Cognex (CGNX) Stock Looks Fully Priced As Shares Jumped 90%

Cognex Corporation CGNX | 0.00 |

Cognex stock has delivered a 90.3% return over the past year, yet both its Discounted Cash Flow (DCF) intrinsic value estimate and market multiples currently point to the shares trading at a premium.

- Over the last 12 months, Cognex has returned 90.3%, which puts extra focus on whether recent gains already reflect the company’s prospects.

- Rising interest in AI driven factory automation can support long term growth expectations for Cognex, while its premium sales multiple and exposure to trade tensions and industrial demand pose risks if those expectations soften.

- Cognex scores just 1 out of 6 on broader valuation checks, which suggests it is leaning more toward expensive than outright bargain territory.

The issue now is whether Cognex’s current share price leaves enough room between market expectations and its intrinsic value to appeal to new investors.

Is Cognex Getting Expensive on Cash Flow?

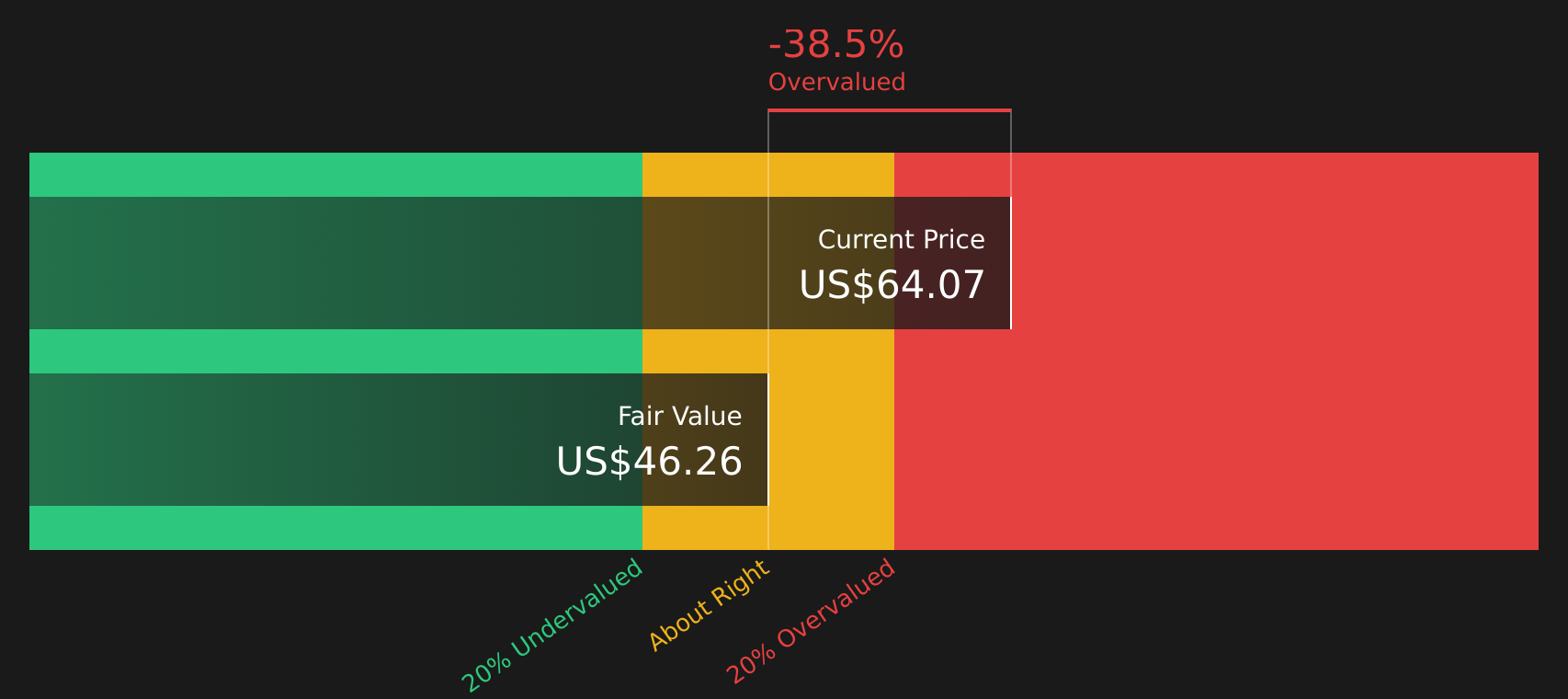

The Discounted Cash Flow (DCF) method estimates what Cognex might be worth today based on projected future cash generation. Cognex currently produces last twelve month free cash flow of about $233.8 million, with the model assuming growing cash flows over time that gradually slow as the business matures.

On these cash flow assumptions, the DCF points to an intrinsic value of about $46.06 per share, which sits well below the current share price, implying the stock screens as around 38.7% overvalued. The recent focus on AI driven factory automation and Cognex’s role in that trend helps explain why investors are willing to pay a premium to these cash flow based estimates.

Overall, the DCF output suggests Cognex stock currently appears overvalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Cognex may be overvalued by 38.7%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Does Cognex Look Pricey on Earnings?

