Consumer Staples Stocks Worth A Look As Tech Sell Offs Push Investors Toward Defensive Names

Kraft Heinz Company KHC | 0.00 |

Tech stocks are under pressure after sharp sell offs in Asia and fresh worries about how higher device and AI costs will hit consumers. For many investors, this is a prompt to revisit the role of Consumer Staples stocks, where demand can sometimes be steadier when people cut back elsewhere. This article looks at three larger Consumer Staples companies from a recent screener that appear especially exposed to the latest tech related news, and explores how that backdrop might influence their risk profile, income potential, and role in a diversified portfolio.

Andersons (ANDE)

Overview: The Andersons is an agriculture and renewable fuels company based in Ohio that trades and processes grains like corn, wheat and soybeans, sells plant nutrients and fertilizers, and operates ethanol and other biofuel businesses across the United States, Canada, Mexico and internationally. It also provides logistics and merchandising services for grain, feed ingredients and fuel products, positioning the company across several key parts of the food and energy supply chain.

Operations: The Andersons generates about US$8.2b in revenue from its Agribusiness segment and roughly US$2.8b from Renewables, with most sales coming from the United States and the rest spread across Canada, Mexico and other international markets.

Market Cap: US$2.38b

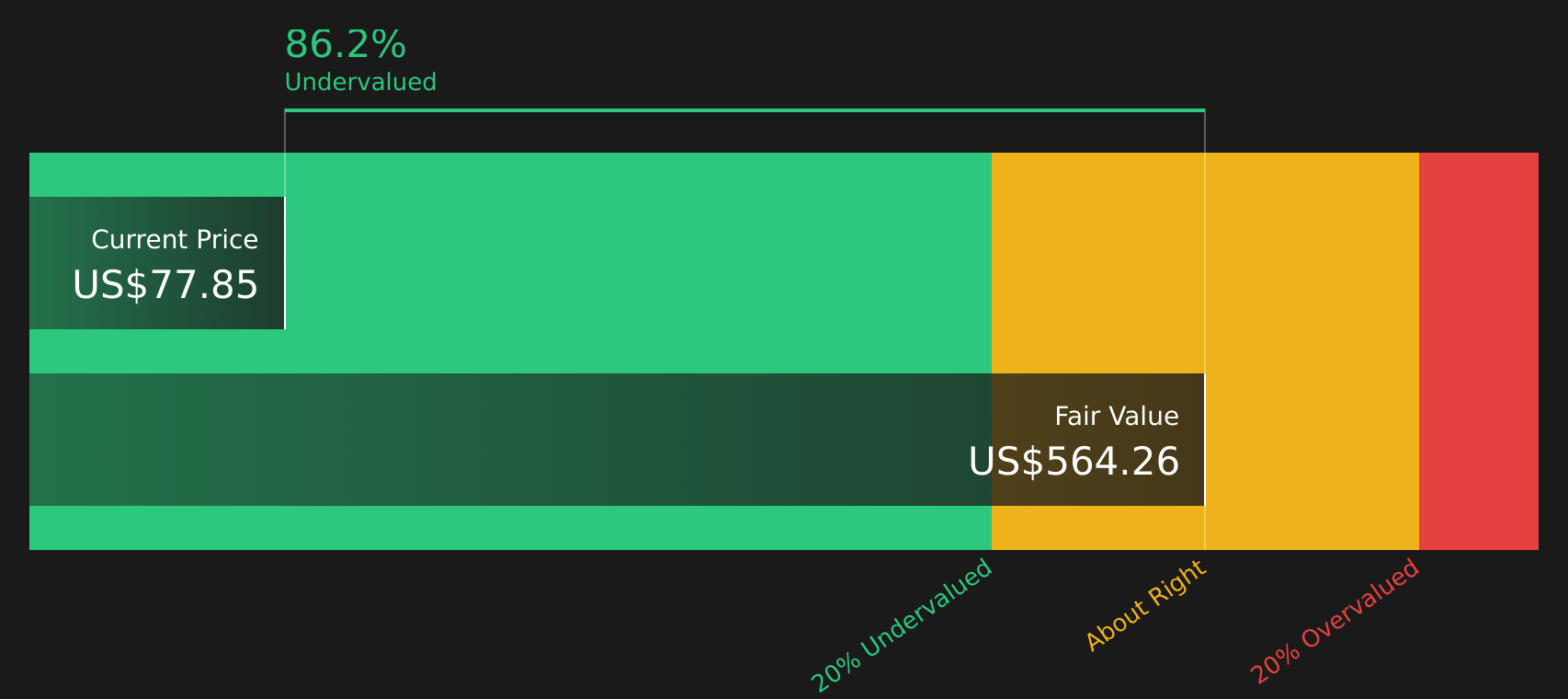

For investors questioning expensive tech stocks, Andersons offers exposure to grain, plant nutrients and ethanol, areas tied to everyday food and fuel demand that can sometimes feel more resilient when consumers pull back on discretionary gadgets. Analysts in some cases project earnings growth well ahead of revenue, citing factors such as full ownership of ethanol plants, cost discipline and potential benefits from renewable fuel tax credits. Some internal valuation work also characterizes the stock as trading well below a cited fair value estimate. The flip side is meaningful exposure to volatile commodity prices, higher reliance on external borrowing and recent insider selling, all of which deserve close attention. That mix of supportive factors and notable risks is what makes Andersons a company some investors may choose to watch more closely.

Andersons’ mix of grain, fertilizer and ethanol exposure, along with claims of a discount to fair value, raises a bigger question: what are investors missing in the 3 key rewards and 2 important warning signs (1 is major!)

Bunge Global (BG)

Overview: Bunge Global is a large agribusiness and food company that buys, processes and sells oilseeds and grains, turning crops like soybeans, softseeds and corn into vegetable oils, animal feed, biodiesel and milled products for food companies, fuel producers and farmers around the world.

Operations: Bunge Global generates most of its revenue from Soybean Processing and Refining at about US$39.9b, followed by Grain Merchandising and Milling at roughly US$25.0b, Softseed Processing and Refining at around US$15.2b, and Tropical Oils and Specialty Ingredients at about US$5.1b, partly offset by eliminations and adjustments.

Market Cap: US$21.1b

