Coty (COTY) Is Up 10.7% After Handing Back Gucci Beauty License To Kering For US$400 Million

Coty Inc. Class A COTY | 0.00 |

- In early July 2026, Coty Inc. announced it would transition the Gucci Beauty license back to Kering for about US$400 million, continue operating the brand through at least June 30, 2027, and use the proceeds for debt reduction, core prestige investments, and organizational streamlining.

- The deal not only reshapes Coty’s prestige portfolio by exiting a key licensed brand but also resolves all related litigation with Kering and accelerates Coty’s shift toward a more focused, centrally managed operating model.

- We’ll now examine how handing back the Gucci Beauty license, while using proceeds to reduce debt and refocus prestige, reshapes Coty’s investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Coty Investment Narrative Recap

To own Coty today, you have to believe it can turn an unprofitable, leveraged beauty portfolio into a more focused, higher quality business, while managing pressure from retailer destocking and intense promotional activity. The Gucci Beauty license sale adds cash and reduces legal noise, but also removes a prestige franchise tied to blockbuster launches, so it directly touches both the near term earnings catalyst and the key risk around dependence on licensed brands.

The July 2026 announcement of Coty.Curated organizational changes looks tightly linked to the Gucci transition, since Coty plans to use proceeds to sharpen its core prestige focus. Centralizing prestige R&D, sustainability, and supply chain under one leader may help execution around new launches and margin improvement, which many investors see as the main catalyst once destocking eases. At the same time, leadership turnover introduces its own uncertainty about how effectively these plans will be delivered.

Yet investors should also weigh how handing back Gucci heightens Coty’s exposure to its remaining prestige licenses and what happens if consumer enthusiasm for those brands...

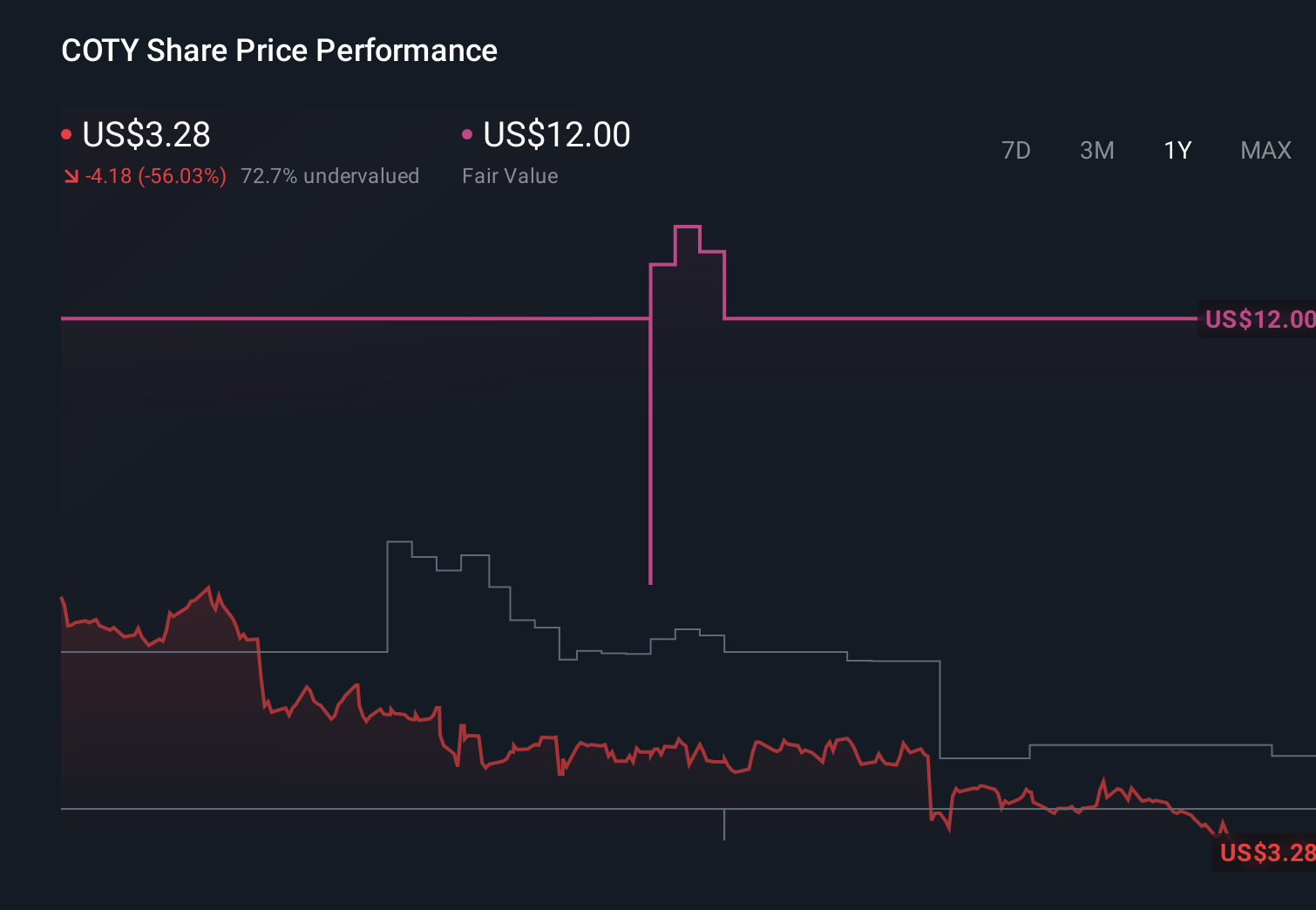

Coty's narrative projects $5.9 billion revenue and $411.8 million earnings by 2029. This requires revenue to remain fairly flat over the next few years and a $957.6 million earnings increase from -$545.8 million today.

Uncover how Coty's forecasts yield a $3.17 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Optimistic analysts were once assuming Coty could lift revenues to about US$6.2 billion and earnings near US$688.6 million, but the Gucci exit and heavy reliance on prestige fragrance show how different your view might be on the balance between growth potential and concentration risk.

Explore 5 other fair value estimates on Coty - why the stock might be worth over 4x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

No Opportunity In Coty?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.