CNO Financial Group (CNO) On Earnings Beats And Upgrade, Is The Stock Already Fully Valued?

CNO Financial Group, Inc. CNO | 0.00 |

CNO Financial Group (CNO) is back in focus after first quarter 2026 earnings and revenue surpassed expectations, followed by an Evercore ISI rating upgrade tied to a favorable long term care statutory review.

At a share price of $52.89, CNO Financial Group has enjoyed firm momentum, with a 30 day share price return of 10.39% and a 1 year total shareholder return of 43.22%, alongside recent earnings strength and the Evercore ISI upgrade.

If recent gains in CNO have you thinking about what else is moving, this could be a good moment to widen your search and check out the 19 top founder-led companies

CNO Financial Group has surged to record highs on better than expected results and a supportive long term care review. The real issue now is simple: does the current valuation still leave enough upside for new buyers?

Most Popular Narrative: 7% Overvalued

CNO Financial Group closed at $52.89, compared with a most followed fair value estimate of $49.50, so the narrative currently sits slightly behind the market price.

Accelerating growth in annuity and life/health policy sales, particularly driven by a rapidly aging U.S. population (11,000 Americans turning 65 each day) and increased focus on retirement income solutions, is expanding CNO's addressable market and supporting consistent, repeatable revenue gains. Strong momentum in digital and web-based direct-to-consumer channels, evidenced by 39% year-over-year growth and over 30% of D2C leads now from digital sources, is reducing customer acquisition costs and is expected to drive further margin expansion and scalability.

Curious how this fair value holds up if revenue barely grows but profits climb and the P/E multiple steps down over time? The narrative leans on a specific path for margins, earnings and share count that is far from automatic. The tension between a flat top line and faster earnings is where the full story gets interesting.

Result: Fair Value of $49.50 (OVERVALUED)

However, the CNO Financial Group narrative could be tested if interest rates compress investment income or if long term care claims rise closer to historical levels.

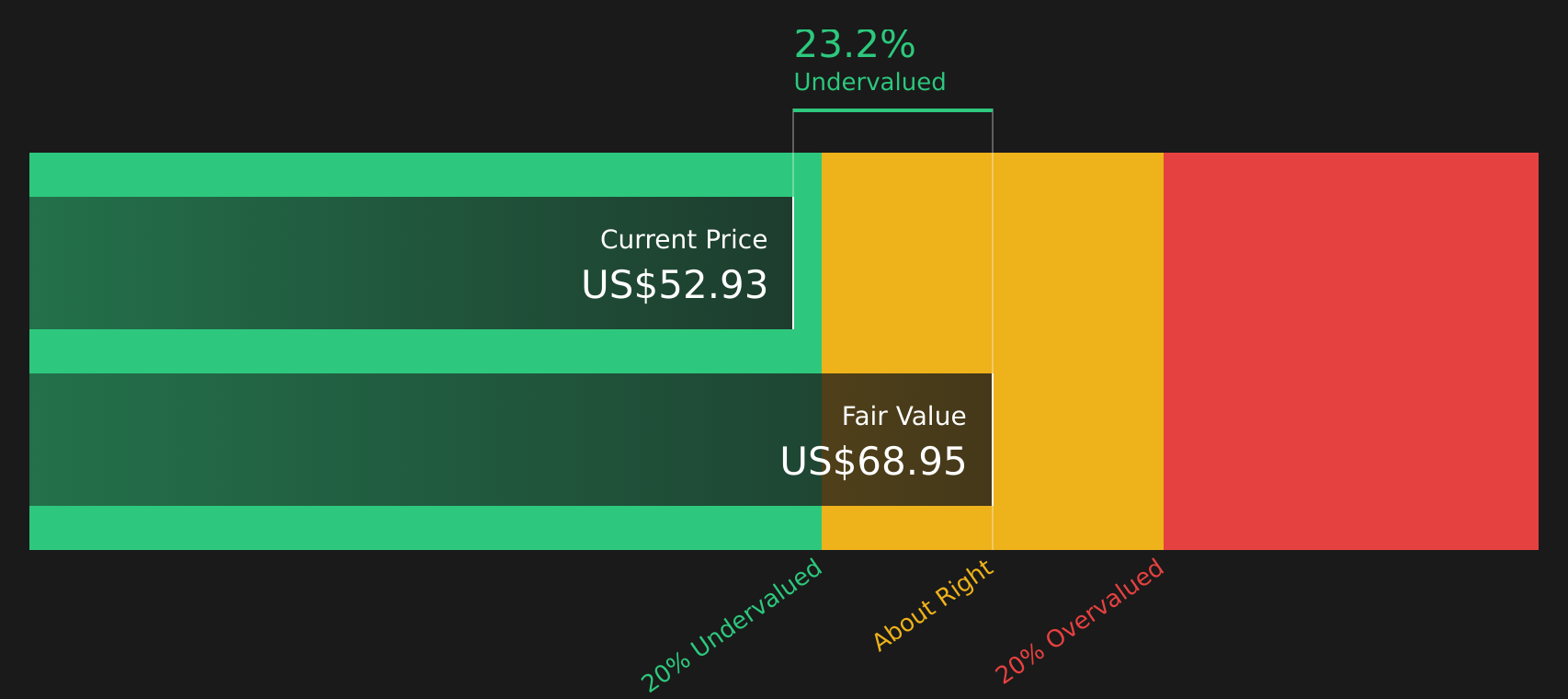

Another View: SWS DCF Model Flags Undervaluation

While the most followed narrative pegs CNO Financial Group at about 7% above its $49.50 fair value estimate, the SWS DCF model points the other way, with an estimated future cash flow value of $68.91 per share, or about 23% above the current $52.89 price. Which story do you think better fits CNO's risk and return trade off?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNO Financial Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With CNO Financial Group pulled between bullish and cautious views, this is a moment to act quickly, review the full picture, and weigh both sides by checking the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond CNO Financial Group?

Do not stop with CNO Financial Group alone. Broaden your watchlist now with fresh stock ideas that could suit very different risk profiles and income goals.

- Target potential mispricings by scanning a curated list of companies that combine quality with value using the 45 high quality undervalued stocks

- Strengthen your income stream by reviewing stocks that offer resilient cash payouts through the 9 dividend fortresses

- Prioritize capital protection by focusing on companies with steadier profiles via the 74 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.