Colgate-Palmolive (CL) Valuation Check As Analyst Upgrades Highlight Emerging Market Growth Potential

Colgate-Palmolive Company CL | 85.14 | -0.32% |

Recent analyst upgrades and increased confidence in Colgate-Palmolive (CL), tied to early growth signals in emerging markets and lower reliance on the US, have renewed attention on how the stock is currently priced.

The recent analyst upgrades, alongside a series of rating revisions across the street, appear to have coincided with stronger trading interest. Colgate-Palmolive’s 7 day share price return of 9.68% and year to date share price return of 8.83% contrast with a 1 year total shareholder return decline of 1.44%, hinting at momentum rebuilding after a softer period.

If you are reassessing consumer staples after these moves, it could be a good time to broaden your watchlist with fast growing stocks with high insider ownership.

With Colgate-Palmolive now trading at $84.55, sitting roughly 4% below the average analyst target of about $88 and with a flagged intrinsic discount of around 32%, you have to ask: is there still an opportunity here, or is the market already pricing in any future growth?

Most Popular Narrative: 3.3% Undervalued

The most followed narrative puts Colgate-Palmolive’s fair value at about US$87.47 per share, only slightly above the last close of US$84.55, which frames the recent move as modest rather than extreme.

Productivity and restructuring initiatives ($200 to $300 million over three years) are designed to free up resources for innovation, digital, and R&D investments, enabling incremental margin expansion and additional reinvestment for growth.

Want to see what sits under that fair value estimate? Revenue expectations, margin tweaks and a richer future P/E are doing the heavy lifting. Curious which assumptions matter most here?

Result: Fair Value of $87.47 (UNDERVALUED)

However, the picture could change quickly if cost pressures remain elevated or if softer demand in markets like China and India persists longer than analysts currently factor in.

Another View: Earnings Multiple Sends A Different Signal

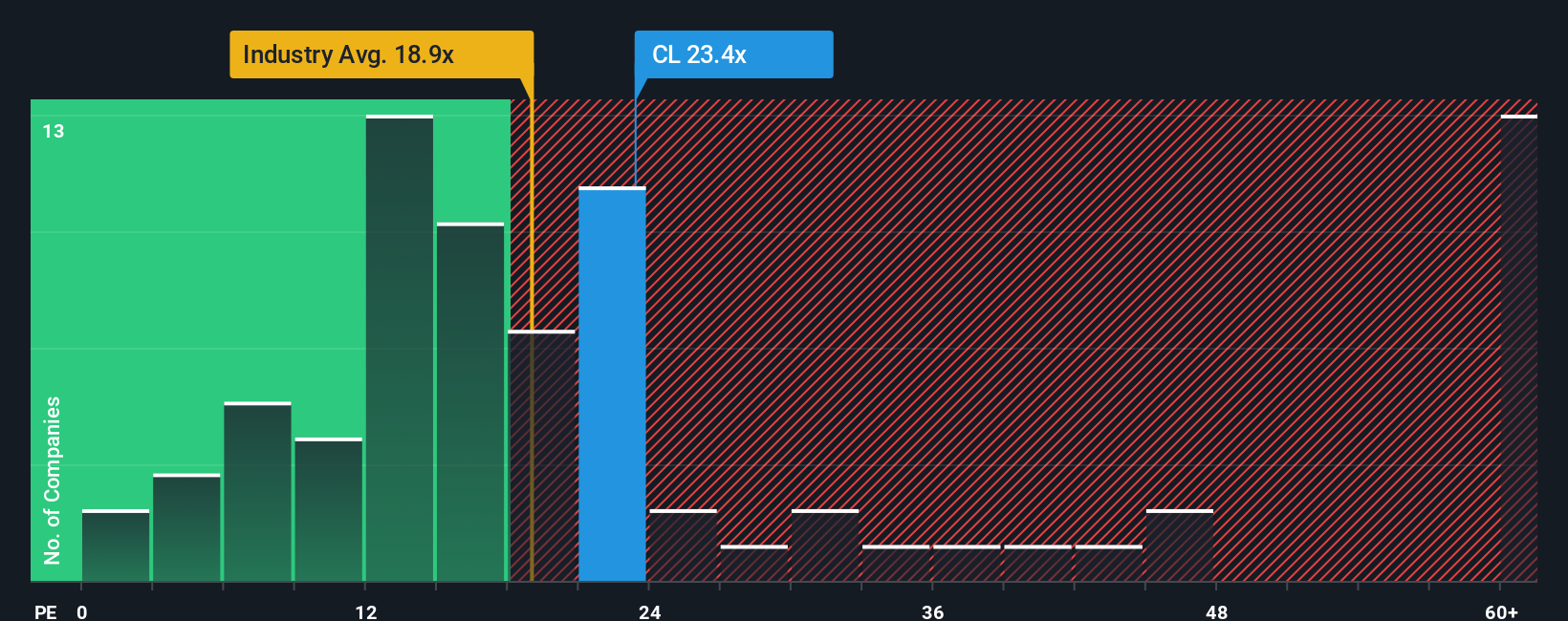

While the SWS narrative and DCF work point to Colgate-Palmolive trading below fair value, the earnings multiple paints a tighter picture. At a P/E of 23.4x versus 17x for the global Household Products industry, 20.6x for peers and a fair ratio of 19x, you are paying a clear premium. Is that gap justified by your own expectations for future earnings and resilience, or does it leave less room for error than the DCF suggests?

Build Your Own Colgate-Palmolive Narrative

If you see the numbers differently, or simply want to test your own assumptions, you can put together a personalised view in a few minutes: Do it your way.

A great starting point for your Colgate-Palmolive research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger watchlist, do not stop at one stock. Widen your search now or you might miss something important.

- Spot potential value ahead of the crowd by reviewing these 875 undervalued stocks based on cash flows that currently look cheap based on their cash flows and fundamentals.

- Position your portfolio for long term tech shifts by scanning these 24 AI penny stocks shaping new applications of artificial intelligence across multiple industries.

- Add income angles to your research by checking out these 12 dividend stocks with yields > 3% that offer yields above 3% while still passing key financial quality checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.