

- A 56.6% return over 5 years suggests Clearway Energy has already rewarded patient investors, so any further upside may depend on how much value is still not priced in.

- The build out of renewable and storage assets tied to long term contracts and AI driven electricity demand can support cash flow expectations. At the same time, the capital required for ongoing projects and acquisitions may limit how much the valuation can re rate.

- On Simply Wall St's checks, Clearway Energy screens cheap on most metrics, with 5 out of 6 valuation checks suggesting the stock leans undervalued.

The stock's next move may depend on whether the market starts to price Clearway Energy more in line with these supportive valuation checks or keeps treating it cautiously despite its track record and pipeline.

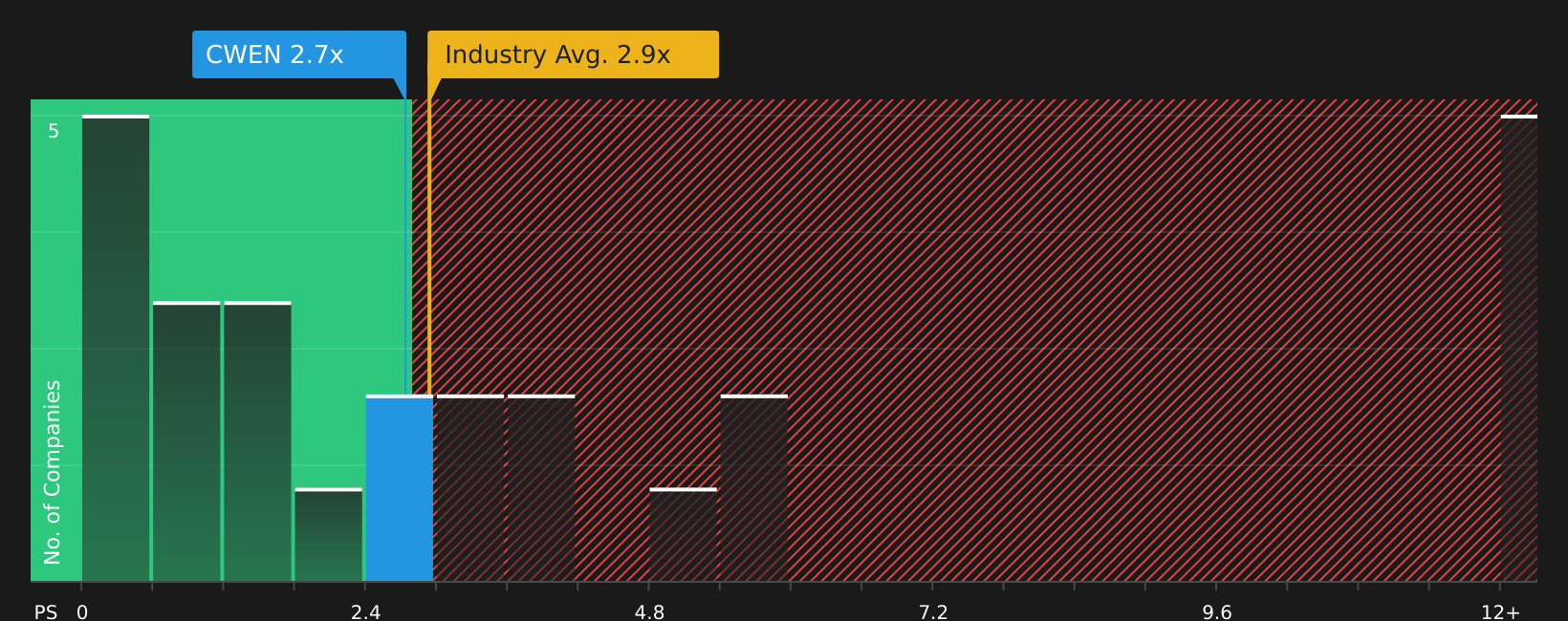

Is Clearway Energy Still Cheap on Sales?

The P/S ratio is a useful way to look at Clearway Energy because its revenues are tied to contracted renewable and storage projects, which can make sales a cleaner anchor than earnings in some periods.

Clearway Energy trades on a P/S of about 2.8x, which is slightly above the renewable energy industry average of roughly 2.6x and very close to the peer group at around 2.7x. Despite that, the modelled fair P/S ratio for Clearway Energy is 4.5x, suggesting the current multiple sits well below what might be expected given its size, business mix and risk profile.

Because the company has been expanding its renewable and battery portfolio, as seen with projects like the Honeycomb storage assets, the stock still prices at a discount to this fair ratio even with those developments in place. Taken together with the other valuation checks, the P/S multiple indicates that the market may not be fully reflecting the sales base Clearway Energy has already built.

On the P/S measure, Clearway Energy stock appears undervalued relative to the level implied by the fair multiple.

The Clearway Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Clearway Energy valuation puzzle leaves off by spelling out which paths for revenue growth, margins and earnings would need to play out for the stock to look meaningfully higher or lower than today's price. Each narrative ties its number to a clear view on how Clearway Energy's growth, profitability and risks might evolve, giving you a reference point you can revisit as new information comes through on the Community page.

One of the top community narratives on Clearway Energy: 23% undervalued

"Clear funding visibility through 2030, including retained cash flow, recent senior unsecured notes with tight spreads to treasuries and accretive equity issuance, positions the company to deploy corporate capital at CAFD yields of around 10.5% on identified projects…"

Do you think there's more to the story for Clearway Energy? Head over to our Community to see what others are saying!

The Bottom Line

Clearway Energy still screens as undervalued on market multiples, with its current P/S ratio sitting below the fair level implied by the checks you have seen. That gap will likely close only if investors gain more confidence that its existing contracted projects and development pipeline can support the cash generation implied by those fair multiples. The key question is whether the current discount reflects an opportunity or a market view that ongoing capital needs and project execution risk deserve a lower valuation for longer.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.