Coterra Energy (CTRA) Valuation Check After Strong Recent Share Price Momentum

Coterra Energy CTRA | 0.00 |

Why Coterra Energy is on investors’ radar

Coterra Energy (CTRA) is drawing attention after a recent share price move, with the stock delivering a 6.7% gain over the past week and a 24.5% return over the past 3 months.

At a latest share price of $35.91, Coterra Energy’s recent 6.7% 7 day share price return sits within a broader pattern, with a 24.5% 90 day share price return and a 49.2% 1 year total shareholder return pointing to strong positive momentum.

If you are comparing Coterra’s move with other opportunities in the resource space, it can be useful to see how oil and gas names stack up against 8 top copper producer stocks

With Coterra trading at $35.91 and an implied upside of around 4% to the average analyst price target, plus a modelled intrinsic value suggesting a wider discount, the key question is whether this reflects genuine value or a market that has already priced in future growth.

Most Popular Narrative: 40.5% Overvalued

According to the most followed narrative from Bejgal, Coterra Energy’s fair value sits at $25.55, which is well below the latest $35.91 share price.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production. Over 10 years, its extensive inventory and focus on innovation position it for sustainable long-term growth.

Curious what sits behind that long runway idea? The narrative leans heavily on LNG volumes, thicker margins from premium assets, and a richer future earnings multiple. The exact mix of growth, profitability, and required return is where the story really gets interesting.

Result: Fair Value of $25.55 (OVERVALUED)

However, this upbeat LNG-led story still leans on assumptions around global gas demand and pricing, and on regulatory decisions in key regions like New Mexico.

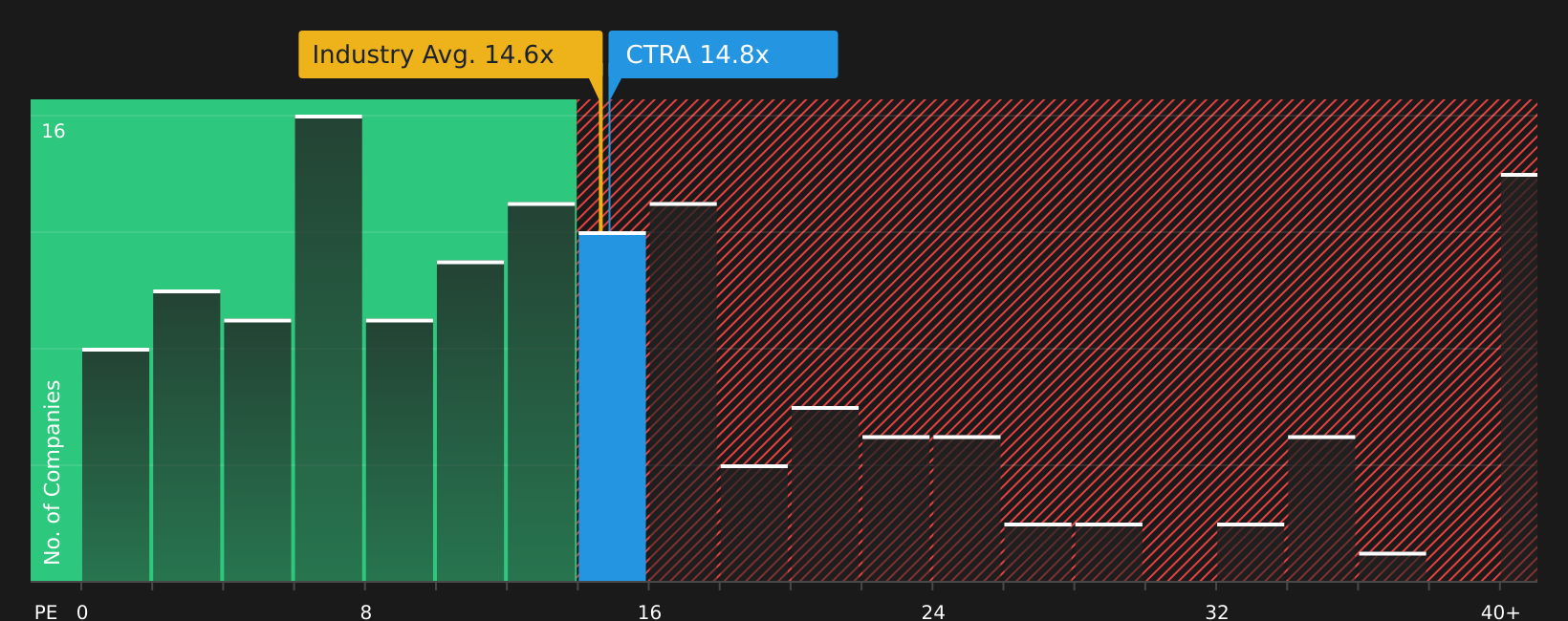

Another way to look at value

Bejgal’s narrative points to Coterra being 40.5% overvalued at $35.91, but earnings based metrics tell a different story. The current P/E of 15.9x sits under the peer average of 24.3x and below a fair ratio of 22.5x, which suggests the market may be pricing in more risk than the numbers imply. So which story do you think is closer to reality?

Next Steps

With sentiment clearly split between valuation risks and earnings based support, it helps to move fast and look at the underlying numbers yourself so you can decide where you stand on Coterra’s story. A good place to start is the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Coterra has your attention, do not stop here. Broadening your watchlist can help you spot opportunities you might otherwise miss in plain sight.

- Target potential mispricings by scanning for quality names trading below what their fundamentals suggest through the 51 high quality undervalued stocks.

- Strengthen your focus on resilience by checking companies that pair solid finances with staying power using the 74 resilient stocks with low risk scores.

- Get ahead of the crowd by reviewing financially sound companies that are not widely followed via the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.