In a market where expensive tech stocks are under scrutiny, Bunge Global offers exposure to the core of global food supply, yet its story is not without tension. The company is integrating the large Viterra merger, which could widen its reach and improve margins, while analysts expect earnings to grow much faster than revenue and forecast a meaningful recovery in profitability. At the same time, recent margin pressure, earnings declines and heavy spending on capacity, renewable fuels and sustainability projects show that execution risk is real, especially with complex regulations and biofuel policies in play. For investors, that mix of essential products, ambitious growth plans and funding pressure raises an important question about whether the current valuation fully reflects both the upside and the risks still ahead.

Bunge Global’s earnings story and the Viterra merger could be masking a much bigger shift in how this business is valued, so it is worth reviewing the 3 key rewards and 4 important warning signs (2 are major!)

Kraft Heinz (KHC)

Overview: Kraft Heinz is a global packaged food and beverage company that owns household brands like Heinz, Kraft, Philadelphia, Oscar Mayer and Capri Sun, selling condiments, cheese, ready meals, snacks, desserts, drinks and meats to supermarkets, foodservice customers and online retailers worldwide.

Operations: Kraft Heinz generates about US$18.6b of revenue from North America, around US$3.6b from International Developed Markets and roughly US$2.9b from Emerging Markets, giving it a broad mix of mature and faster growing regions.

Market Cap: US$27.2b

For investors rotating out of expensive tech, Kraft Heinz offers something very different: essential pantry products, a sizeable income stream and a company that is explicitly leaning into brand investment instead of financial engineering. Recent quarters show solid cash generation, a maintained US$0.40 quarterly dividend and management committing around US$600m to improve products, marketing and operations. At the same time, some analysts flag concerns about leverage, pricing power and a dividend that is not fully supported by earnings. With tech stocks under pressure from higher device and AI costs, some investors are asking whether a steady, globally diversified staples business with well known brands and ongoing restructuring is being overlooked while attention stays focused on volatility in chips and software.

Kraft Heinz might be quietly resetting its story as steady cash, a US$0.40 dividend, and US$600m of brand investment pull against leverage and pricing concerns, so it is worth reading the 2 key rewards and 2 important warning signs

The three Consumer Staples stocks in this list are only a starting point, as the full screener identified 19 more companies with equally interesting Consumer Staples stories in the Consumer Staples Stocks screener. With Simply Wall St, you can quickly analyze and filter for the specific catalysts, risk factors and income characteristics that matter to you so you can identify the Consumer Staples stocks that fit your highest conviction ideas.

Take Control of Your Investment Journey

If Bunge Global or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move first, and the best entry points often appear just as momentum builds or drops off. Scan these curated shortlists before the crowd piles in and act now.

- Spot strong cash generators early by tracking companies in the 43 high quality undervalued stocks while they are still flying under most investors' radar.

- Focus on real earnings power instead of hype by zeroing in on the 60 profitable AI stocks that aren't just burning cash before momentum traders get caught chasing late moves.

- Position for long term demand shifts by reviewing the 89 nuclear energy infrastructure stocks while sentiment is still forming and valuations can be more forgiving.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.