Crane (CR): Assessing Valuation Following Declining Sales and Slower Organic Revenue Growth

Crane Company CR | 171.00 | +6.30% |

Despite recent worries over declining sales, Crane’s 24.14% year-to-date share price return stands out. Its three-year total shareholder return of 197.40% highlights robust long-term gains, even as momentum appears to be cooling in the near term.

If these shifting fortunes have you curious about where else strong returns might be found, now’s the perfect time to discover fast growing stocks with high insider ownership

With shares already up over 24% this year, the key question is whether Crane’s current valuation reflects future growth or if today’s lackluster momentum suggests a real buying opportunity remains for forward-looking investors.

Most Popular Narrative: 11.5% Undervalued

With Crane's narrative fair value of $211.88 sitting comfortably above the last close price, the narrative perspective presents a more optimistic outlook than current market sentiment. Here is the standout catalyst fueling this higher estimate.

Crane's recent acquisition of PSI (Druck, Panametrics, Reuter-Stokes) positions the company to capture rising demand for advanced sensing and fluid control in both aerospace and process industries. This move directly benefits from infrastructure modernization and growing automation, supporting sustained revenue and future margin expansion.

Want to know why this valuation pushes the envelope? The underlying assumptions hinge on ambitious forecasts for revenue, earnings, and margin expansion not typically seen in this sector. Is this a bold bet on structural change or just market optimism? Only the narrative's full details reveal the drivers behind the price target.

Result: Fair Value of $211.88 (UNDERVALUED)

However, persistent weakness in key European markets or challenges integrating recent acquisitions could quickly undermine the positive outlook for Crane’s future growth.

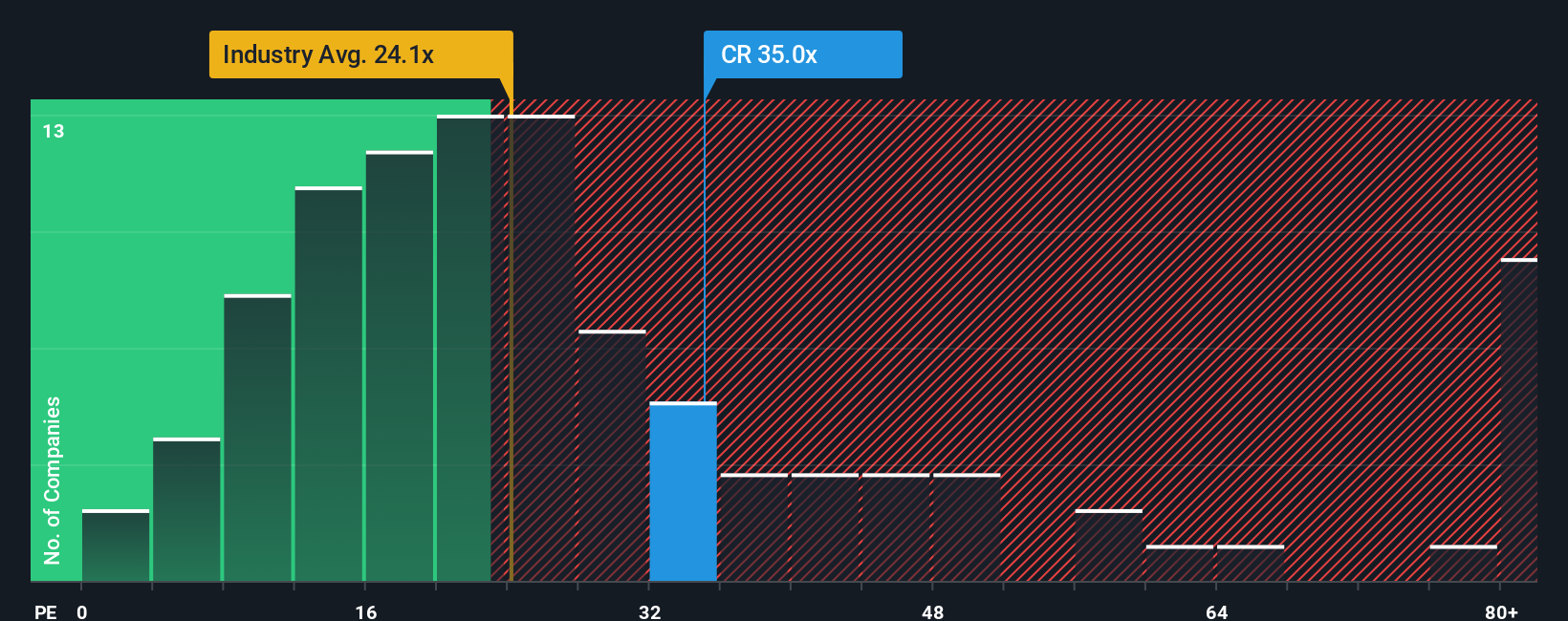

Another View: High Relative Valuation Raises Questions

While the narrative-based valuation signals opportunity, a look at Crane's price-to-earnings ratio tells a different story. At 35.7x, Crane trades well above both industry peers (21.3x) and the market's fair ratio of 25.9x. This makes its shares look relatively expensive. Could this premium reflect unique potential, or is it a risk for buyers at these prices?

Build Your Own Crane Narrative

If you see things differently or want to dig into the numbers yourself, you can build your own view on Crane’s future in just a few minutes, starting here: Do it your way

A great starting point for your Crane research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Stay ahead by using the right tools to spot promising stocks before the crowd. Miss out and you could leave untapped opportunities on the table.

- Tap into the future of medicine when you check out these 33 healthcare AI stocks, transforming patient care and diagnostics through artificial intelligence breakthroughs.

- Unlock the power of consistent income streams by exploring these 17 dividend stocks with yields > 3%, which offer attractive yields well above market averages.

- Get a front-row seat to technological innovation by browsing these 26 quantum computing stocks, pioneering the next era of computing and security.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.