Could Google’s TurboQuant Shift AI Memory Needs and Subtly Reshape Photronics’ (PLAB) Chipmaking Role?

Photronics, Inc. PLAB | 0.00 |

- In recent trading, semiconductor maker Photronics was caught up in a sector-wide reaction after Google revealed its TurboQuant algorithm, a tool that could sharply reduce the memory needs of artificial intelligence models.

- This development has prompted investors to reassess how advances in AI efficiency might ripple through the broader chip supply chain, including specialist suppliers such as photomask producers.

- We’ll now examine how concerns about AI-driven memory demand, highlighted by Google’s TurboQuant news, could influence Photronics’ existing investment narrative.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 26 companies in the world exploring or producing it. Find the list for free.

Photronics Investment Narrative Recap

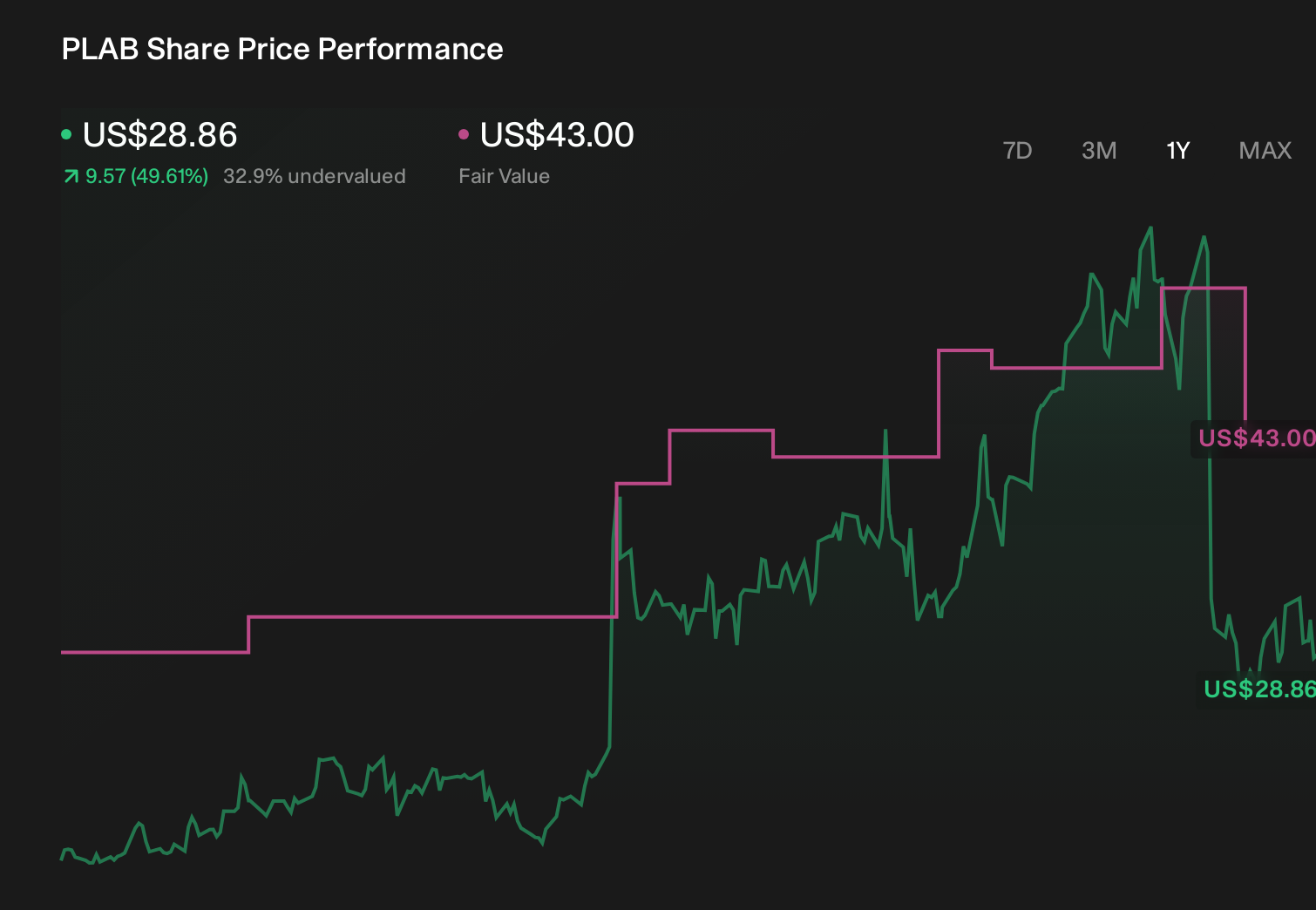

To own Photronics, you generally need to believe that demand for photomasks across both mainstream and advanced nodes will support its heavy investment in new tools and capacity. The Google TurboQuant news speaks directly to memory demand, but its impact on Photronics’ near term revenue drivers and the key risks around capital intensity and order visibility does not appear material at this stage, given the company’s broader exposure across IC and display customers.

What does feel more directly relevant is Photronics’ Q1 2026 update, where revenue reached US$225.07 million with net income of US$42.94 million and management guided Q2 sales to US$212 million to US$220 million. This recent confirmation of near term demand and the maintained guidance range helps frame the TurboQuant headline as one factor among many for investors weighing short term earnings variability, capital spending needs and the evolving AI memory story.

Yet for all of this, the limited order backlog visibility and exposure to sharp swings in IC design activity remain risks investors should be aware of...

Photronics' narrative projects $973.4 million revenue and $138.1 million earnings by 2029. This requires 4.1% yearly revenue growth and a modest $1.6 million earnings increase from $136.5 million today.

Uncover how Photronics' forecasts yield a $47.00 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community value Photronics between US$19.10 and US$47.00 per share, showing how far opinions can spread. Set that against concerns about volatile IC demand and short backlog visibility, and it becomes clear why you may want to compare several independent views before making up your mind.

Explore 8 other fair value estimates on Photronics - why the stock might be worth as much as 18% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.