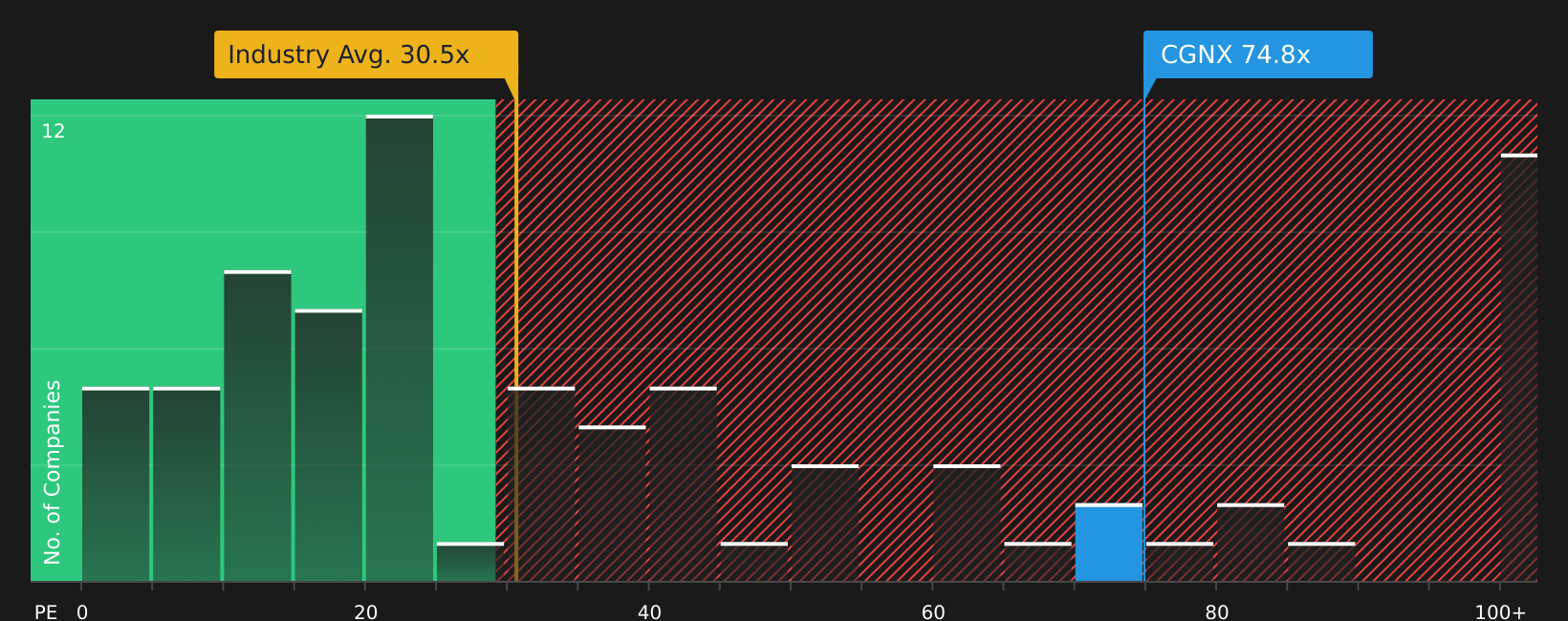

P/E is a useful yardstick for Cognex because earnings are a key focus for investors in established, profitable tech hardware companies. Cognex currently trades on a P/E of about 74.6x, compared with an Electronic industry average of roughly 30.8x and a peer group average near 55.9x, so the stock is priced at a clear premium to both its sector and closer comparables.

The fair P/E ratio implied by Simply Wall St’s model is around 42.3x, which already factors in Cognex’s growth profile, profitability, size, and risk characteristics. Against that yardstick, the current 74.6x multiple is materially higher, suggesting investors are paying well above what this framework views as a balanced level for Cognex stock.

On the P/E multiple alone, Cognex currently screens as overvalued relative to what the model suggests would be a more grounded earnings-based valuation.

The Cognex Narrative: What Would Justify Today's Price?

Simply Wall St Narratives help connect Cognex's current valuation with the specific expectations that would need to hold around its future growth, margins, and earnings. Each narrative ties a fair value estimate to a clear storyline about Cognex's potential catalysts and risks, so you can track over time which version of events appears to be aligning with how the business and stock are actually progressing, all within the Community page.

One of the top community narratives on Cognex: 16% undervalued

"Accelerating adoption of AI-powered vision solutions positions Cognex to upsell higher-value systems and increase average selling prices, supporting higher revenue and gross margin expansion..."

Do you think there's more to the story for Cognex? Head over to our Community to see what others are saying!

The Bottom Line

Cognex looks overvalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and its current earnings multiple, so the stock is already pricing in optimistic assumptions. That does not rule out further upside, but it means new buyers are paying up for the AI driven factory automation story rather than getting a clear valuation cushion. The key question from here is whether Cognex can deliver the growth, margins, and durability of demand that keep investors comfortable with this premium, or whether expectations eventually settle back toward more moderate levels.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.