Clover Health (CLOV) Is Up 20.7% After Court-Ordered Medicare Star Rating Upgrade - What's Changed

Clover Health CLOV | 0.00 |

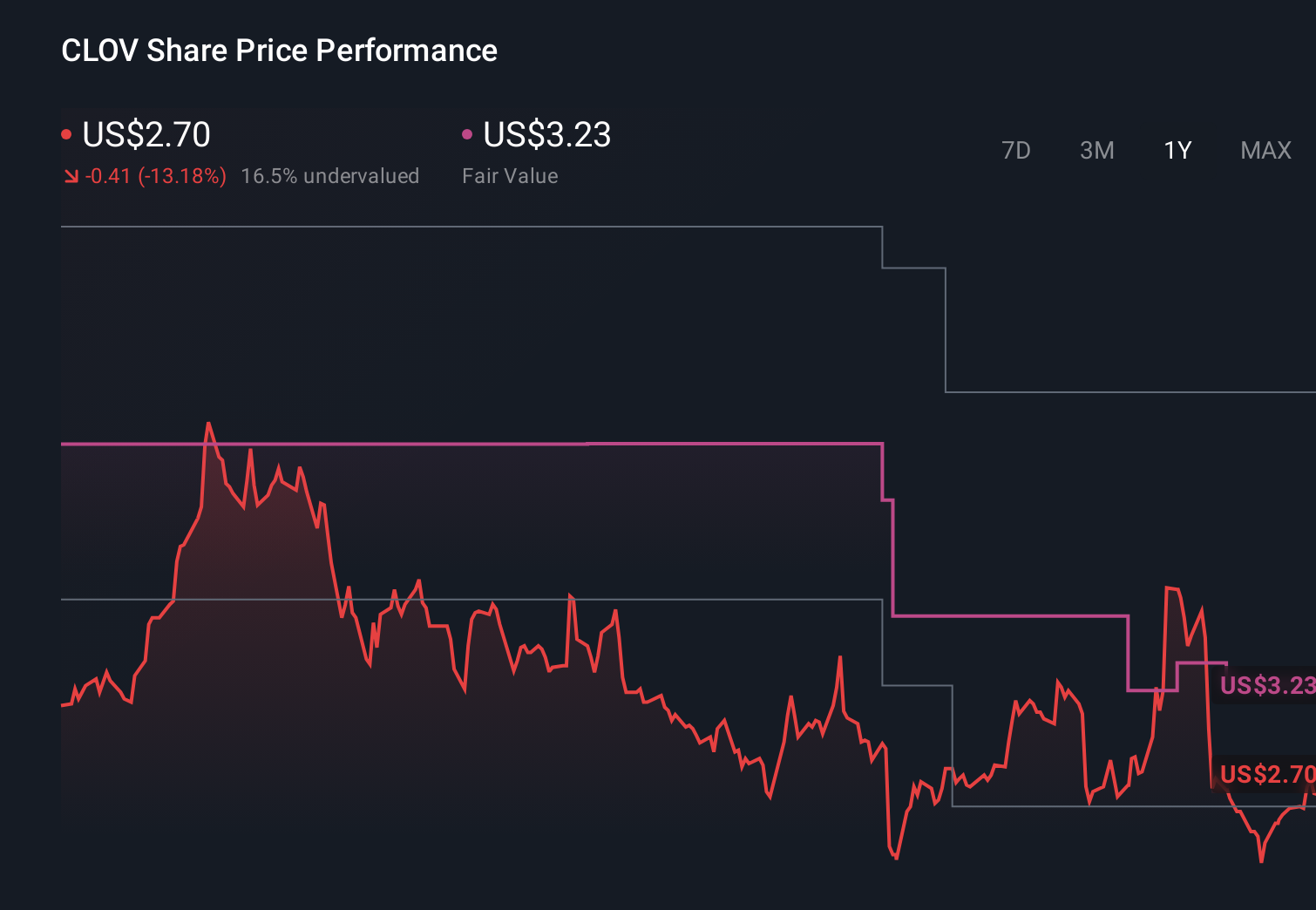

- Clover Health Investments recently won a U.S. District Court case that led CMS to recalculate and upgrade its 2026 Medicare Star Rating for the company’s PPO plan from 3.5 to 4.5 stars, which is expected to influence payment year 2027 bonuses and reimbursement levels.

- This court-ordered rating improvement not only supports higher-quality perceptions of Clover Health’s Medicare Advantage offering, but also reshapes the financial importance of its technology-enabled care model within the value-based care ecosystem.

- We will now examine how this court-driven Medicare Star Rating upgrade could affect Clover Health’s investment narrative and long-term positioning.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Clover Health Investments Investment Narrative Recap

To own Clover Health, you need to believe its technology-enabled Medicare Advantage model can translate improving quality metrics into sustainable profitability, while managing medical costs and regulatory complexity. The court ordered upgrade of its PPO Star Rating to 4.5 stars directly supports the near term reimbursement and bonus catalyst, but it also heightens sensitivity to any future Medicare policy shifts that could weaken the value of those higher ratings.

Against this backdrop, Clover’s Q1 2026 results, with US$749.19 million in revenue and US$27.33 million in net income, are especially relevant. They show the company can be profitable even before the full financial benefit of the improved 2027 payment year Star Rating flows through, which may influence how investors weigh the upside of better reimbursement against ongoing risks from elevated utilization, competition and regulatory changes.

Yet while the higher Star Rating strengthens the story, investors should also be aware that...

Clover Health Investments' narrative projects $4.0 billion revenue and $30.9 million earnings by 2029. This requires 21.8% yearly revenue growth and an $87.8 million earnings increase from -$56.9 million today.

Uncover how Clover Health Investments' forecasts yield a $3.15 fair value, a 33% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already expecting revenue to reach about US$4.0 billion and earnings near US$57.9 million by 2029, which is far more upbeat than consensus and assumes Clover’s platform economics and wide network PPO advantages meaningfully accelerate from here, even though those projections did not yet factor in the recent Star Rating ruling and may be revisited as views on reimbursement risk and interoperability driven upside evolve.

Explore 5 other fair value estimates on Clover Health Investments - why the stock might be worth 33% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Clover Health Investments research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Clover Health Investments research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clover Health Investments' overall financial health at a glance.

No Opportunity In Clover Health Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.