Corteva (CTVA) Stock Could Be 13% Undervalued After FMC Herbicide Deal

Corteva Inc CTVA | 0.00 |

Why the new FMC partnership matters for Corteva stock

Corteva (CTVA) recently signed a multi-year, co-exclusive supply and license agreement with FMC Corporation for rimisoxafen herbicide technology, giving the company another tool in corn and soybean crop protection.

The deal covers North and South American markets, includes a US$200 million prepurchase payment from Corteva, and allows both companies to create their own premix formulations. Commercial sales are targeted by the end of the decade, pending approvals.

At a share price of US$78.59, Corteva has delivered a 16.0% year to date share price return and a 41.9% total shareholder return over three years. Recent FMC news and the upcoming conference appearance are keeping interest in the longer term growth story alive despite a slightly weaker 30 day share price return.

If you want to see what else is shaping the market beyond agricultural stocks, this is a good moment to scout 20 top founder-led companies

Corteva now trades around US$78.59 with double digit year to date and multi year total returns, plus a partnership that some investors view as a new growth lever. Is there still value on the table, or is the market already pricing in the future potential?

Most Popular Narrative: 13% Undervalued

The most followed narrative puts Corteva’s fair value at about $90.05, compared with the recent $78.59 close, and roots that gap in earnings and margin expectations.

Advancements in Corteva's innovation pipeline, including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing, enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Analysts are effectively sketching a playbook built on steady revenue gains, widening margins and a future earnings multiple that sits above the wider chemicals sector. Curious which assumptions really carry that valuation story and how sensitive the fair value is to them? The full narrative breaks those moving parts into clear, testable numbers.

Result: Fair Value of $90.05 (UNDERVALUED)

However, there are still watchpoints for Corteva, including pressure from low cost generics in crop protection and currency swings in key emerging markets that could unsettle those assumptions.

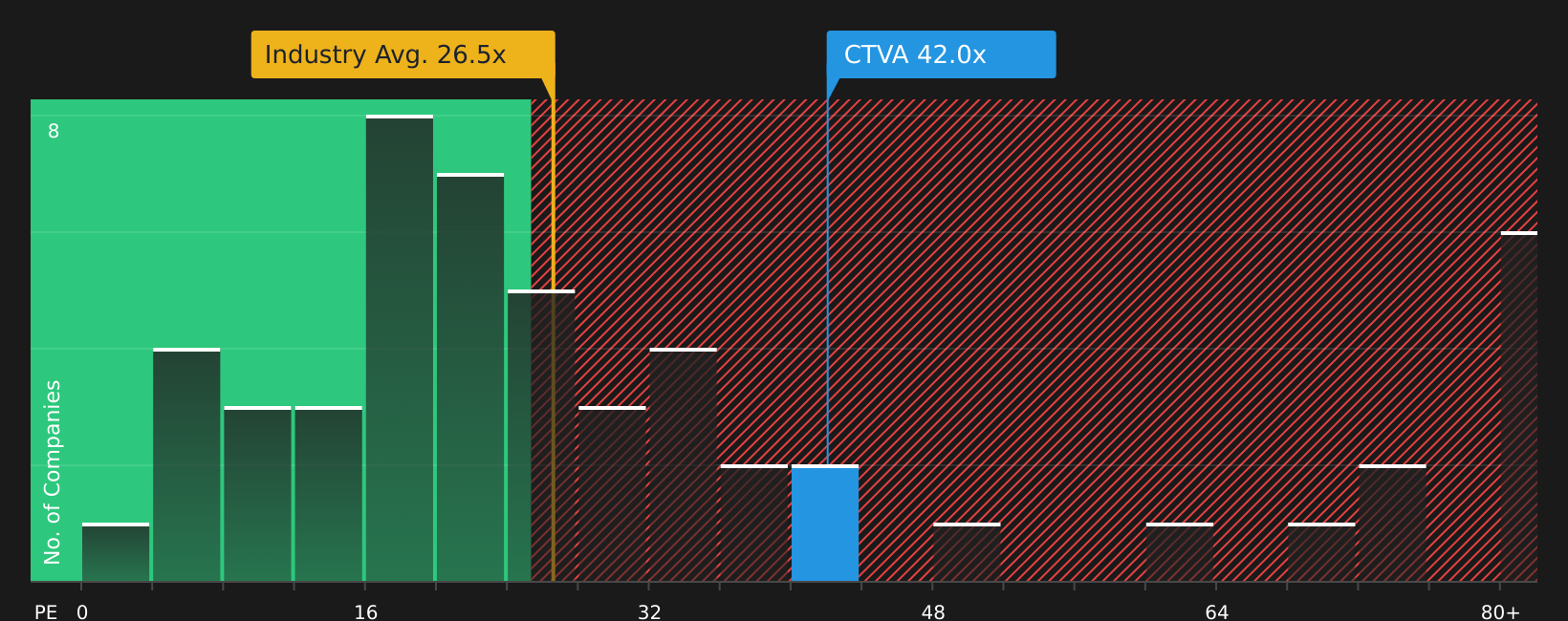

Another View: What Corteva’s P/E Is Telling You

The first narrative leans on fair value of US$90.05 for Corteva using analyst earnings and margin forecasts. On current numbers though, Corteva trades on a P/E of 42x, compared with a US Chemicals industry average of 26.5x and a fair ratio of 25.6x, which implies a much richer pricing.

If the market eventually moves closer to that fair ratio, today’s P/E leaves less room for error than a simple discount to fair value might suggest. The real question is whether you think Corteva’s earnings profile can keep justifying that premium.

Next Steps

With Corteva attracting both optimism and caution, this is a good time to move quickly, review the underlying data, and weigh the 3 key rewards and 1 important warning sign

Looking for more ideas beyond Corteva?

If you are serious about building a stronger portfolio alongside Corteva, this is the moment to widen your lens and scan for fresh opportunities.

- Spot potential mispriced opportunities early by scanning 45 high quality undervalued stocks that combine quality fundamentals with prices that some investors may consider attractive.

- Strengthen your income stream by reviewing 8 dividend fortresses that focus on higher yielding companies with an emphasis on stability.

- Reduce overall portfolio stress by considering 66 resilient stocks with low risk scores that screen for resilience and lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.