Clover Health (CLOV) Is Up 25.7% After Q1 Return To Profitability And Revenue Surge – Has The Bull Case Changed?

Clover Health CLOV | 0.00 |

- Clover Health Investments, Corp. reported first-quarter 2026 results showing revenue of US$749.19 million versus US$462.33 million a year earlier, and net income of US$27.33 million versus a small loss, with basic and diluted earnings per share of US$0.05 from continuing operations.

- The return to profitability was supported by strong Medicare Advantage-driven growth, geographic expansion, and wider use of Clover’s clinical technology platform to improve care management and provider engagement.

- We’ll now examine how Clover’s return to profitability and improved operating leverage could influence its previously balanced investment narrative.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

Clover Health Investments Investment Narrative Recap

To own Clover Health, you need to believe its Medicare Advantage footprint and Clover Assistant technology can support profitable growth without eroding margins through higher medical and pharmacy costs. The Q1 2026 return to profitability reinforces the near term catalyst of improving operating leverage, but the biggest risk remains that elevated benefit expense ratios or policy changes could quickly compress those margins, so this quarter’s strength should still be viewed alongside that concern.

Among recent developments, Clover’s April 2026 move to go live on a CMS aligned TEFCA framework and real time data exchange feels especially relevant. Better interoperability can make Clover Assistant more effective, potentially supporting the same cost control and care management that underpinned Q1’s profitability, and ties directly into the catalyst of technology driven efficiency rather than simply relying on faster membership growth.

Yet against this improving story, investors should still be aware of how sensitive Clover’s margins could be if benefit expenses climb faster than expected...

Clover Health Investments' narrative projects $3.7 billion revenue and $31.7 million earnings by 2029.

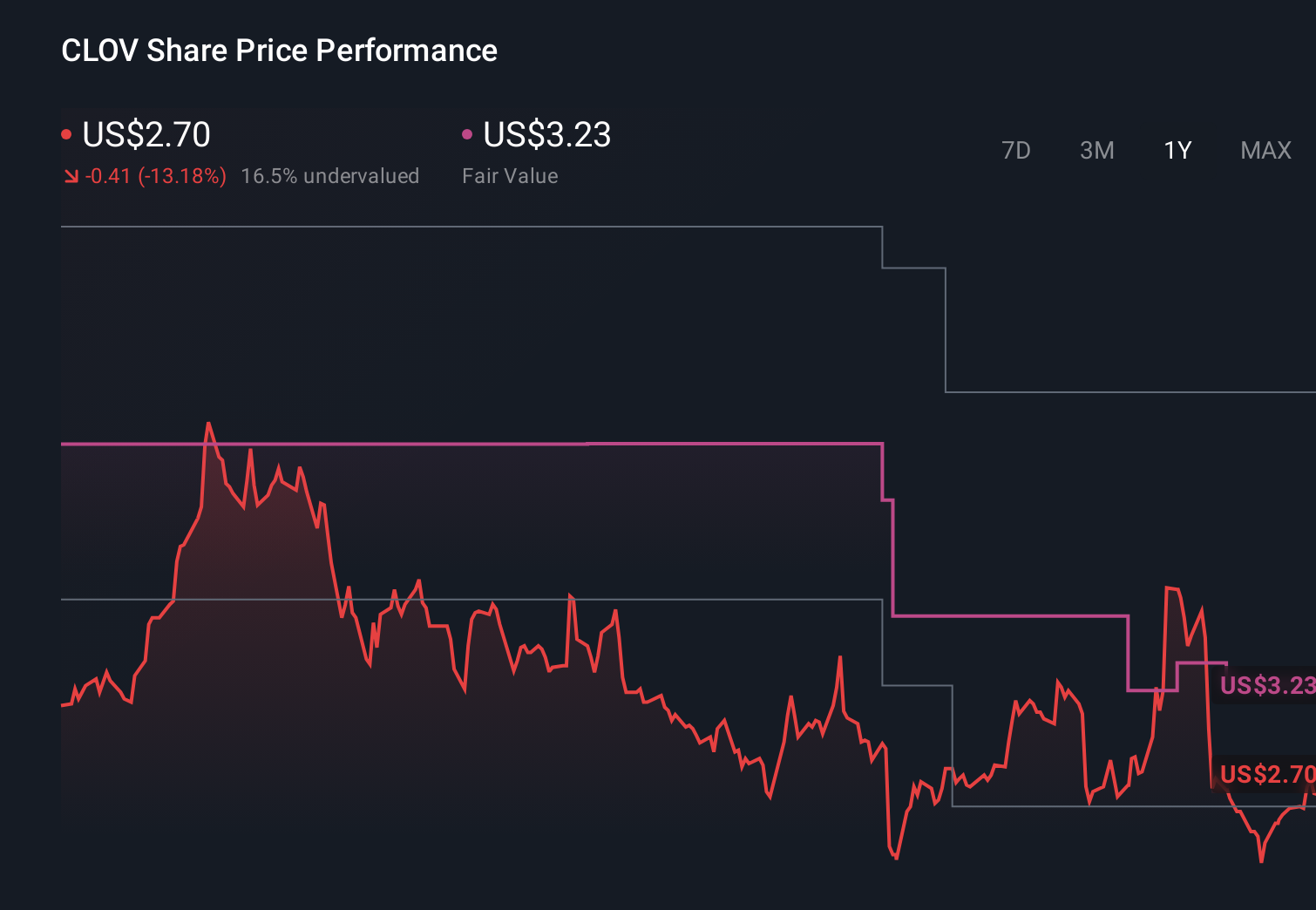

Uncover how Clover Health Investments' forecasts yield a $2.82 fair value, a 14% downside to its current price.

Exploring Other Perspectives

Before this earnings beat, the most optimistic analysts expected about US$4.0 billion of revenue and US$57.9 million of earnings by 2029, so Q1’s profit surprise could either support those projections or prompt a rethink, depending on how you weigh that upside against the ongoing risk of rising benefit costs and regulatory shifts.

Explore 6 other fair value estimates on Clover Health Investments - why the stock might be worth 14% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Clover Health Investments research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Clover Health Investments research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clover Health Investments' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.