Coupang (CPNG) Stock Still Looks Cheap As Sales Keep Growing

Coupang, Inc. Class A CPNG | 0.00 |

Coupang stock has quietly built a mixed record for shareholders, with the share price down over the last year but the valuation checks still suggesting the current US$18.13 level may be on the cheap side.

- Over the past 5 years, Coupang has delivered a cumulative share price decline of about 55%, which means long term holders have experienced a material drawdown that puts extra focus on whether the current valuation offers a margin of safety.

- For the business, the key support for valuation can come from the ability to grow revenue while improving profitability in its core e commerce operations. A key risk is that heavy reinvestment needs or thinner margins limit the cash that ultimately reaches shareholders.

- On Simply Wall St's checks, Coupang screens as undervalued in 5 of 6 valuation tests, so the broader toolkit leans toward the stock trading below what its fundamentals might justify.

The issue now is whether Coupang's current price already reflects the pressure in its historical returns or if the valuation gap still leaves room for upside before the story changes.

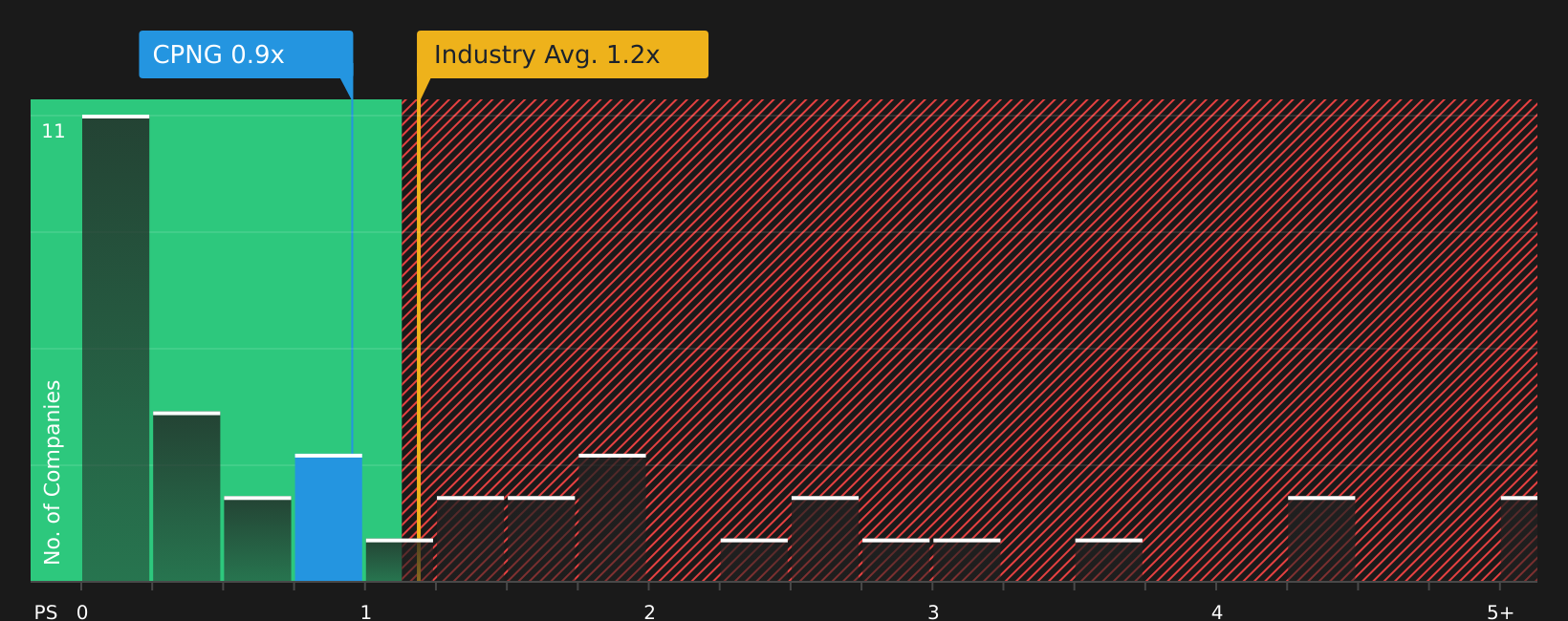

Does Coupang Look Undervalued on Sales?

The P/S multiple fits Coupang because revenue is still a central reference point, while earnings are less straightforward to evaluate through P/E. At the current share price, Coupang trades on a P/S of about 0.9x, compared with an industry average of around 1.2x for multiline retail peers and a broader peer group average near 2.4x.

The fair P/S ratio estimated for Coupang is about 1.3x, which is higher than the current 0.9x level. That gap suggests the stock is pricing Coupang's revenue at a lower level than the model implies, even after adjusting for its scale, business mix and risks in the core e-commerce operations. While a low P/S on its own does not indicate any specific investment outcome, it does indicate that the market is not paying a premium for each dollar of Coupang's sales.

On balance, Coupang stock appears undervalued on the P/S multiple compared with both tailored and industry benchmarks.

The Coupang Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Coupang sit between the valuation puzzle and your investment view, by spelling out which paths for Coupang's revenue growth, margins and earnings would need to play out for the stock to be worth materially more or less than today's price on the market. Each Narrative links a fair value estimate to a particular story about Coupang's potential catalysts and risks, so you can track over time which version of events seems closest to reality on the Community page.

The community is effectively weighing two very different futures for Coupang, with one camp focused on technology driven upside and the other on rising structural costs and regulatory pressure.

Bull case: 31% undervalued

"Ongoing investments in automation, AI, and logistics technology are already driving major improvements in operational efficiency and gross margins, and management sees significant further upside as these technologies are scaled. Over time, this is likely to result in continued margin expansion and growth in earnings..."

Bear case: 12% overvalued

"Coupang's long-term profitability is threatened by rising labor costs and the demographic challenges in South Korea, such as a shrinking workforce, which will significantly elevate operating expenses and strain last-mile logistics, leading to compressed net margins regardless of near-term gains in automation or process improvements..."

Do you think there's more to the story for Coupang? Head over to our Community to see what others are saying!

The Bottom Line

Coupang screens as undervalued on the market multiples used here, with its P/S ratio suggesting investors are paying less for each dollar of sales than for many peers. That discount only matters if Coupang can keep growing its revenue base while moving margins in the right direction, rather than seeing costs absorb most of the benefit. The crux is whether current pricing reflects justified caution on profitability or a gap between sentiment and the underlying business, and that is what will decide whether today’s discount proves attractive or a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.