Copa Holdings (CPA) Stock Could Be 8.5% Undervalued After May Traffic Data

Copa Holdings, S.A. Class A CPA | 0.00 |

Copa Holdings (NYSE:CPA) is back in focus after releasing preliminary traffic data for May 2026. The report shows year-over-year changes in capacity, demand, and load factor that help investors reassess the airline stock.

Copa Holdings has seen momentum build in recent months, with a 17.84% 1 month share price return and a 53.14% 1 year total shareholder return, as May traffic data refocuses attention on growth and risk expectations.

If Copa Holdings' recent move has you reassessing airline exposure, it could be a good moment to broaden your search and check out 20 top founder-led companies

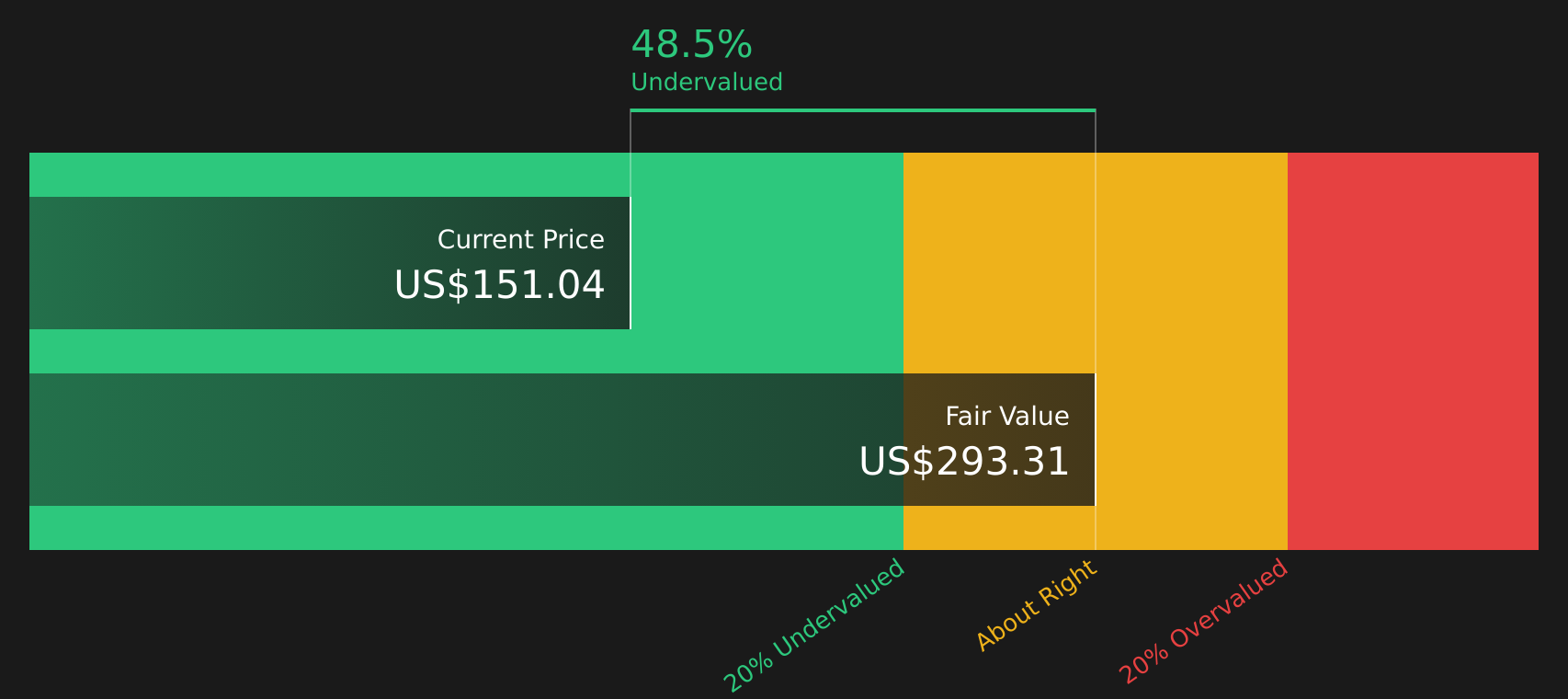

With Copa Holdings trading at $151.04, sitting about 10.6% below the average analyst price target yet showing an intrinsic value estimate that points to a premium, investors have to ask whether there is still mispricing here or whether the market is already baking in future growth.

Most Popular Narrative: 8.5% Undervalued

Copa Holdings' most followed valuation narrative pegs fair value at $165.13, above the latest close at $151.04, which puts the current price under scrutiny.

The company's disciplined cost management, ongoing seat densification, and delivery of more fuel efficient Boeing 737 MAX aircraft enable Copa to maintain industry leading net and operating margins. This gives it resilience and earnings growth potential even in a competitive environment with downward pressure on yields. Strengthening financial flexibility (high cash balance, low net debt to EBITDA, and a largely unencumbered fleet) underpins Copa's ability to invest in network growth, fleet renewal, and opportunistic initiatives (such as cargo expansion and code share partnerships). All of these factors diversify earnings streams and mitigate risk to future earnings.

Want to see what underpins that valuation gap on Copa Holdings? The narrative leans on steady revenue expansion, firm margins, and a future earnings multiple that has to hold up over time.

Result: Fair Value of $165.13 (UNDERVALUED)

However, Copa Holdings' narrative could be challenged if competitive pressure continues to push yields lower or if jet fuel costs rise faster than the company can offset through efficiencies.

Another View on Copa Holdings' Valuation

While the most followed narrative sees Copa Holdings as 8.5% undervalued based on fair value estimates, the Simply Wall St DCF model presents a different perspective. At $151.04, the stock is above an implied future cash flow value of $128.13, which suggests an overvalued result. Which story do you think better fits your thesis?

For a closer look at how this cash flow view is built and how sensitive it is to the assumptions underneath it, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Copa Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern around Copa Holdings has raised new questions for you, take a moment to review the numbers yourself and consider both sides using 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Copa Holdings?

Do not stop with Copa Holdings when there are other stocks that could fit your goals. Use these focused tools to quickly surface ideas that match your style.

- Target dependable cash flow by reviewing companies in the 8 dividend fortresses that may appeal if income is a key part of your plan.

- Zero in on value opportunities by checking the screener containing 20 high quality undiscovered gems that might not yet be widely followed but still show solid fundamentals.

- Prioritise resilience by filtering for stocks in the 66 resilient stocks with low risk scores that align with a more cautious approach to risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.