Cloudflare (NET) Valuation In Focus As Earnings Near And Zero Trust Demand Meets Deal Uncertainty

Cloudflare NET | 178.65 | -2.92% |

Why Cloudflare’s upcoming earnings are in focus

Cloudflare (NET) is set to report fourth quarter 2025 results on February 10, 2026, drawing attention to how enterprise demand for zero trust cybersecurity compares with recent challenges in closing larger deals.

Cloudflare’s share price has been choppy, with a 1-day share price return of 6.23% contrasting with a 90-day share price return showing a decline of 27.99%. Its 3-year total shareholder return of 188.20% highlights that long term holders have still seen very strong gains.

If you are watching Cloudflare ahead of earnings and want more ideas in similar areas, take a look at our screener of 56 profitable AI stocks that aren't just burning cash as potential next candidates to research.

With Cloudflare shares down 28% over 90 days but still up strongly over three years, and the stock trading about 33% below the average analyst target, you have to ask: Is there a genuine entry point here, or is the market already baking in the next leg of growth?

Most Popular Narrative: 26% Undervalued

Cloudflare’s most followed narrative pegs fair value at about $232.78, above the last close of $173.21. This puts a spotlight on the growth assumptions behind that gap.

The accelerating adoption of AI, explosion in global web traffic, and proliferation of IoT devices are driving increased demand for fast, secure, and resilient cloud-native infrastructure, Cloudflare's core strength, evidenced by strategic partnerships with major AI companies and record-breaking DDoS mitigation, positioning the company for sustained top-line revenue growth and strengthening customer retention.

Curious what earnings path and margin profile underpin that higher fair value, especially given today’s losses and rich expectations on future profits? The full narrative spells out the revenue ramp, profitability shift, and valuation multiple that have to line up for Cloudflare’s story to match that price.

Result: Fair Value of $232.78 (UNDERVALUED)

However, you also have to weigh margin pressure from heavy investment against rising competition, which could challenge the high growth and rich P/E assumptions behind this story.

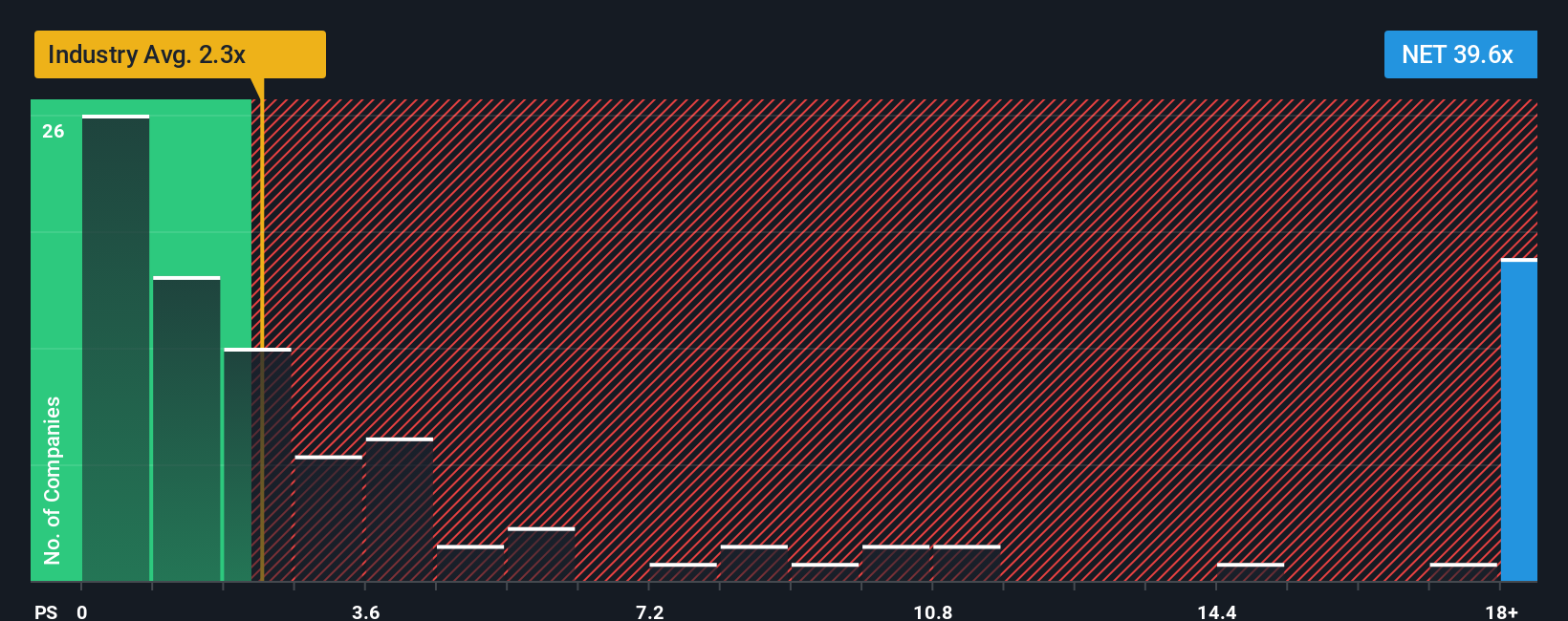

Another View: Valuation Looks Full On Sales

While the narrative model points to a fair value of $232.78 and labels Cloudflare as undervalued, the current P/S ratio of 30.1x tells a different story. That is much higher than the US IT industry at 2x, the peer average at 12.8x, and the fair ratio of 13.4x that the market could move toward over time.

If the P/S ratio were to drift closer to peers or that fair ratio, it would imply a very different price than the narrative suggests. This raises the question of which signal to use as the primary reference point when thinking about risk and potential upside.

Build Your Own Cloudflare Narrative

If you think the current story misses something or prefer to lean on your own work, you can build a custom view in minutes, starting with Do it your way.

A great starting point for your Cloudflare research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Cloudflare is on your radar, do not stop there; casting a wider net now could help you spot opportunities others overlook and refine your watchlist.

- Target value focused opportunities by scanning companies our screener highlights as 52 high quality undervalued stocks that combine quality fundamentals with appealing prices.

- Prioritise resilience by reviewing businesses flagged in our 82 resilient stocks with low risk scores that score well on stability and lower observed risk factors.

- Hunt for potential future standouts using our screener containing 24 high quality undiscovered gems that surface lesser known names with solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.