Clover Health (CLOV) Stock Valuation After Court-Ordered Medicare Star Rating Upgrade

Clover Health CLOV | 0.00 |

A U.S. District Court ordered the Centers for Medicare & Medicaid Services to raise Clover Health Investments (CLOV) 2026 Medicare Star Rating from 3.5 to 4.5 stars, which will reshape its CMS payments and bonus eligibility for 2027.

After the court ordered Star Rating upgrade, investor interest has been strong, with Clover’s 7 day share price return of 23.5% and 90 day share price return of 138.89%. The 3 year total shareholder return is very large, although the 5 year total shareholder return remains down 60.71%.

If this kind of healthcare re rating has your attention, it could be worth scanning other potential opportunities across 40 healthcare AI stocks

With Clover now trading near analyst targets after a sharp rally and an intrinsic value estimate that still implies a large discount, the key question is whether you are seeing a genuine mispricing or a market already baking in future growth?

Most Popular Narrative: 50.2% Overvalued

The most widely followed narrative puts Clover Health Investments' fair value at $3.15, well below the last close of $4.73, which creates a clear tension between modeled value and current price.

The analysts have a consensus price target of $3.15 for Clover Health Investments based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.5, and the most bearish reporting a price target of just $2.75.

Curious what kind of revenue ramp, margin lift, and future earnings multiple have to work together to justify that fair value gap? The underlying narrative blends ambitious growth, a return to profitability, and a premium earnings multiple that is more commonly associated with mature high quality compounders. The real question is how tightly these assumptions need to line up for the model to hold.

Result: Fair Value of $3.15 (OVERVALUED)

However, there is still real execution risk. Rising medical and pharmacy utilization and ongoing GAAP net losses are both capable of undermining those long range earnings assumptions.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

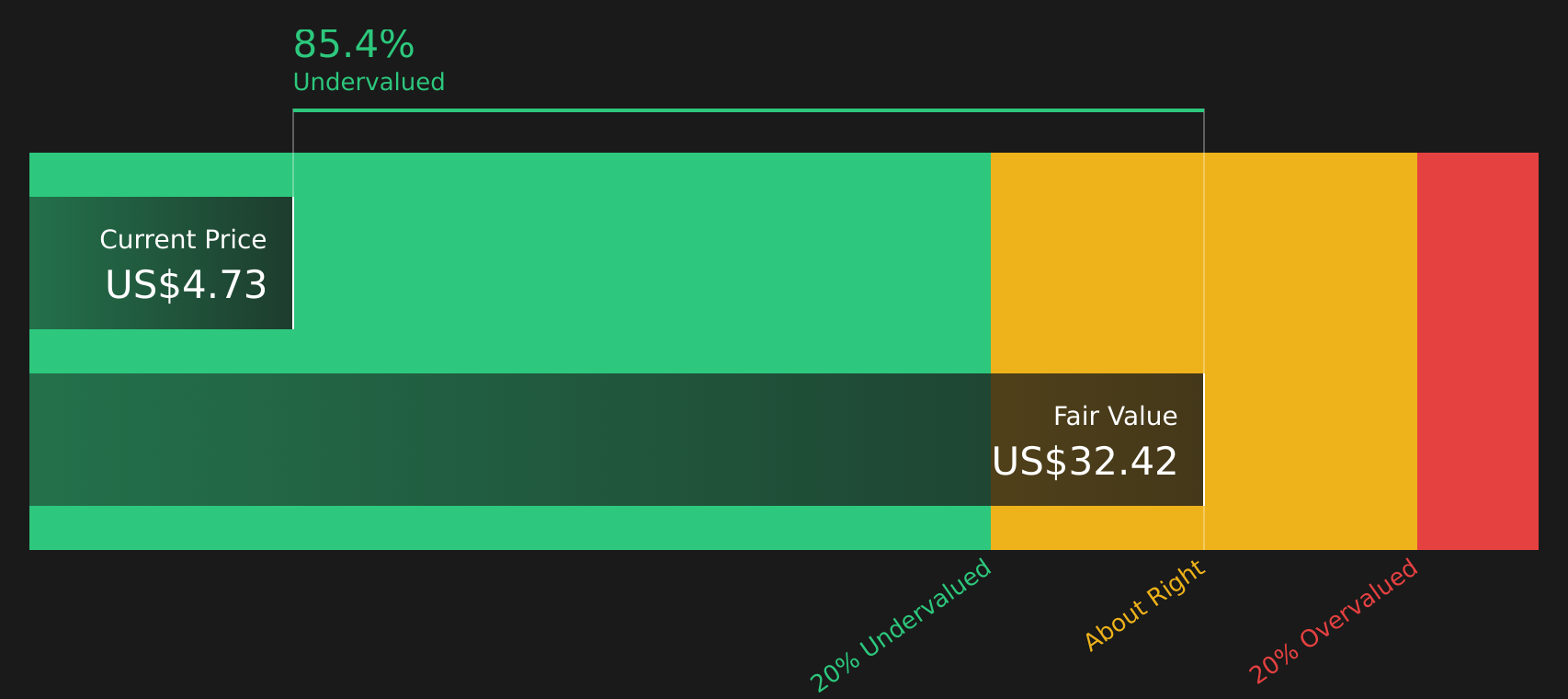

Another View: DCF Signals Deep Undervaluation

While analyst targets suggest Clover Health Investments is 50.2% overvalued at $4.73, the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $32.42. That gap is wide. Which set of assumptions feels more realistic to you?

Next Steps

If the mix of enthusiasm and concern in this story feels familiar, do not wait for consensus to form before you decide what it all means. Review the data, stress test the assumptions that matter most to you, and weigh the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If this kind of valuation tension is on your radar, broaden your watchlist now so you are not relying on a single stock to carry your thesis.

- Target stability first by scanning 70 resilient stocks with low risk scores that aim to keep downside in focus while still leaving room for upside potential.

- Hunt for value by checking screener containing 20 high quality undiscovered gems that combine solid fundamentals with stories the broader market may not be focused on yet.

- Prioritize financial strength by reviewing the solid balance sheet and fundamentals stocks screener (48 results) so you concentrate on companies backed by healthier balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.