COMPASS Pathways (CMPS) Gets A Fresh Valuation Test On New Phase 3 Data

COMPASS Pathways Plc Sponsored ADR CMPS | 0.00 |

Why the COMP360 trial update matters for COMPASS Pathways stock

COMPASS Pathways (NasdaqGS:CMPS) released six month data from its pivotal Phase 3 COMP006 trial of COMP360 in treatment resistant depression, confirming rapid onset, durable benefit and a generally well tolerated safety profile.

For investors, this event ties clinical outcomes directly to COMPASS Pathways' path toward potential commercialization. A rolling New Drug Application is already underway, and management has indicated an aim for a first half 2027 launch, subject to regulatory decisions.

Against this clinical backdrop, COMPASS Pathways’ share price has shown strong momentum, with a 30 day share price return of 19.05% and a 90 day share price return of 150.27%. At the same time, the 1 year total shareholder return of 295.61% contrasts with a 5 year total shareholder return that remains significantly lower, highlighting both recent enthusiasm and a still mixed long term record.

If this kind of sharp move in a single biotech stock has your attention, it may be a good time to broaden your watchlist and check out 40 healthcare AI stocks.

After a surge that has taken COMPASS Pathways to a market value of about US$1.8b, backed by encouraging COMP360 data and a still loss-making profile, does the balance of risk and potential reward still lean toward buyers, or has the easy part of the move already passed?

Most Popular Narrative: 73.4% Undervalued

The most followed valuation narrative for COMPASS Pathways places fair value at $52.55, far above the last close of $13.97. This helps explain why some investors see the recent rally as only part of a larger story.

The assumed bullish price target for COMPASS Pathways is $52.55, which represents up to two standard deviations above the consensus price target of $21.75. This valuation is based on what can be assumed as the expectations of COMPASS Pathways's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

Curious what kind of revenue ramp, margin profile and future earnings multiple are baked into that fair value, and how far those assumptions stretch current analyst views? The full narrative walks through a detailed path from zero revenue today to a much larger business, plus the earnings power that would need to sit behind COMPASS Pathways to support that price tag.

Result: Fair Value of $52.55 (UNDERVALUED)

However, this COMPASS Pathways narrative depends on smooth trial timelines and regulatory progress, and any delay or stricter FDA requirements could quickly change sentiment.

Another view on COMPASS Pathways valuation

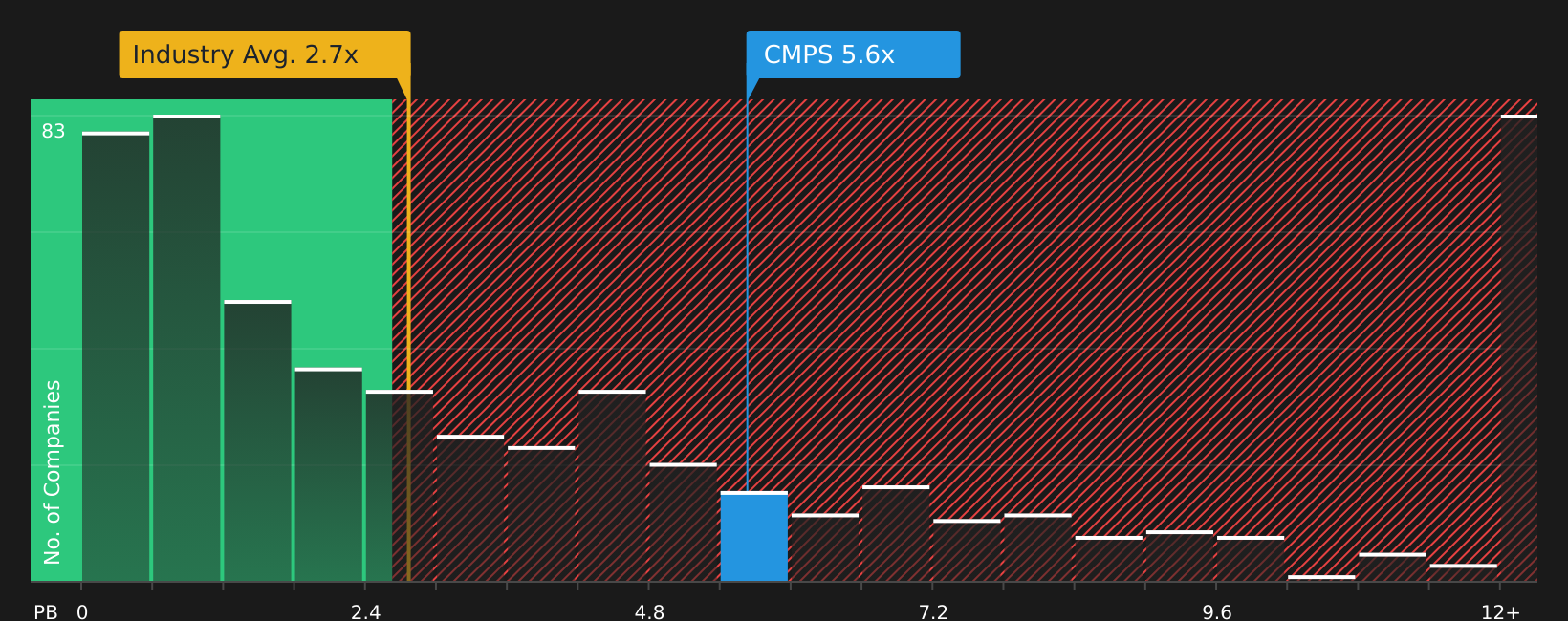

That bullish fair value of $52.55 for COMPASS Pathways sits beside a very different message from simple market ratios. On a P/B of 5.8x, the stock trades at more than double the US Biotechs industry average of 2.8x, even though it is currently loss making.

Compared with a peer average P/B of 41.2x, COMPASS Pathways looks much cheaper on this single metric. This could point to either a cushion if sentiment cools or less upside than the most optimistic targets suggest. Which signal do you trust more when real revenue is still ahead?

Next Steps

With sentiment clearly split on COMPASS Pathways, it may be useful to act promptly, review the data yourself and weigh both the concerns and potential upside in the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond COMPASS Pathways?

Round out your COMPASS Pathways research by lining it up against other opportunities, so you are not relying on a single stock for your next move.

- Target potential upside in quality companies trading below their estimated worth by scanning the 44 high quality undervalued stocks.

- Strengthen your portfolio's foundations by reviewing the solid balance sheet and fundamentals stocks screener (47 results), which is packed with companies that show robust financial footing.

- Get ahead of the crowd by checking the screener containing 19 high quality undiscovered gems that many investors may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.