Crescent Energy (CRGY) Is Up 11.8% After Return To Profitability And Royalty Cash Flow Launch – Has The Bull Case Changed?

Crescent Energy CRGY | 0.00 |

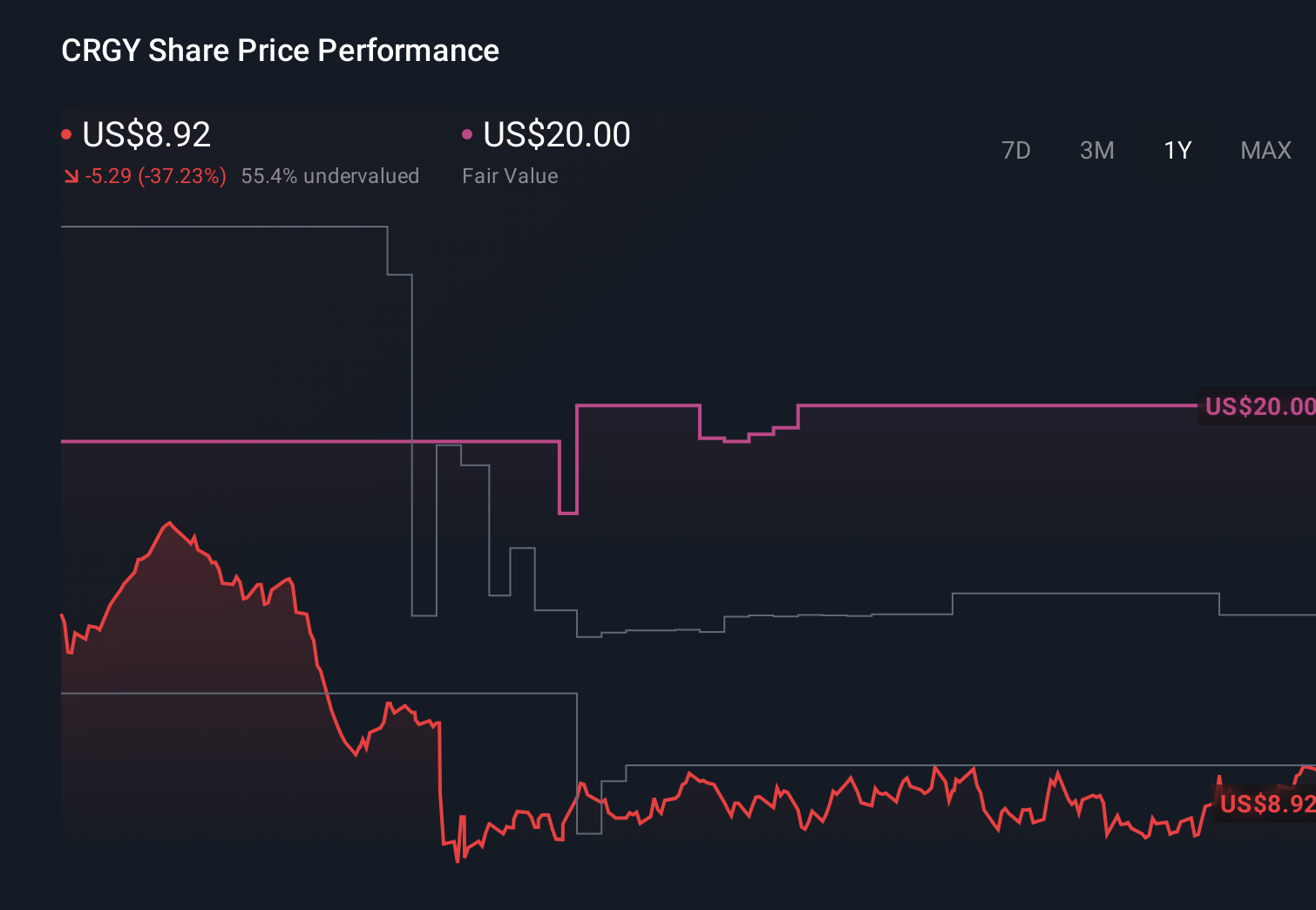

- Crescent Energy Company recently reported its fourth-quarter and full-year 2025 results, showing revenue of US$865.05 million for the quarter versus US$875.29 million a year earlier and a swing to full-year net income of US$132.91 million from a prior year net loss.

- Beyond the headline profitability shift, Crescent executed nearly US$5.00 billion of 2025 transactions, cut drilling and completion costs by 15%, and launched Crescent Royalties, which is already contributing US$160.00 million in annual cash flow.

- We’ll now examine how Crescent’s move to full-year profitability in 2025 reshapes its existing investment narrative and medium-term outlook.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

Crescent Energy Investment Narrative Recap

To own Crescent Energy, you need to believe it can keep turning its acquisition-heavy model and cost-cutting into durable, cash-generating profitability while managing balance sheet and commodity risks. The move to a US$132.91 million full-year profit in 2025 supports that case, and reinforces the near term catalyst around capital returns, but it does not erase the key risk that ongoing deal activity and basin concentration could still pressure margins and earnings if conditions turn less favorable.

The company’s 2025 results are most closely tied to its update on capital allocation, including boosting the share repurchase authorization to US$400 million and maintaining a US$0.12 per share dividend. That package connects directly to the profitability swing and cost reductions, and is likely to matter for how investors weigh Crescent’s acquisition risk against the potential for higher shareholder returns as Crescent Royalties and recent transactions contribute more cash flow over time.

Yet beneath Crescent’s new profitability, investors should still be aware of how its reliance on acquisitions could amplify balance sheet risk if...

Crescent Energy's narrative projects $5.2 billion revenue and $672.6 million earnings by 2028. This requires 14.8% yearly revenue growth and about a $649.5 million earnings increase from $23.1 million today.

Uncover how Crescent Energy's forecasts yield a $13.07 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Crescent could lift revenue toward about US$6.3 billion and earnings to roughly US$874 million, which paints a far brighter path than the consensus view of slower growth and balance sheet risk. With 2025’s profit swing and cost cuts now on the table, you can see how that bullish cost synergy story might gain support or be challenged, and why it is worth comparing these very different expectations before you decide what you believe.

Explore 5 other fair value estimates on Crescent Energy - why the stock might be worth over 3x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crescent Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

No Opportunity In Crescent Energy?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.